A conservative colleague said the use of AI to create addiction and device dependency was evil. That is an understatement. These kids rely on ChatGPT not just for information but also to make choices, and for many, that seems to extend to every aspect of their lives. Sam Altman makes clear in video clips below that this extreme loss of independence, of personal autonomy, is deliberate.

That means unless these kids can find a way to break free, they are cognitive serfs that can be told to do anything. How to vote. Whether to sign up to die in a hopeless war. Whether to take a job in a unsafe meatpacking plant and risk loss of limbs.

This widespread abuse is far worse than what the Sacklers and other opioid peddlers did to mainly working class pain victims, or what the British did to China in the Opium Wars. At least with opioid addiction, it is possible for the victims to recover even if the withdrawal process is painful. The evidence is mounting that even for adults, regular use of AI diminishes reasoning skills and attention spans.

These children are being turned into automatons, incapable of independent thought and action. It’s widely known in developmental psychology that if certain patterning does not happen at critical ages, the deficit is permanent. Kittens needing visual input in their first few days or they are blind. Kids who don’t crawl having coordination issues as adults due to missing important movement patterning. Less dramatic versions are not being able to make sounds in foreign languages if you have not heard and practiced them when young.

Physical activity consistently emerges as the most important factor influencing both absolute physical capacity and the rate of age-related decline. Our longitudinal data are consistent with previous studies showing that regular physical activity can attenuate the decline in physical performance [17, 32–37]. Individuals who were physically active in their leisure time at age 16 maintained higher aerobic capacity, muscular endurance and muscle power throughout the observation period. This emphasizes the importance of early intervention to establish positive exercise habits in adolescence and early adulthood, as these patterns appear to have long-term benefits for physical function. Encouragingly, our results show that transitioning from physical inactivity to activity at any age significantly improves performance in all fitness modalities studied. These findings contradict the assumption that early inactivity irreversibly impairs physical performance. Rather, taking up regular physical activity leads to measurable improvements in performance even in later decades of life. This finding is of particular importance for clinical practice, as physical activity is still the only evidence-based intervention to reduce the risk of sarcopenia [2, 38]. Recent large population studies also show that an active lifestyle is beneficial at any age [13, 39, 40]. Rise and Fall of Physical Capacity in a General Population: A 47-Year Longitudinal Study – https://onlinelibrary.wiley.com/doi/10.1002/jcsm.70134

Text above in bold are my highlights.

Despite the documented limitations this is a very strong study.

I’ve been doing my home based virtual physical therapy for nearly a year. I’m trying to get to the gym at least twice a week. I don’t walk as much as I used to but…

The power of PATHWEIGH is that it puts patients and their primary care provider on the same page…It all started with signage placed in clinics that notified patients that if they wanted to make an appointment to specifically talk about weight management, all they had to do was approach the desk and ask for it. That request automatically triggered a mechanism in the patient’s electronic health record that sent them a survey that after completion would flow into the provider’s notes. Instead of spending so much time typing and talking about the patient’s history, the scheduled visit could be centered around solutions. PATHWEIGH: A Model Changing Weight Management For All – https://news.cuanschutz.edu/medicine/pathweigh-pilot-research

As Pepperdine University literature professor Jessica Hooten Wilson told Fortune in a recent interview, “it’s not even an inability to critically think. It’s an inability to read sentences.” Gen Z Arriving at College Unable to Read https://futurism.com/future-society/gen-z-literacy-reading

“We have to understand that anything in the past takes you out of the present moment. Anything in the future takes you out of the present moment.”

Zen Master Daigneault

To readers who are visiting this blog for the first time my posts on Random Thoughts About Retirement and Unretirement are written by an Old Guy who is old enough to be retired but isn’t retired and is still working. I had another birthday and the older I get the more I think about retirement. Back in 2023 I was thinking about what retirement for me would look like (see More Random Thoughts on Retirement – June 2023). But decisions such as this take serious thought and consideration. At first I thought I wanted to retire to a quiet life of blogging and writing my Future Best Seller titled The Man Who Had No Hobbies. After much thought I decided to add a short term goal to my retirement plan. My new short term goal is to avoid unretirement.

My RSS feed feeds me headlines on unretirement.

According to a new report from T. Rowe Price around 7% of retirees are looking for work in retirement, while 20% say they’re already working part time or full time…The two main reasons for coming back into the workforce are a tale of opposites. While 45% chose to work for social and emotional benefits… a slightly larger percentage — 48% — felt they needed to work for financial reasons.

Once an eagerly awaited milestone, retirement is currently undergoing a transformative reevaluation. Traditionally seen as a well-deserved period of rest and relaxation, the dream of early retirement is now being challenged by a new perspective – that of embracing lifelong work. This paradigm shift reflects the changing nature of work, increased life expectancy, and the desire for personal fulfillment.

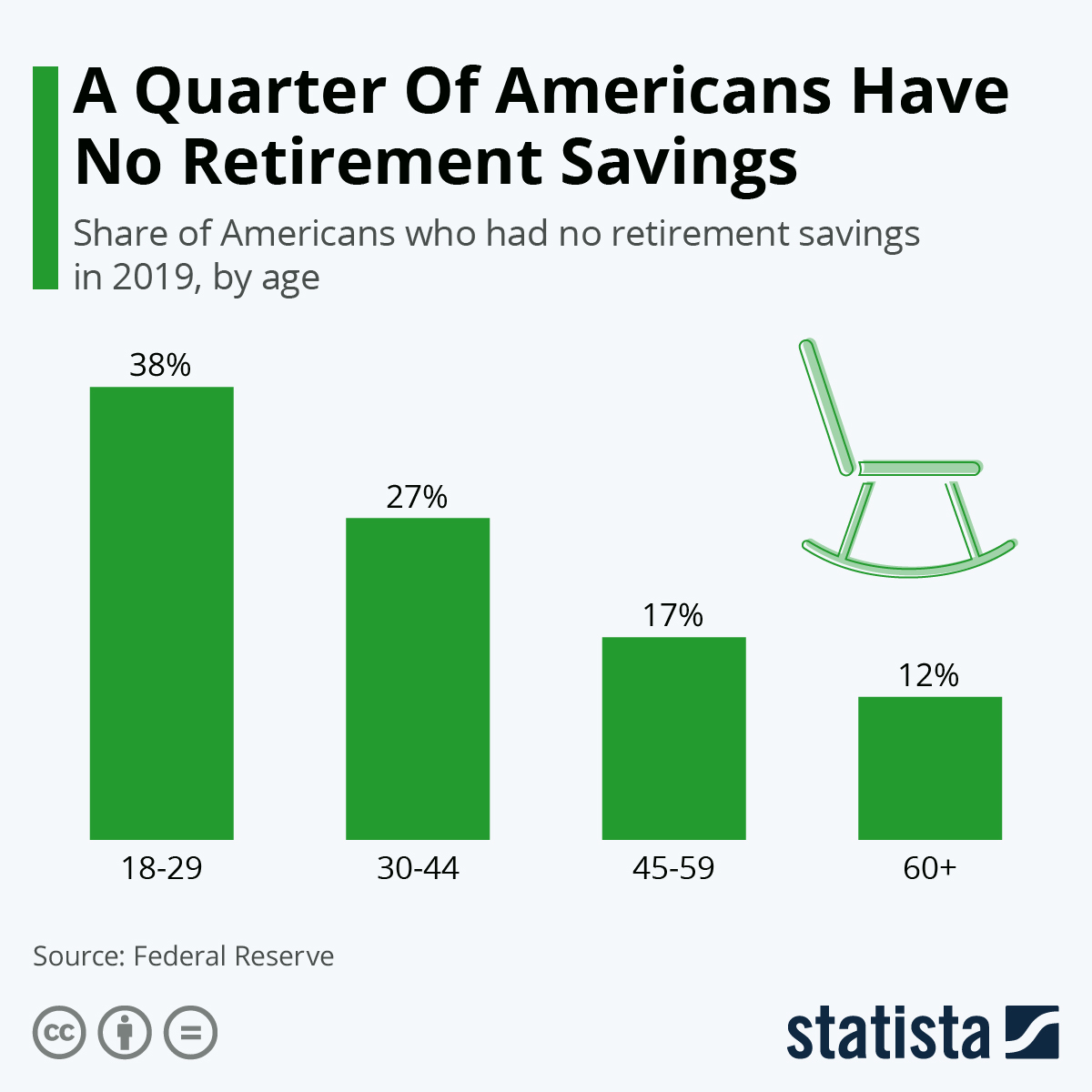

The reality is many won’t have a choice. The following chart illustrates retirement savings as of 2019.

Americans are having trouble financially preparing themselves for life after work. A recent Federal Reserve report found that nearly a quarter of U.S. adults have absolutely no retirement savings or pension. Even though the level of preparation increases as people get older, concern about inadequate savings is still readily apparent across all age groups, even older people in their 60s.

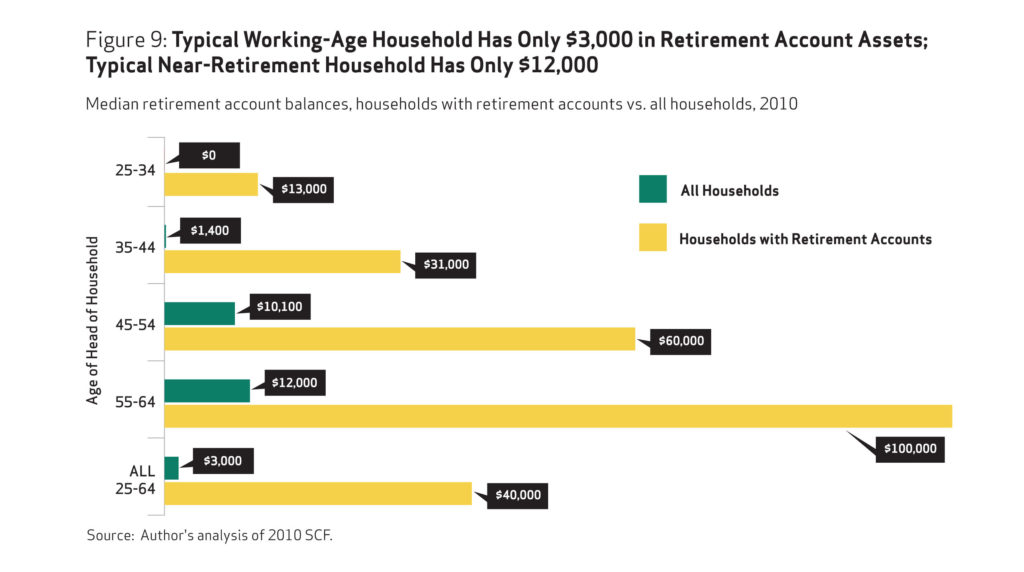

OOPS. I’m glad I didn’t click the Publish button. The savings situation appears to be worse than I thought. The study below was an analysis of data from 2010!

The study broadly examines how American households are faring in relation to retirement savings targets recommended by some financial services firms. It uses the Federal Reserve’s Survey of Consumer Finances to analyze retirement plan participation, savings, and overall assets of all U.S. households age 25 to 64, not just those with retirement account assets. This is important because some 45 percent, or 38 million working-age households, do not have any retirement account assets.

The average working household has virtually no retirement savings. When all households are included— not just households with retirement accounts—the median retirement account balance is $3,000 for all working-age households and $12,000 for near-retirement households. Two-thirds of working households age 55-64 with at least one earner have retirement savings less than one times their annual income, which is far below what they will need to maintain their standard of living in retirement.

The findings confirm that the American Dream of retiring comfortably after a lifetime of work will be impossible for many. Based on 401(k)–type account and IRA balances alone, some 92 percent of working households do not meet conservative retirement savings targets for their age and income. Even when counting their entire net worth, 65 percent still fall short.

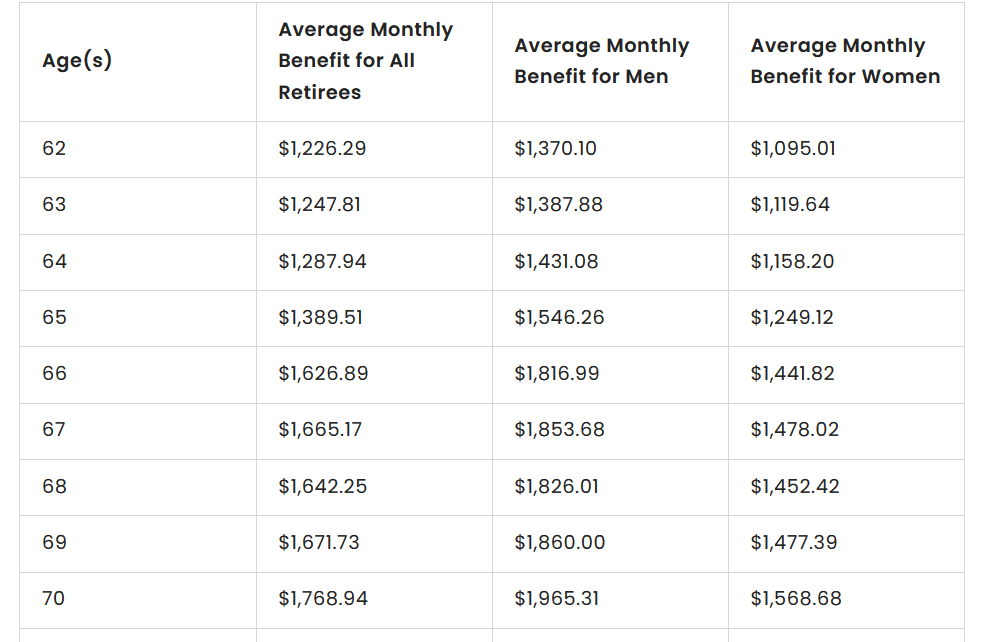

So how will you afford retirement without any savings? Don’t look to Social Security. Here’s some numbers on average Social Security payments. The full chart at the source website goes up to age 100.

As of December 31, 2021, the average Social Security payment for all retirees was $1,658.03 a month, according to the Social Security Administration’s Annual Statistical Supplement for 2022. For men, the overall average was $1,838.08. For women, the average was $1,483.75 — a difference of $354.33 per month.

Whether people unretire or simply stay in the workforce longer, some of the largest financial benefits of additional years of work are delaying retirement account withdrawals and delaying claiming Social Security benefits. These actions essentially shorten the amount of time your assets will need to support you in retirement. Even a few additional years of income have a positive effect on the probability that you won’t outlive your funds.

lifeunderwriter.net is a personal WordPress.com blog run by an experienced life insurance underwriting professional (the author uses the handle “SupremeCmdr” and has been posting since at least 2008).

The site’s tagline is “Curated Content From a Life Underwriting Professional”. It primarily features:

Curated links to external articles, studies, and news items

Commentary and personal reflections from the author’s perspective as someone who has worked in life insurance underwriting (assessing mortality risks, medical records, risk classification for policies, etc.)

Insights related to the insurance industry, mortality trends, health/longevity topics (e.g., vitamin D in older adults, obesity treatments, nutrition, diabetes risks), retirement planning (e.g., deferring Social Security), remote work in insurance, and occasional broader thoughts on society, technology, or resilience

The content often ties back to how various medical, lifestyle, or demographic factors might influence underwriting decisions in life insurance, but it has evolved over time into a more eclectic mix. Recent posts (including into 2025) frequently cover:

Health and nutrition (e.g., protein’s role in diets, GLP-1 drugs, probiotics)

Personal anecdotes (cooking recipes, music like Pat Metheny)

Retirement and aging commentary

Industry observations (e.g., older workers, AI’s effects)

The blog is not a commercial service site offering underwriting services (an older page mentions “Underwriting Solutions LLC” from around 2006–2017, but those appear to be in hibernation or discontinued). It functions more as a personal journal / link blog than a formal resource or forum.

It remains active with regular (sometimes frequent) posts, though the style is informal, opinionated, and not strictly professional/academic. If you’re in the life insurance field or interested in mortality/longevity topics through an underwriter’s lens, it can offer interesting curated reading; otherwise, it’s a niche personal blog.

It has evolved over time into a more eclectic mix?

According to the USP, the bulk of the APIs come from India. That country is responsible for 50% of the active pharmaceutic ingredients. China is not far behind at 32%. The European Union supplies 10%. That’s a big change since 2000. Back then, European countries like France, Germany, Switzerland and Denmark supplied 42% of the APIs. Drug Recalls From India – Can You Trust Foreign-Made Generics? – https://www.peoplespharmacy.com/articles/more-drug-recalls-from-india-do-you-trust-foreign-made-generics

Dozens of companies received approval from the FDA over the years to sell metoprolol and bupropion in the U.S. Yet from 2018 to 2024, the agency reported running only 2 tests on metoprolol and 7 on bupropion through its quality surveillance program — in each case, by pulling a sample from a single drug maker. In many of those years, the drugs weren’t tested at all, FDA records show. Those that were assessed received passing results. The FDA Often Doesn’t Test Generic Drugs for Quality Concerns, So ProPublica Did – https://www.propublica.org/article/fda-generic-drug-testing

You must be logged in to post a comment.