You must be 18 or older and meet one of these requirements when you start GLP-1 therapy:

You have a body mass index (BMI) of 35 or more.

You have a BMI between 30-34.99 and have at least one of these conditions: Diastolic heart failure (also called heart failure with preserved ejection fraction) Uncontrolled high blood pressure (also called hypertension) Chronic kidney disease at stage 3a or higher Prediabetes A previous heart attack (also called myocardial infarction) or stroke Blocked arteries in your legs or arms (also called peripheral artery disease) with symptoms

You have a BMI between 27-29.99 and have at least one of these conditions: Prediabetes A previous heart attack (also called myocardial infarction) or stroke Blocked arteries in your legs or arms (also called peripheral artery disease) with symptoms

Yes, I loved writing the click bait title to this post.

This is another post in the never ending series of random thoughts on retirement. For the curious, here’s a link to my previous posts full of random thoughts (brain droppings): https://lifeunderwriter.net/tag/retirement/.

I am writing this on Father’s Day, the fourth day of a four day weekend and I’m ready to go back to work. It’s tough being an Old Guy who is old enough to be retired but isn’t retired and still working. Some days I wonder why I’m not retired. I guess this is all part of my living a longer healthier life strategy.

Social connection, prosociality, spirituality, optimism, and work—growing evidence suggests these five factors can play an important role in improving the well-being of people and communities…Work is one of the most important—and neglected—social determinants of health, according to Lisa Berkman, Thomas D. Cabot Professor of Public Policy and of Epidemiology at Harvard Chan School and director of the Harvard Center for Population and Development Studies. “Work drives income, social ties, and the opportunity for meaningful participation in society,” she said. “As such, it also shapes both our cognitive and physical health in many different ways.” The importance of connections: Ways to live a longer, healthier life – https://hsph.harvard.edu/news/the-importance-of-connections-ways-to-live-a-longer-healthier-life/

The optimism factor is interesting.

“The findings are remarkably consistent,” she said. “Across different racial and ethnic populations, we have seen that people who are more optimistic are more likely to age in good health and less likely to suffer from chronic diseases, physical illness, or cognitive impairments in old age. Optimists are also more likely to live exceptionally longer lives, beyond age 85 or more.”

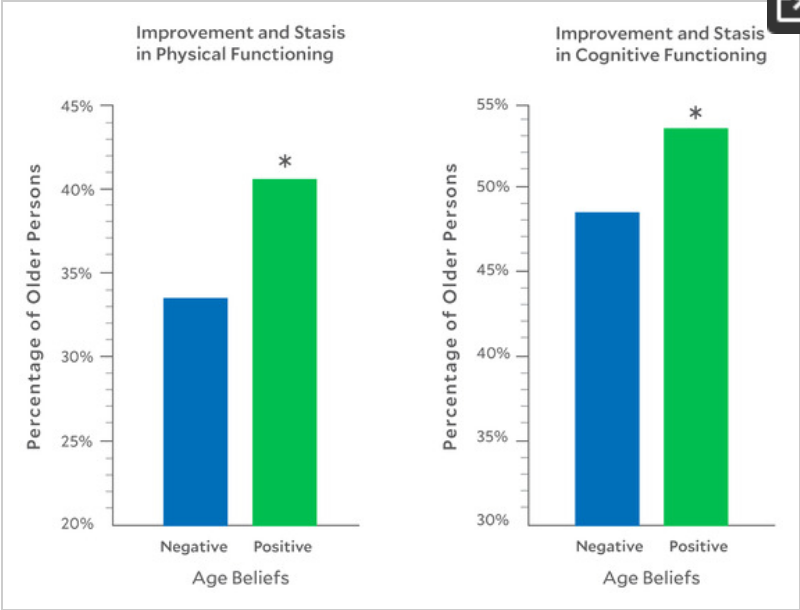

Aging Redefined: Cognitive and Physical Improvement with Positive Age Beliefs

Background/Objectives: A widespread assumption exists among scientists, health care providers, and the public that later life is a time of inevitable and universal cognitive and physical decline. This assumption is likely due to considering older persons who improve to be exceptions, and the reliance on aging-health measures that do not allow for improvement. In contrast, we utilized a measure that allowed for an upward trajectory to occur. Our objective was to examine whether a meaningful number of older persons improve with this measure and, if so, to examine whether a promising modifiable culture-based variable, positive age beliefs, contributes to this improvement. Methods: Individuals 65 years and older, who participated in a nationally representative longitudinal study, had their physical health assessed by walking speed and their cognitive health assessed by a global performance measure. We calculated the percentage of the sample that showed improvement in each domain from baseline to the last measurement up to 12 years later. We also examined whether a positive-age-belief measure predicted this improvement in regression models. Results: It was found that 45.15% of persons improved in cognitive and/or physical function over this period, and positive age beliefs predicted these two types of improvement, both with and without adjusting for relevant covariates. Conclusions: Our findings underscore the need to instill or magnify the positivity of age beliefs and to redefine aging so that it includes the possibility of improvement.

In sociology this phenomenon is known as a self-fulfilling prophecy.

Yes dear reader, yet another post in the never ending series of random thoughts on retirement. For the curious, here’s a link to some previous posts https://lifeunderwriter.net/tag/retirement/. I am an Old Guy who is old enough to be retired but isn’t retired and still working. After many mornings spent in deep contemplation and many posts where I think out loud I’ve finally accepted my fate and come to a deeper understanding of why I do what I do.

I’ve spent a lifetime working in risk management. Finally, the light bulb came on.

I am actively managing my longevity risk. It’s what I do. I manage risks.

The majority of our friends are retired. I’m always asked when I’m going to retire. My answer was always “Don’t know”. I subsequently modified my response to “Two to four years”. This has been my answer for the past two years. But now when someone asks when I will retire, my answer will be:

I am managing my longevity risk. I am managing future inflation risk.

Imagine you retire at 65, feeling confident. You’ve budgeted $80,000 a year to live comfortably — travel, dining out, covering healthcare, the works.

Fast-forward 25 years.

At age 85, you’re still spending about $80,000 a year … but that no longer buys what it used to.

That nice dinner out that cost $100 now costs about $210

A $5,000 annual vacation is now closer to $10,500

Groceries that ran $10,000 a year are now over $21,000

In other words, your $80,000 lifestyle now costs roughly $168,000 to maintain.

Ghilarducci is spot on with her assessment. My plan on working longer wasn’t really a plan so much as it was a set of assumptions. Everything had to go as “planned” or forget about working longer. The two major variables were continued good health and finding an employer that values older workers.

I got lucky. My illusion is working (pun intended).

About 20 years ago, neuropathologists began to report an inconvenient finding in the autopsied brains of people with dementia: Most have evidence of more than one disease. Studies since have shown the brains of up to half of people diagnosed with Alzheimer’s disease also have a key feature of Parkinson’s disease—deposits of the protein alpha synuclein. At the same time, up to half of Parkinson’s patients who develop dementia have elevated levels of beta amyloid and tau proteins, hallmarks of Alzheimer’s. Most dementia patients have multiple brain diseases – https://www.science.org/content/article/most-dementia-patients-have-multiple-brain-diseases-how-should-they-be-treated

Conclusions and Relevance Adults 75 years of age or older with adenoma at prior colonoscopy were more likely to experience subsequent CRC and CRC death compared with those without adenoma, but cumulative risks were low and were far exceeded by competing risks for non-CRC death. Older adults may consider deprioritizing surveillance colonoscopy relative to other health concerns. Colorectal Cancer and Mortality Risk Among Older Adults With vs Without Adenoma on Prior Colonoscopy – https://jamanetwork.com/journals/jama/article-abstract/2847311

Though the traditional retirement age in the U.S. typically falls between 62 and 67, many Americans continue working beyond that point. As of 2024, slightly more than 22% of adults aged 65 and older are still employed, either full-time or part-time. Though the traditional retirement age in the U.S. typically falls between 62 and 67, many Americans continue working beyond that point. As of 2024, slightly more than 22% of adults aged 65 and older are still employed, either full-time or part-time. – https://financebuzz.com/working-in-retirement-data

I’m not the only Old Guy who is still working past age 65.

But despite the fact I’m not the only Old Guy who is still working past age 65 more people are starting retirements earlier than they expected (always have a Plan B and maybe even a Plan C).

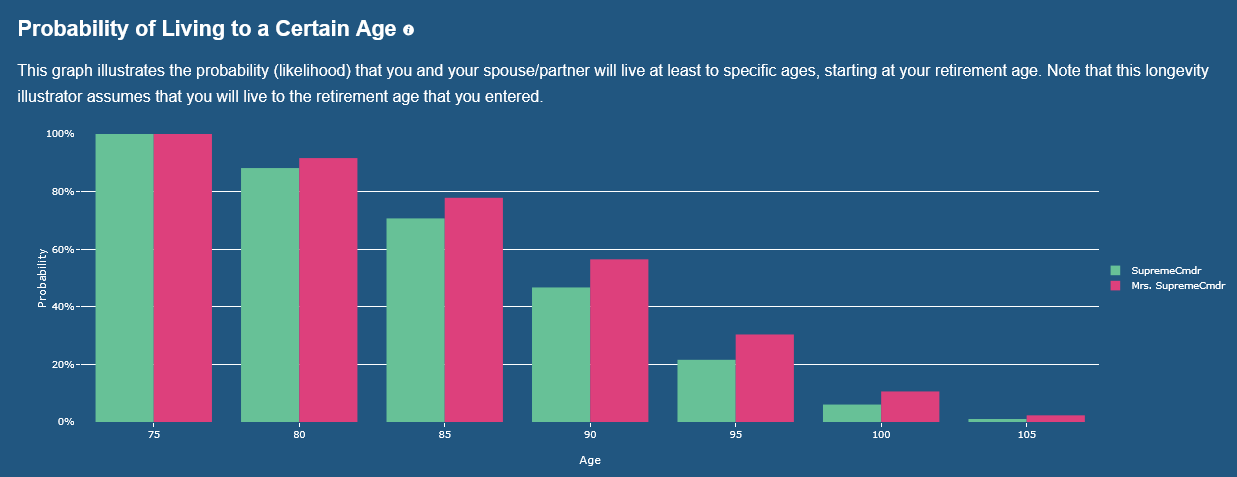

There is a significant chance that you will live for many years beyond the average, and you should consider this possibility when thinking about your retirement. The Actuaries Longevity Illustrator (“ALI”) has been developed as an educational tool by the American Academy of Actuaries and the Society of Actuaries to help you gauge what those chances are. Reflecting on your longevity will allow you to consider the risks of outliving your financial resources, i.e., the chance of running out of money during your lifetime, which we refer to as retiree financial longevity risk . The ALI helps you to consider those risks by letting you see how long you might live. https://www.longevityillustrator.org/

Try this calculator to see your probability of living to certain ripe old age.

We plan for the money. We don’t plan for the Monday morning when no one needs you to be anywhere.

Julianne Holt-Lunstad, a professor of psychology and neuroscience at Brigham Young University, published a landmark meta-analysis in 2015 involving over 3.4 million participants. Her finding: social isolation increases the risk of premature death by 26%, and loneliness by 29%. Those numbers rival the health impact of smoking fifteen cigarettes a day. We treat smoking as a public health crisis. We treat retirement loneliness as a personal failing.

Though the traditional retirement age in the U.S. typically falls between 62 and 67, many Americans continue working beyond that point. As of 2024, slightly more than 22% of adults aged 65 and older are still employed, either full-time or part-time. Though the traditional retirement age in the U.S. typically falls between 62 and 67, many Americans continue working beyond that point. As of 2024, slightly more than 22% of adults aged 65 and older are still employed, either full-time or part-time. – https://financebuzz.com/working-in-retirement-data

So I’m not the only Old Guy who is still working past age 65.

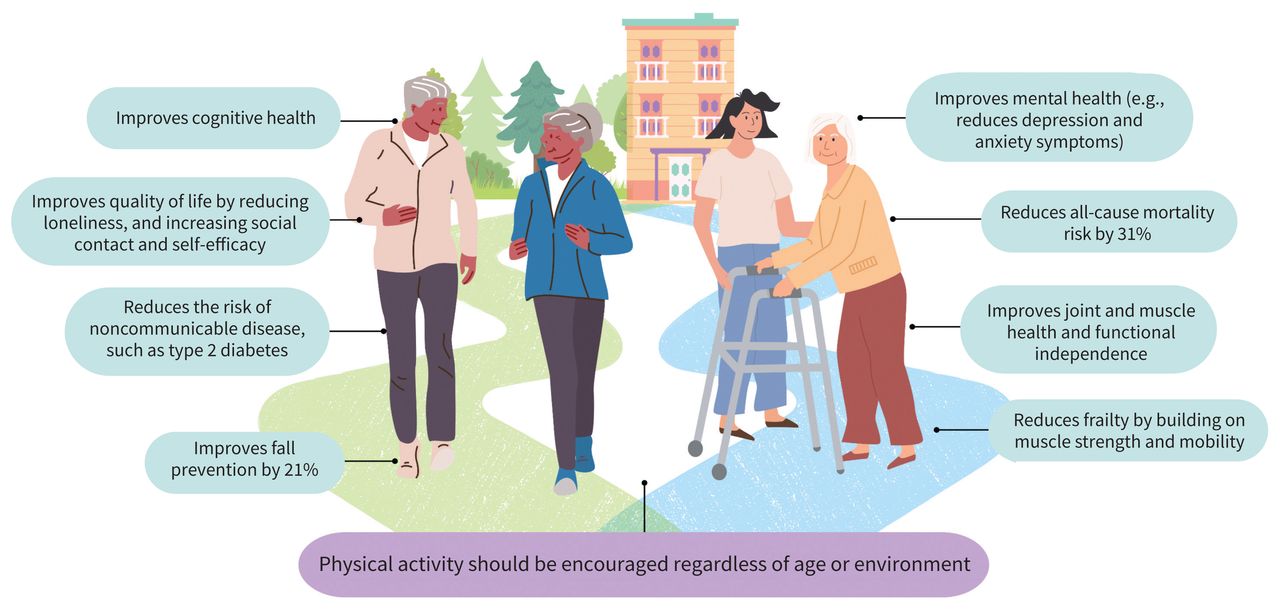

The association between physical activity and mortality and morbidity is well established. A 2023 meta-analysis of large prospective studies that examined dose–response found that physical activity levels equivalent to the recommended 150 minutes per week of moderate physical activity reduced all-cause mortality by 31% compared with no physical activity.12 The authors used metabolic equivalent of task (MET), the ratio of work metabolic rate to resting metabolic rate. One MET is equivalent to the energy cost of sitting quietly. A 2019 systematic review and meta-analysis found that, among middle-aged and older adults (aged ≥ 40 yr), higher levels of total physical activity were associated with reduced risk of death in a dose–response relation, such that the most, second-most, and third-most active quartiles were associated with 0.47, 0.35, and 0.28 hazard ratios, respectively, compared with the least active quartile.13 According to a large 2019 observational study, resistance exercise is also associated with reduced mortality independent of aerobic exercise.14 Two 2022 meta-analyses found, respectively, that 60 minutes of resistance exercise per week is associated with a risk reduction of 27% in all-cause mortality15 and that muscle-strengthening activities for 30–60 minutes per week is associated with a 10%–20% reduction.16

Cardiorespiratory fitness and peak exercise capacity are associated with mortality. Peak exercise capacity is a better indicator of risk of death than established cardiovascular risk factors such as smoking, hypertension, and diabetes mellitus.17 A study examining cardiorespiratory fitness in older adults found dose-dependent reductions in mortality across all age groups (including participants aged 60–69, 70–79, and 80–95 yr).18 Substantial improvements (approximately 16%) in VO2max (an individual’s maximum rate of oxygen consumption, a strong indicator of mortality19) in older adults can occur with only 90 minutes of submaximal exercise per week over 16–20 weeks.20

Strength is also associated with reductions in all-cause mortality in older adults. A 2022 systematic review and meta-analysis found a linear inverse relation between handgrip strength and all-cause mortality up to sex-dependent thresholds (42 kg for men, 25 kg for women) in older adults.21 In their 2018 systematic review and meta-analysis, the authors found both handgrip and knee extension strength to be predictors of all-cause mortality in adults, with most of the studies examining adults older than 65 years.22 – Move more, age well: prescribing physical activity for older adults CMAJ January 27, 2025 197 (3) E59-E67; DOI: https://doi.org/10.1503/cmaj.231336

You must be logged in to post a comment.