Success

Not Everyone Gets Lucky

My interviews with Howard Marks, Chairman of Oaktree Capital, and famed for his “Chairman’s Memos,” were instructive.1 The first time he mentioned his good fortune, I pushed back, asking, “What about intelligence, hard work, and perseverance?”

His answer:

“Everybody in my MBA class at the University of Chicago was very smart and very hard working. But hard work and intelligence are mere table stakes. Not everybody has fortune smile on them; not everybody gets lucky.”

Serendipity: The Role of Luck in Your Life and Career – https://ritholtz.com/2026/06/recognize-the-role-of-luck-in-your-life-and-career/

The older you get you do develop a better understanding of luck and random events. Interesting article.

Not everyone gets lucky.

Study Failure to Learn Success

Michael Girdley on private equity:

The lesson is pretty straightforward. You’re going to go buy a business, and you’re going to look and say, “Where can I cut costs? How can I start to optimize and streamline this?” You can cut fat, but you definitely don’t want to cut muscle, and you don’t want to cut bone. That’s exactly what these guys did. Why did they do that? They’re private equity guys. They get paid on management fees and the deals when they turn around and put them out in the public. They don’t care about the long term. They care about the next three to five years, and that’s exactly what they optimized for.

How Not To Invest – A Lesson From The University of Chicago

CRSP’s origins date back to the 1960s. Its initial goal was to build a database of historical stock prices. This is harder than it might seem. Before trading was computerized, stock prices were maintained on paper. And when stocks split or companies merged, that added to the complexity.

Despite this seemingly dull mandate, CRSP has played an important role in the development of modern finance over the years. Most notably, the efficient market hypothesis and the capital asset pricing model were both made possible by CRSP data. And today, many of the world’s largest index funds, including Vanguard’s Total Stock Market Fund, are built on CRSP indexes. Endowment Lessons https://humbledollar.com/2026/02/endowment-lessons/

This article by Adam M. Grossman uses the University of Chicago’s financial struggles as a cautionary tale for individual investors.

Key Lessons for Individual Investors

- Spending: Avoid “Keeping Up with the Joneses”

- The university invested heavily in new buildings and programs to maintain its “eminence” without securing corresponding revenue.

- Takeaway: Financial success depends on income exceeding expenses. Operating costs of new assets (like large homes or complex projects) must be planned for in advance.

- Saving: Beware of Recency Bias

- During a 15-year market boom, the university ramped up debt rather than stockpiling resources.

- Takeaway: Investors often falsely assume current trends will continue forever. Use periods of market strength to re-balance portfolios and manage risk rather than increasing lifestyle or debt commitments.

- Investing: Complexity vs. Simplicity

- Performance: UChicago’s endowment returned 6.7% annually over 10 years, trailing a simple Vanguard Balanced Index Fund (VBIAX), which returned 8.2%.

- Liquidity: The university locked over 60% of its funds into illiquid assets like private equity and real estate, making it difficult to cover cash flow needs.

- Takeaway: High-fee, complex, and illiquid investments often under-perform simple index funds. If elite institutions with dedicated investment offices “are having second thoughts” about private equity, the message for individual investors seems clear.

This summary was produced by Gemini AI and edited by yours truly.

Here’s a link to an article on the sale of CRSP. Morningstar Completes Acquisition of CRSP and Extends Relationship with Vanguard https://newsroom.morningstar.com/news/news-details/2026/Morningstar-Completes-Acquisition-of-CRSP-and-Extends-Relationship-with-Vanguard/default.aspx

The Edge

My takeaways:

The first takeaway is about the mindset. Winning requires staying in the present. When you lose nearly half the points you play, the past offers no help. Dwelling on past mistakes only distracts from the real goal, which is to win the match. We cannot change what has happened, and we cannot control what comes next. Stay present, follow the process, and let the result take care of itself…The idea of edge applies directly to our lives. Life is made up of thousands of decisions taken over decades. A small edge in how we make those decisions quietly stacks the odds in our favor.

Take health. Lifting weights a few times a week, walking a few miles a day, eating reasonably well, and sleeping enough each give us a small edge. We are not competing with anyone else here. We are competing against chronic diseases. These habits do not guarantee outcomes, but they help us avoid most of the problems that are within our control, and leave the rest to chance. None of these decisions matter much on their own. Taken together over years they matter a lot.

Nice article, wonderful insights. Now go read the entire article.

Random Thoughts on Unretirement – 01.10.26

“We have to understand that anything in the past takes you out of the present moment. Anything in the future takes you out of the present moment.”

Zen Master Daigneault

To readers who are visiting this blog for the first time my posts on Random Thoughts About Retirement and Unretirement are written by an Old Guy who is old enough to be retired but isn’t retired and is still working. I had another birthday and the older I get the more I think about retirement. Back in 2023 I was thinking about what retirement for me would look like (see More Random Thoughts on Retirement – June 2023). But decisions such as this take serious thought and consideration. At first I thought I wanted to retire to a quiet life of blogging and writing my Future Best Seller titled The Man Who Had No Hobbies. After much thought I decided to add a short term goal to my retirement plan. My new short term goal is to avoid unretirement.

My RSS feed feeds me headlines on unretirement.

According to a new report from T. Rowe Price around 7% of retirees are looking for work in retirement, while 20% say they’re already working part time or full time…The two main reasons for coming back into the workforce are a tale of opposites. While 45% chose to work for social and emotional benefits… a slightly larger percentage — 48% — felt they needed to work for financial reasons.

Unretiring: More retirees are going back to work because they want to — or need to — https://finance.yahoo.com/news/unretiring-more-retirees-are-going-back-to-work-because-they-want-to–or-need-to-123203300.html

And this.

Once an eagerly awaited milestone, retirement is currently undergoing a transformative reevaluation. Traditionally seen as a well-deserved period of rest and relaxation, the dream of early retirement is now being challenged by a new perspective – that of embracing lifelong work. This paradigm shift reflects the changing nature of work, increased life expectancy, and the desire for personal fulfillment.

Rethinking Retirement: The Case for Embracing Lifelong Work — https://due.com/rethinking-retirement-the-case-for-embracing-lifelong-work/

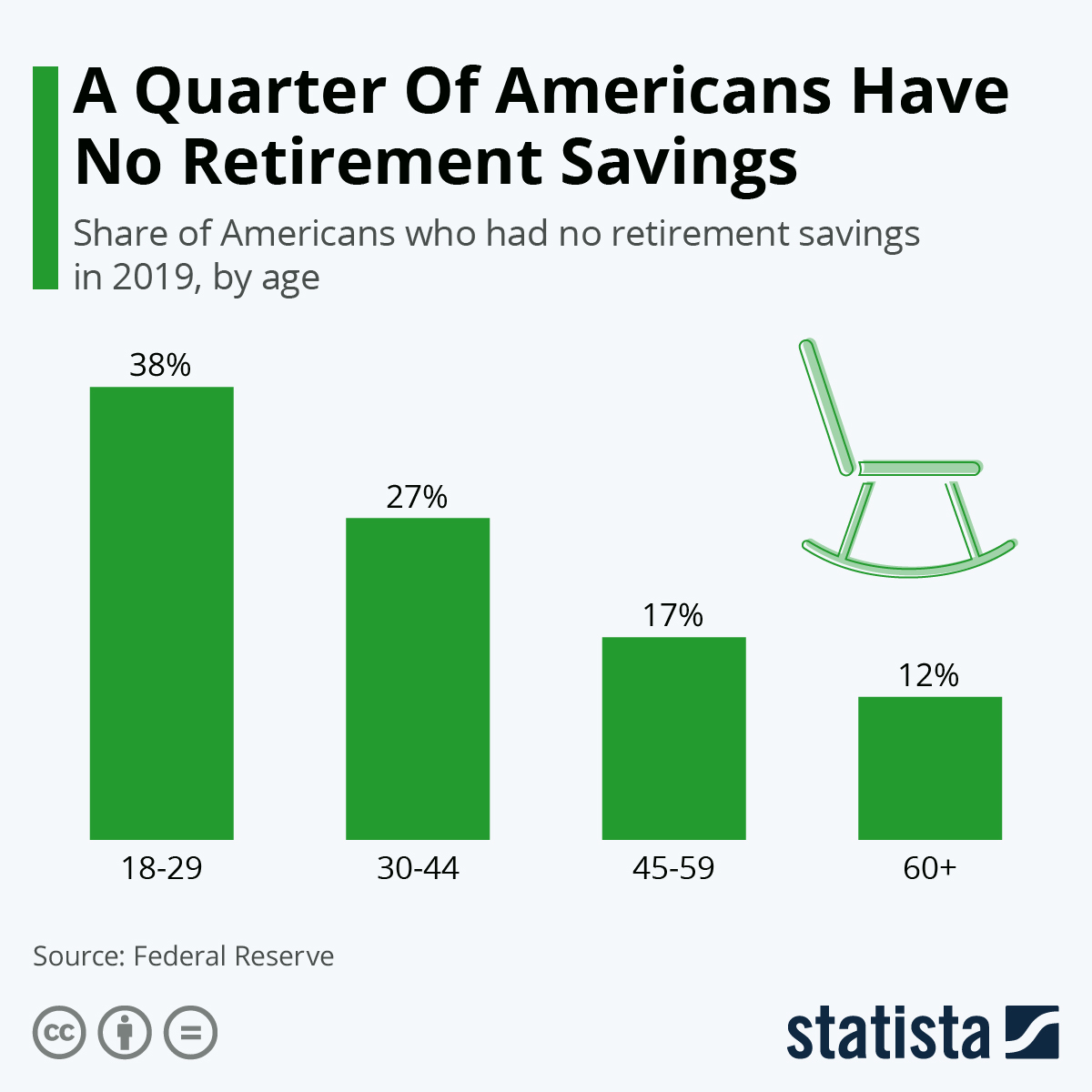

The reality is many won’t have a choice. The following chart illustrates retirement savings as of 2019.

Americans are having trouble financially preparing themselves for life after work. A recent Federal Reserve report found that nearly a quarter of U.S. adults have absolutely no retirement savings or pension. Even though the level of preparation increases as people get older, concern about inadequate savings is still readily apparent across all age groups, even older people in their 60s.

A Quarter Of Americans Have No Retirement Savings — https://www.statista.com/chart/18246/share-of-americans-who-have-no-retirement-savings/

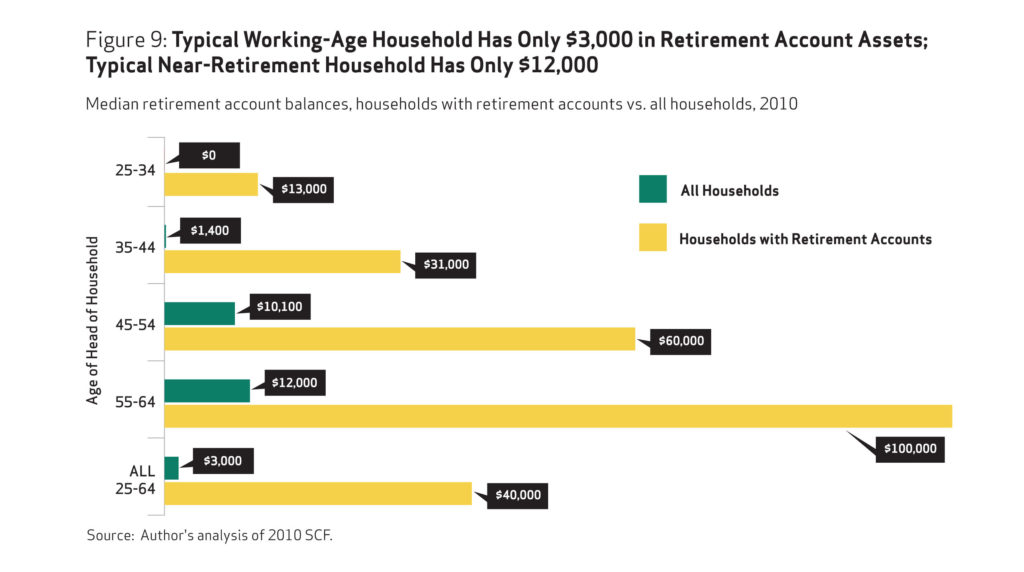

OOPS. I’m glad I didn’t click the Publish button. The savings situation appears to be worse than I thought. The study below was an analysis of data from 2010!

The study broadly examines how American households are faring in relation to retirement savings targets recommended by some financial services firms. It uses the Federal Reserve’s Survey of Consumer Finances to analyze retirement plan participation, savings, and overall assets of all U.S. households age 25 to 64, not just those with retirement account assets. This is important because some 45 percent, or 38 million working-age households, do not have any retirement account assets.

The average working household has virtually no retirement savings. When all households are included— not just households with retirement accounts—the median retirement account balance is $3,000 for all working-age households and $12,000 for near-retirement households. Two-thirds of working households age 55-64 with at least one earner have retirement savings less than one times their annual income, which is far below what they will need to maintain their standard of living in retirement.

The findings confirm that the American Dream of retiring comfortably after a lifetime of work will be impossible for many. Based on 401(k)–type account and IRA balances alone, some 92 percent of working households do not meet conservative retirement savings targets for their age and income. Even when counting their entire net worth, 65 percent still fall short.

The Retirement Savings Crisis: Is It Worse Than We Think? — https://www.nirsonline.org/reports/the-retirement-savings-crisis-is-it-worse-than-we-think/

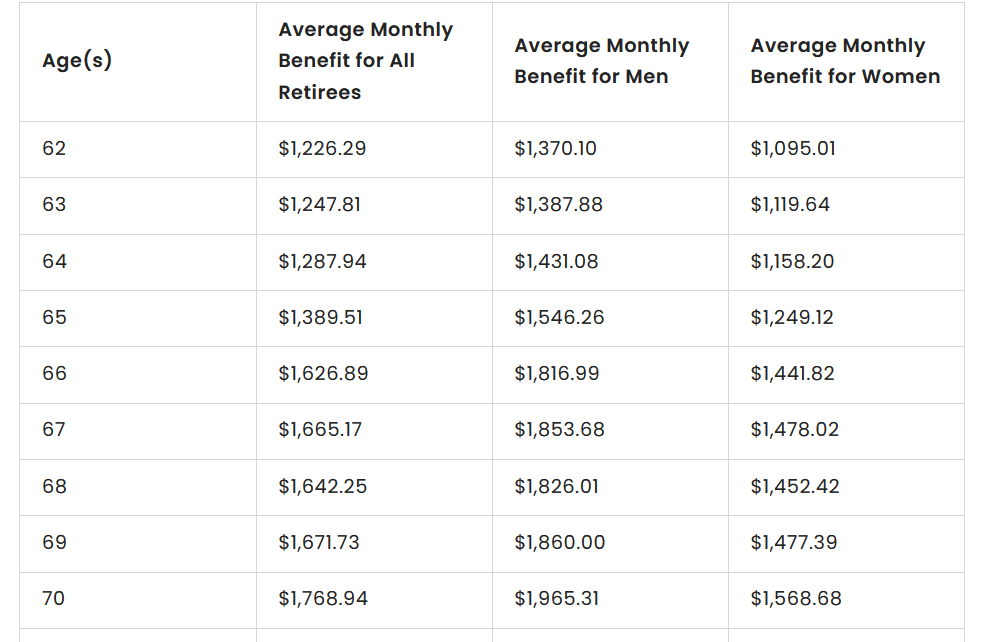

So how will you afford retirement without any savings? Don’t look to Social Security. Here’s some numbers on average Social Security payments. The full chart at the source website goes up to age 100.

As of December 31, 2021, the average Social Security payment for all retirees was $1,658.03 a month, according to the Social Security Administration’s Annual Statistical Supplement for 2022. For men, the overall average was $1,838.08. For women, the average was $1,483.75 — a difference of $354.33 per month.

Here’s the Average Social Security Check for Men vs. Women — https://www.gobankingrates.com/retirement/social-security/average-social-security-check-men-women/

I’ve previously advised everyone to Save as Much as You Can Because Whatever You Manage to Save Will Never Be Enough – Random Thoughts on Retirement. Now here’s my second piece of sage advice: keep working so you don’t have to unretire.

Whether people unretire or simply stay in the workforce longer, some of the largest financial benefits of additional years of work are delaying retirement account withdrawals and delaying claiming Social Security benefits. These actions essentially shorten the amount of time your assets will need to support you in retirement. Even a few additional years of income have a positive effect on the probability that you won’t outlive your funds.

“Unretiring”: Why Recent Retirees Want to Go Back to Work — https://www.troweprice.com/personal-investing/resources/insights/unretiring-why-recent-retirees-want-to-go-back-to-work.html

Whew. Long post. Longer than I anticipated. If you made it this far, congratulations!

Double OOPS. Hit the publish button too soon. Postscript.

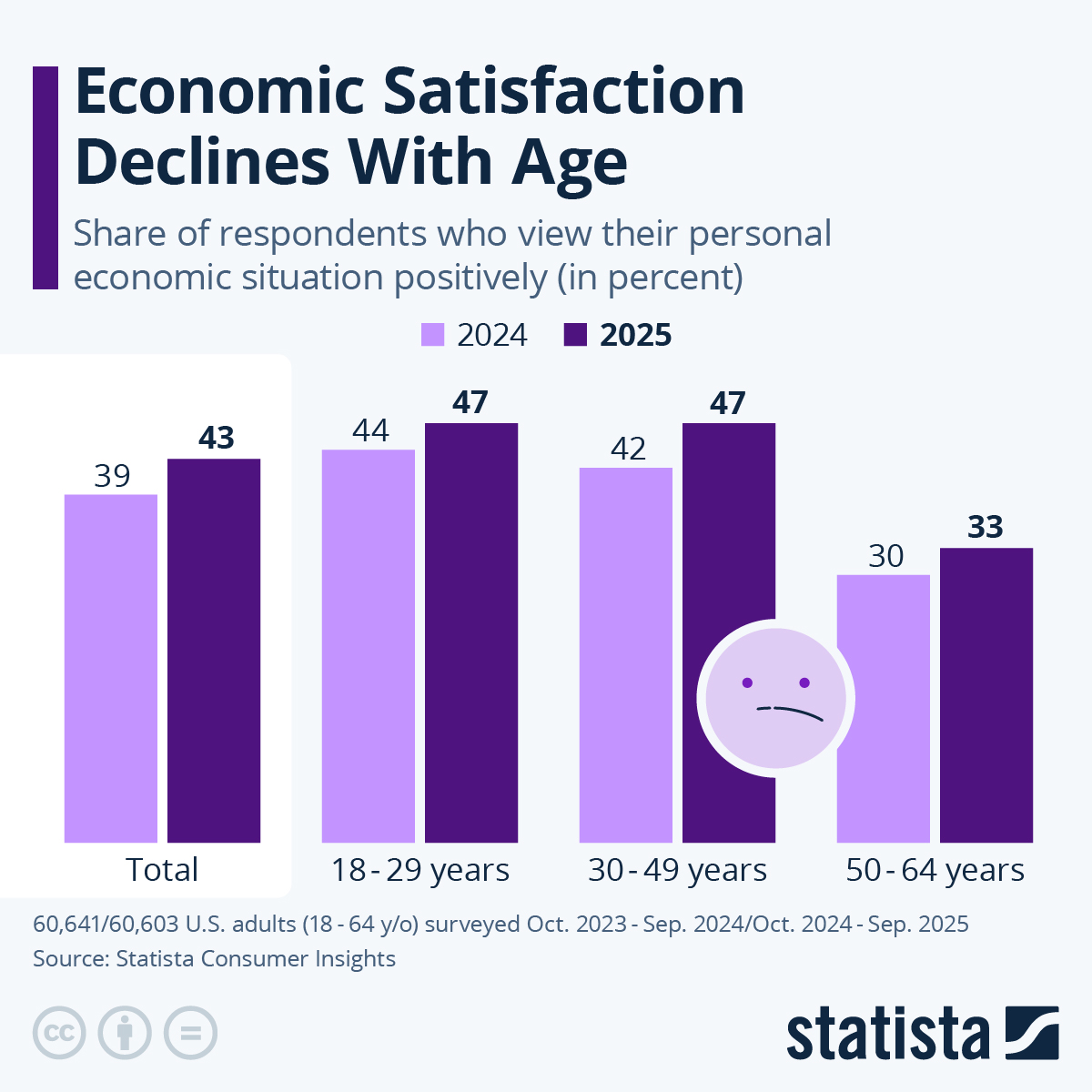

Economic Satisfaction Declines With Age – https://www.statista.com/chart/35656/us-respondents-who-view-their-financial-situation-positively/

Note the survey respondents’ age stops at 64.

The Gift of Work

It’s a book.

The Gift of Work: Overcoming Workplace Burnout and Finding Satisfaction in Your 9-to-5 by Tarthang Tulka.

Read about Tarthang Tulka at https://www.buddhanet.net/masters/tarthang-rinpoche/

Now read the book. You’re welcome.

Nonrandom Thoughts on Retirement – Nov. 2024 (scary chart too)

Americans are split over the state of the American dream — https://www.pewresearch.org/short-reads/2024/07/02/americans-are-split-over-the-state-of-the-american-dream/

Are you familiar with the self-fulfilling prophecy in psychology/sociology? Simply stated a self-fulfilling prophecy occurs when what you believe about your future causes it to happen. When you believe something will become true, you’ll act to make it a reality. Look at the chart above. Looks like around 50% of the survey respondents under the age of 50 will never achieve their American Dream.

They will make choices and act in ways to ensure they will never achieve the American Dream.

Why I am a Life Underwriter (Take a Break 09.20.24)

Because God said NO you’re an underwriter. Philip will play the blues.

I take solace in the fact that Philip would not be able to underwrite a life insurance application to save his life.

You must be logged in to post a comment.