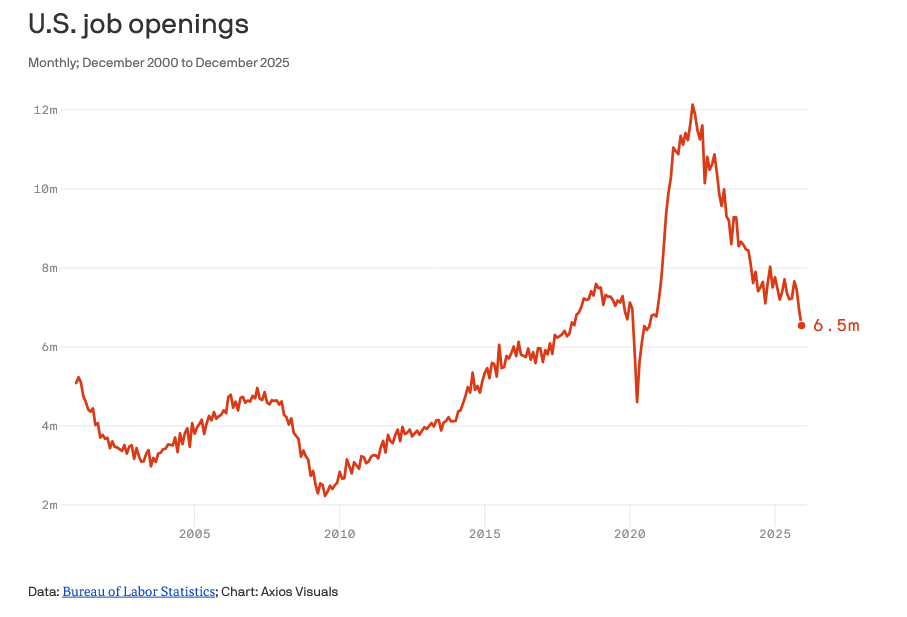

US employers cut more jobs last month than in any period since 2009. More than 100,000 workers were fired at Amazon, UPS, and Dow, and hiring was the slowest for any January on record, according to outplacement firm Challenger, Gray & Christmas. The low-fire, low-hire dynamic that has kept the US labor market in an anxious balance appears to have tipped. US layoffs in January hit highest monthly record since 2009 – https://www.semafor.com/article/02/05/2026/us-layoffs-in-january-hit-highest-monthly-record-since-2009

“We have to understand that anything in the past takes you out of the present moment. Anything in the future takes you out of the present moment.”

Zen Master Daigneault

To readers who are visiting this blog for the first time my posts on Random Thoughts About Retirement and Unretirement are written by an Old Guy who is old enough to be retired but isn’t retired and is still working. I had another birthday and the older I get the more I think about retirement. Back in 2023 I was thinking about what retirement for me would look like (see More Random Thoughts on Retirement – June 2023). But decisions such as this take serious thought and consideration. At first I thought I wanted to retire to a quiet life of blogging and writing my Future Best Seller titled The Man Who Had No Hobbies. After much thought I decided to add a short term goal to my retirement plan. My new short term goal is to avoid unretirement.

My RSS feed feeds me headlines on unretirement.

According to a new report from T. Rowe Price around 7% of retirees are looking for work in retirement, while 20% say they’re already working part time or full time…The two main reasons for coming back into the workforce are a tale of opposites. While 45% chose to work for social and emotional benefits… a slightly larger percentage — 48% — felt they needed to work for financial reasons.

Once an eagerly awaited milestone, retirement is currently undergoing a transformative reevaluation. Traditionally seen as a well-deserved period of rest and relaxation, the dream of early retirement is now being challenged by a new perspective – that of embracing lifelong work. This paradigm shift reflects the changing nature of work, increased life expectancy, and the desire for personal fulfillment.

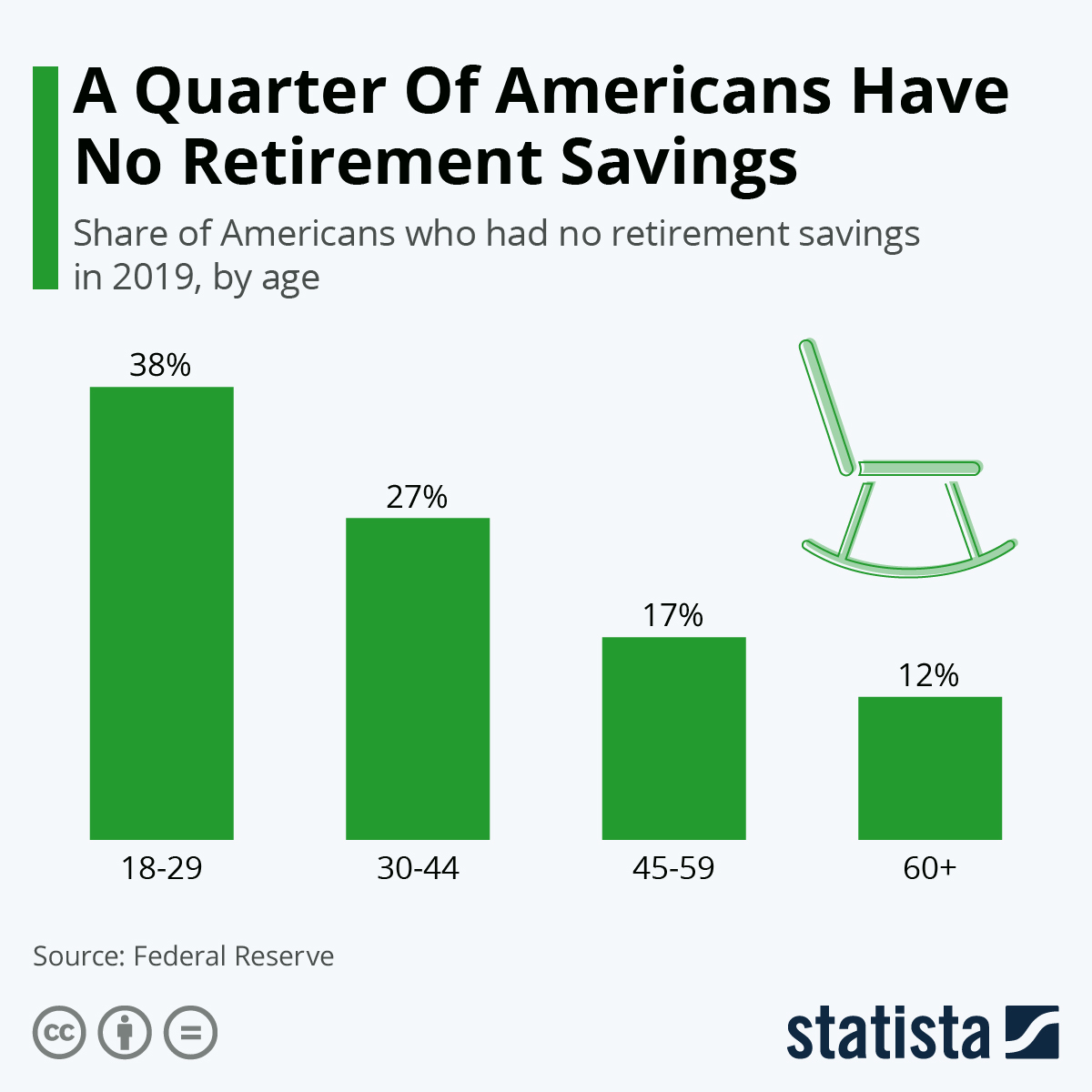

The reality is many won’t have a choice. The following chart illustrates retirement savings as of 2019.

Americans are having trouble financially preparing themselves for life after work. A recent Federal Reserve report found that nearly a quarter of U.S. adults have absolutely no retirement savings or pension. Even though the level of preparation increases as people get older, concern about inadequate savings is still readily apparent across all age groups, even older people in their 60s.

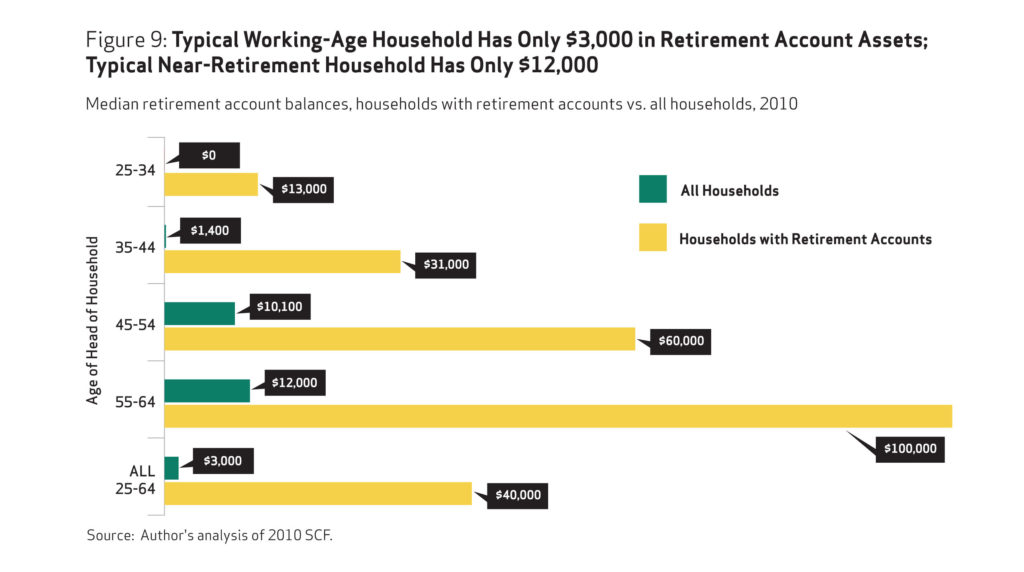

OOPS. I’m glad I didn’t click the Publish button. The savings situation appears to be worse than I thought. The study below was an analysis of data from 2010!

The study broadly examines how American households are faring in relation to retirement savings targets recommended by some financial services firms. It uses the Federal Reserve’s Survey of Consumer Finances to analyze retirement plan participation, savings, and overall assets of all U.S. households age 25 to 64, not just those with retirement account assets. This is important because some 45 percent, or 38 million working-age households, do not have any retirement account assets.

The average working household has virtually no retirement savings. When all households are included— not just households with retirement accounts—the median retirement account balance is $3,000 for all working-age households and $12,000 for near-retirement households. Two-thirds of working households age 55-64 with at least one earner have retirement savings less than one times their annual income, which is far below what they will need to maintain their standard of living in retirement.

The findings confirm that the American Dream of retiring comfortably after a lifetime of work will be impossible for many. Based on 401(k)–type account and IRA balances alone, some 92 percent of working households do not meet conservative retirement savings targets for their age and income. Even when counting their entire net worth, 65 percent still fall short.

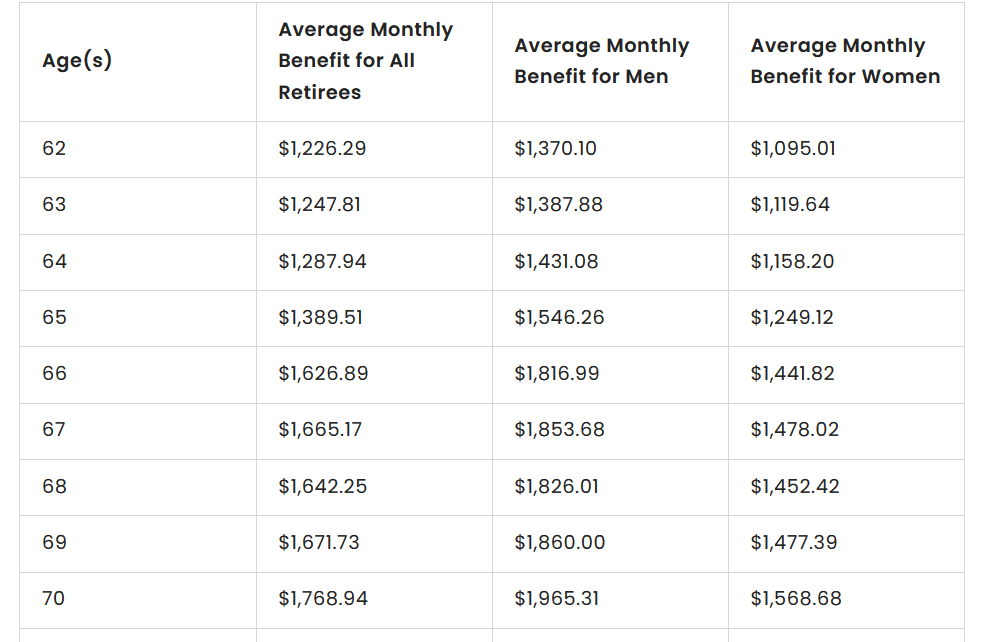

So how will you afford retirement without any savings? Don’t look to Social Security. Here’s some numbers on average Social Security payments. The full chart at the source website goes up to age 100.

As of December 31, 2021, the average Social Security payment for all retirees was $1,658.03 a month, according to the Social Security Administration’s Annual Statistical Supplement for 2022. For men, the overall average was $1,838.08. For women, the average was $1,483.75 — a difference of $354.33 per month.

Whether people unretire or simply stay in the workforce longer, some of the largest financial benefits of additional years of work are delaying retirement account withdrawals and delaying claiming Social Security benefits. These actions essentially shorten the amount of time your assets will need to support you in retirement. Even a few additional years of income have a positive effect on the probability that you won’t outlive your funds.

Through November, employers have announced 1,170,821 job cuts, an increase of 54% from the 761,358 announced in the first eleven months of last year. Year-to-date job cuts are at the highest level since 2020 when 2,227,725 cuts were announced through November. It is the sixth time since 1993 that job cuts through November have surpassed 1.1 million. Challenger Report: 71,321 Job Cuts on Restructurings, Closings, Economyhttps://www.challengergray.com/blog/challenger-report-71321-job-cuts-on-restructurings-closings-economy/

Yikes.

In my less than illustrious career I’ve suffered 100% reductions in income multiple times. Hopefully the newly unemployed have some form of a fallback plan.

The Boss (SWMBO) and I talk about this often. Once the W2 income stops and we have to rely upon a small corporate pension, savings, and a shaky Social Security promise we’ll have to get conservative on our spending. No more Stratocasters. Less purchases for wardrobe enhancements. Gas station beer instead of craft brews.

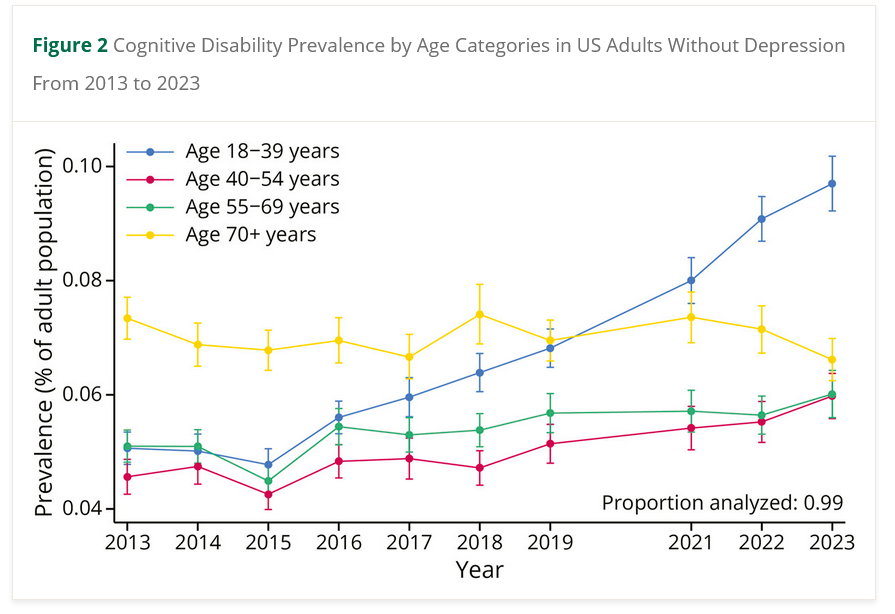

Cognitive disability was strongly associated with socioeconomic factors such as income and education. Adults with household incomes less than $35,000 consistently reported the highest prevalence, increasing from 8.8% (95% CI 8.5%–9.2%) in 2013 to 12.6% (95% CI 12.0%–13.2%) in 2023. By contrast, adults in the highest income bracket (household income ≥ $75,000) had substantially lower prevalence, with a more modest increase from 1.8% (95% CI 1.6%–2.0%) in 2013 to 3.9% (95% CI 3.6%–4.2%) in 2023. Rising Cognitive Disability as a Public Health Concern Among US Adults – Neurology October 21, 2025 issue 105 (8) e214226 https://doi.org/10.1212/WNL.0000000000214226

I’ve decided not to retire. Wait, let me clarify my statement.

I’ve not changed my mind about my decision not to retire five years ago.

I love double negative sentences.

Fewer than twenty percent of older people worldwide enjoy a retirement pension that is enough for them to live off. Although countries like China and India are now also developing their pension systems, the prospect of most older people receiving pensions totaling 60 to 70% of their final salaries remains a long way off.

The majority of our friends are retired. I’m always asked when I’m going to retire. My quick answer was always “Don’t know”. I’ve since modified my response to “Two to four years”. This has been my answer for the past two years. Might still be my answer next year too.

Interestingly, older workers (65+) earn around $3,000 more than those in the 25 to 34 bracket, reflecting a group of late-career professionals who continue to command strong wages. Charted: Median U.S. Salaries by Age Grouphttps://www.visualcapitalist.com/charted-median-u-s-salaries-by-age-group/

Late-career professional. There seem to be a lot more of us now.

Three in four workers (75 percent) plan to work for pay in retirement, compared with just 29 percent of retirees who report they have actually worked for pay in retirement. In fact, the RCS has consistently found that workers are far more likely to plan to work for pay in retirement than retirees are to have actually done so. 2025 Retirement Confidence Survey – https://www.ebri.org/retirement/retirement-confidence-survey

But if you’re working for pay in retirement how can this be considered retirement?

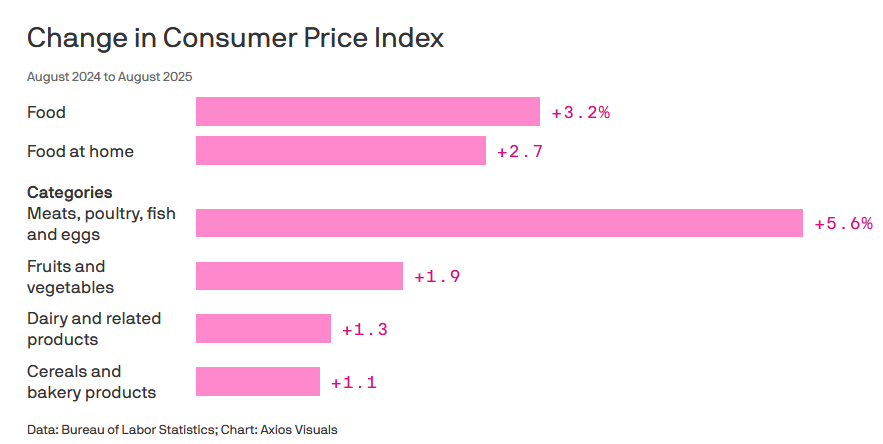

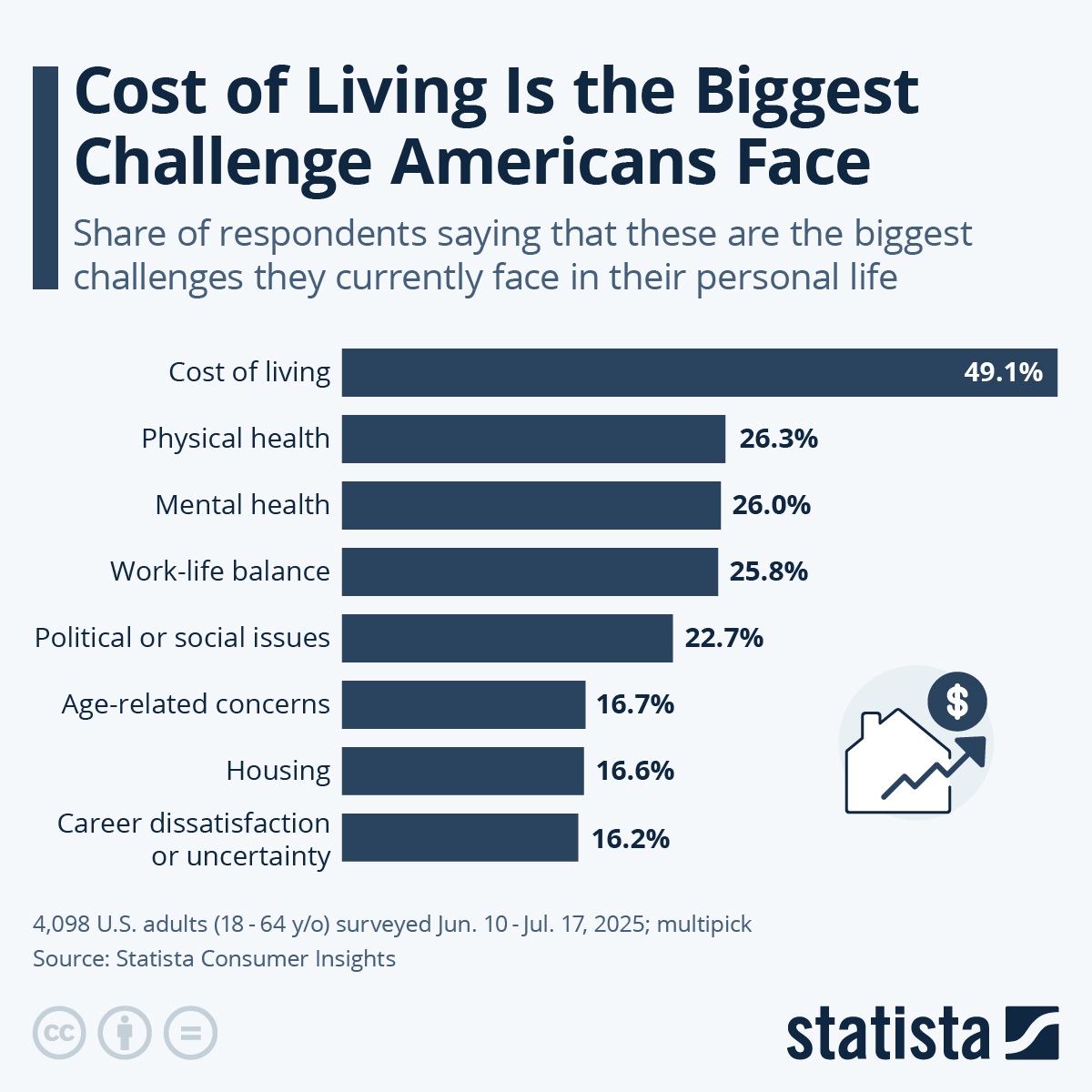

It is a common misconception that prices come down when inflation cools, when in reality a period of high inflation leaves a legacy of high prices. According to the Bureau of Labor Statistics, U.S. consumer prices have increased 22.7 percent since January 2021, with some categories seeing even steeper price increases than that. Food prices have are up 25 percent, rents have increased almost 27 percent and transportation prices are up 28 percent. And yet, nominal wages have only grown 21.8 percent since January 2021, leaving many people worse off than they were almost five years ago. Cost of Living Is the Biggest Challenge Americans Facehttps://www.statista.com/chart/35054/biggest-challenges-faced-by-americans/

The second survey is small with just over 200 respondents. The methodology statement is vague so it’s hard to tell if the findings are truly representative of a larger population.

Maybe the survey got an overwhelming number of pessimists.

You must be logged in to post a comment.