We plan for the money. We don’t plan for the Monday morning when no one needs you to be anywhere.

Julianne Holt-Lunstad, a professor of psychology and neuroscience at Brigham Young University, published a landmark meta-analysis in 2015 involving over 3.4 million participants. Her finding: social isolation increases the risk of premature death by 26%, and loneliness by 29%. Those numbers rival the health impact of smoking fifteen cigarettes a day. We treat smoking as a public health crisis. We treat retirement loneliness as a personal failing.

Though the traditional retirement age in the U.S. typically falls between 62 and 67, many Americans continue working beyond that point. As of 2024, slightly more than 22% of adults aged 65 and older are still employed, either full-time or part-time. Though the traditional retirement age in the U.S. typically falls between 62 and 67, many Americans continue working beyond that point. As of 2024, slightly more than 22% of adults aged 65 and older are still employed, either full-time or part-time. – https://financebuzz.com/working-in-retirement-data

So I’m not the only Old Guy who is still working past age 65.

Curiosity is not a curse. I’ve been expanding my knowledge base this morning.

As I have written before, the key to treating chronic pain often lies in therapies designed to dampen the brain’s response to pain signals. In treating my own chronic pain, I benefited greatly from a mindfulness therapist who helped me develop techniques to redirect thoughts and feelings of pain, push them out of my body. In my case, I met virtually with the therapist, who expertly sussed out my situation and tailored her advice to my needs. She worked at Duke University, in one of their pain clinics, and was an expert at helping people like me. This Online Program Could Be The Solution To Your Chronic Pain – https://www.forbes.com/sites/peterubel/2026/02/07/this-online-program-could-be-the-solution-to-your-chronic-pain/

Here’s the link to Telehealth and Online Cognitive Behavioral Therapy–Based Treatments for High-Impact Chronic Pain A Randomized Clinical Trial – https://jamanetwork.com/journals/jama/fullarticle/2836795Conclusions and Relevance Remote, scalable CBT-CP treatments (delivered either via telehealth or self-completed modules online) resulted in modest improvements in pain and related functional/quality-of-life outcomes compared with usual care among individuals with high-impact chronic pain. These lower-resource CBT-CP treatments could improve availability of evidence-based nonpharmacologic pain treatments within health care systems.

I’ve had chronic pain since 1976 (or was it 1977?) when I had a near fatal encounter with a fast moving car while walking home. I don’t take any pain medications other than the occasional ibuprofen. I have been using an online pain management resource courtesy of my employer (not the resource linked above). A DPT (Doctor of Physical Therapy) and health coach are part of the resources at my disposal. I haven’t used any ibuprofen in quite some time, if that tells you anything.

“We have to understand that anything in the past takes you out of the present moment. Anything in the future takes you out of the present moment.”

Zen Master Daigneault

To readers who are visiting this blog for the first time my posts on Random Thoughts About Retirement and Unretirement are written by an Old Guy who is old enough to be retired but isn’t retired and is still working. I had another birthday and the older I get the more I think about retirement. Back in 2023 I was thinking about what retirement for me would look like (see More Random Thoughts on Retirement – June 2023). But decisions such as this take serious thought and consideration. At first I thought I wanted to retire to a quiet life of blogging and writing my Future Best Seller titled The Man Who Had No Hobbies. After much thought I decided to add a short term goal to my retirement plan. My new short term goal is to avoid unretirement.

My RSS feed feeds me headlines on unretirement.

According to a new report from T. Rowe Price around 7% of retirees are looking for work in retirement, while 20% say they’re already working part time or full time…The two main reasons for coming back into the workforce are a tale of opposites. While 45% chose to work for social and emotional benefits… a slightly larger percentage — 48% — felt they needed to work for financial reasons.

Once an eagerly awaited milestone, retirement is currently undergoing a transformative reevaluation. Traditionally seen as a well-deserved period of rest and relaxation, the dream of early retirement is now being challenged by a new perspective – that of embracing lifelong work. This paradigm shift reflects the changing nature of work, increased life expectancy, and the desire for personal fulfillment.

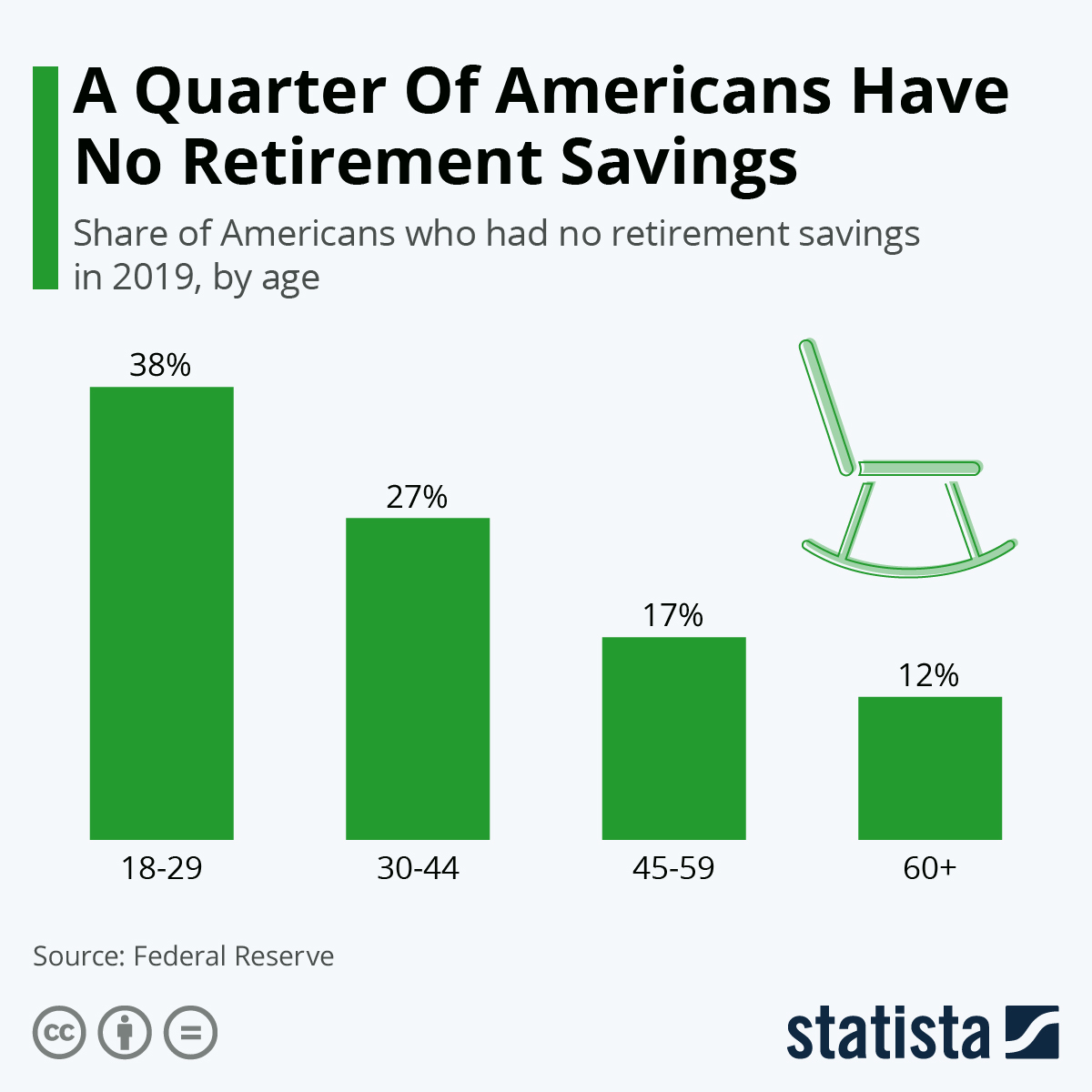

The reality is many won’t have a choice. The following chart illustrates retirement savings as of 2019.

Americans are having trouble financially preparing themselves for life after work. A recent Federal Reserve report found that nearly a quarter of U.S. adults have absolutely no retirement savings or pension. Even though the level of preparation increases as people get older, concern about inadequate savings is still readily apparent across all age groups, even older people in their 60s.

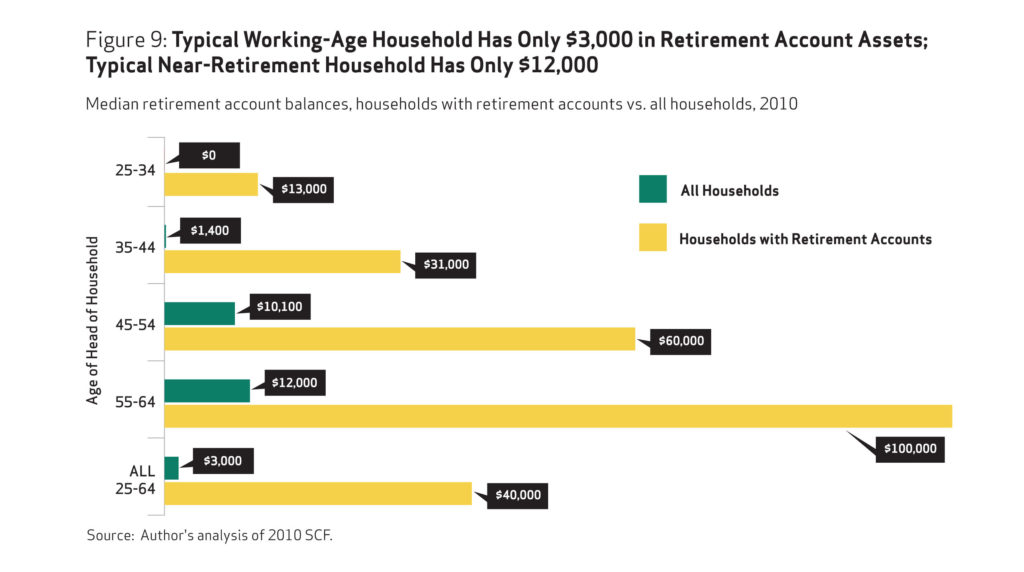

OOPS. I’m glad I didn’t click the Publish button. The savings situation appears to be worse than I thought. The study below was an analysis of data from 2010!

The study broadly examines how American households are faring in relation to retirement savings targets recommended by some financial services firms. It uses the Federal Reserve’s Survey of Consumer Finances to analyze retirement plan participation, savings, and overall assets of all U.S. households age 25 to 64, not just those with retirement account assets. This is important because some 45 percent, or 38 million working-age households, do not have any retirement account assets.

The average working household has virtually no retirement savings. When all households are included— not just households with retirement accounts—the median retirement account balance is $3,000 for all working-age households and $12,000 for near-retirement households. Two-thirds of working households age 55-64 with at least one earner have retirement savings less than one times their annual income, which is far below what they will need to maintain their standard of living in retirement.

The findings confirm that the American Dream of retiring comfortably after a lifetime of work will be impossible for many. Based on 401(k)–type account and IRA balances alone, some 92 percent of working households do not meet conservative retirement savings targets for their age and income. Even when counting their entire net worth, 65 percent still fall short.

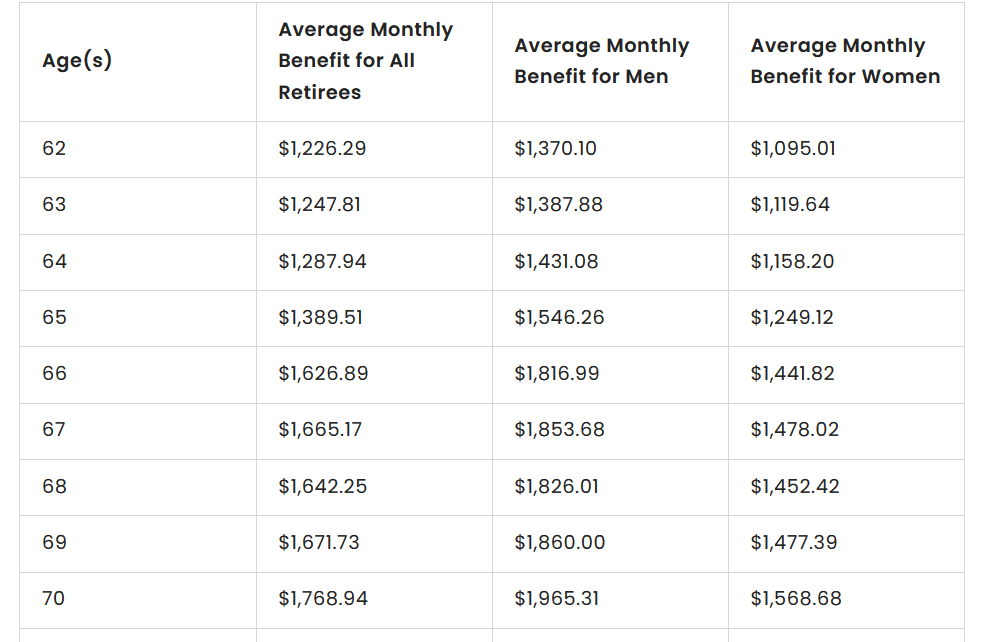

So how will you afford retirement without any savings? Don’t look to Social Security. Here’s some numbers on average Social Security payments. The full chart at the source website goes up to age 100.

As of December 31, 2021, the average Social Security payment for all retirees was $1,658.03 a month, according to the Social Security Administration’s Annual Statistical Supplement for 2022. For men, the overall average was $1,838.08. For women, the average was $1,483.75 — a difference of $354.33 per month.

Whether people unretire or simply stay in the workforce longer, some of the largest financial benefits of additional years of work are delaying retirement account withdrawals and delaying claiming Social Security benefits. These actions essentially shorten the amount of time your assets will need to support you in retirement. Even a few additional years of income have a positive effect on the probability that you won’t outlive your funds.

lifeunderwriter.net is a personal WordPress.com blog run by an experienced life insurance underwriting professional (the author uses the handle “SupremeCmdr” and has been posting since at least 2008).

The site’s tagline is “Curated Content From a Life Underwriting Professional”. It primarily features:

Curated links to external articles, studies, and news items

Commentary and personal reflections from the author’s perspective as someone who has worked in life insurance underwriting (assessing mortality risks, medical records, risk classification for policies, etc.)

Insights related to the insurance industry, mortality trends, health/longevity topics (e.g., vitamin D in older adults, obesity treatments, nutrition, diabetes risks), retirement planning (e.g., deferring Social Security), remote work in insurance, and occasional broader thoughts on society, technology, or resilience

The content often ties back to how various medical, lifestyle, or demographic factors might influence underwriting decisions in life insurance, but it has evolved over time into a more eclectic mix. Recent posts (including into 2025) frequently cover:

Health and nutrition (e.g., protein’s role in diets, GLP-1 drugs, probiotics)

Personal anecdotes (cooking recipes, music like Pat Metheny)

Retirement and aging commentary

Industry observations (e.g., older workers, AI’s effects)

The blog is not a commercial service site offering underwriting services (an older page mentions “Underwriting Solutions LLC” from around 2006–2017, but those appear to be in hibernation or discontinued). It functions more as a personal journal / link blog than a formal resource or forum.

It remains active with regular (sometimes frequent) posts, though the style is informal, opinionated, and not strictly professional/academic. If you’re in the life insurance field or interested in mortality/longevity topics through an underwriter’s lens, it can offer interesting curated reading; otherwise, it’s a niche personal blog.

It has evolved over time into a more eclectic mix?

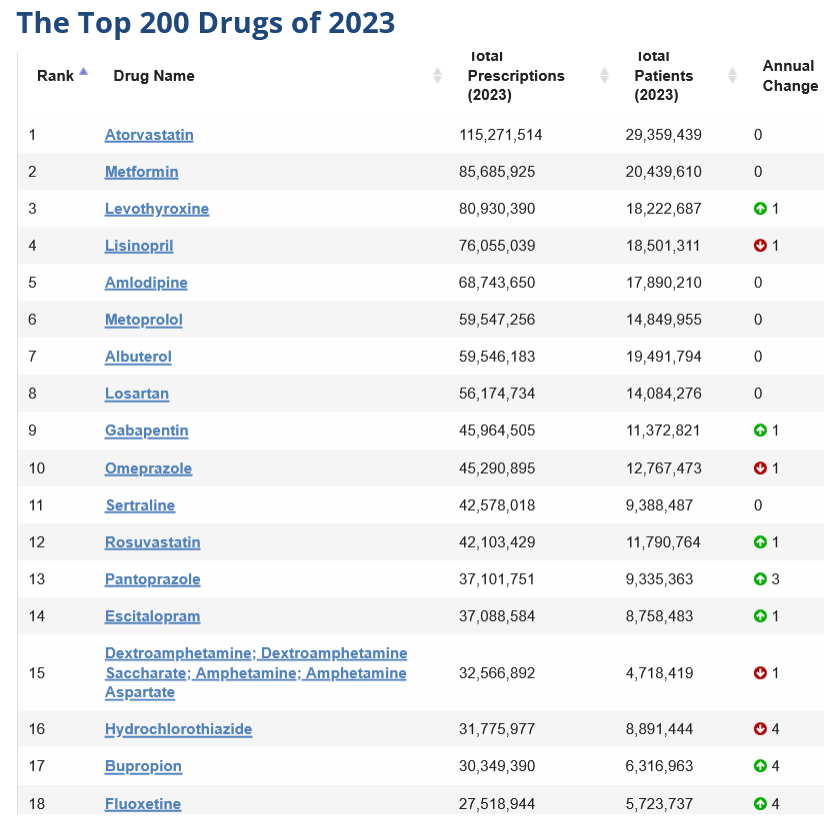

According to the USP, the bulk of the APIs come from India. That country is responsible for 50% of the active pharmaceutic ingredients. China is not far behind at 32%. The European Union supplies 10%. That’s a big change since 2000. Back then, European countries like France, Germany, Switzerland and Denmark supplied 42% of the APIs. Drug Recalls From India – Can You Trust Foreign-Made Generics? – https://www.peoplespharmacy.com/articles/more-drug-recalls-from-india-do-you-trust-foreign-made-generics

Dozens of companies received approval from the FDA over the years to sell metoprolol and bupropion in the U.S. Yet from 2018 to 2024, the agency reported running only 2 tests on metoprolol and 7 on bupropion through its quality surveillance program — in each case, by pulling a sample from a single drug maker. In many of those years, the drugs weren’t tested at all, FDA records show. Those that were assessed received passing results. The FDA Often Doesn’t Test Generic Drugs for Quality Concerns, So ProPublica Did – https://www.propublica.org/article/fda-generic-drug-testing

Through November, employers have announced 1,170,821 job cuts, an increase of 54% from the 761,358 announced in the first eleven months of last year. Year-to-date job cuts are at the highest level since 2020 when 2,227,725 cuts were announced through November. It is the sixth time since 1993 that job cuts through November have surpassed 1.1 million. Challenger Report: 71,321 Job Cuts on Restructurings, Closings, Economyhttps://www.challengergray.com/blog/challenger-report-71321-job-cuts-on-restructurings-closings-economy/

Yikes.

In my less than illustrious career I’ve suffered 100% reductions in income multiple times. Hopefully the newly unemployed have some form of a fallback plan.

Lifeunderwriter.net is a blog mainly focused on topics related to life underwriting in the insurance sector. It covers various aspects of the underwriting process, success tips for professionals, and insights into the life insurance industry.

Key Features of the Blog

Curated Content: The blog displays curated content from a life underwriting professional aimed at sharing knowledge and resources.

Topics Covered: Posts may include discussions on underwriting practices, medical news relevant to underwriters, career tips, and personal insights about the industry.

Regular Updates: The blog has been active for several years, with posts dating back to 2008, and it appears to encourage subscriber engagement.

Recent Posts and Themes

Recent entries suggest a mix of industry insights and personal reflections. Topics range from the impact of emerging trends in underwriting to the importance of keeping updated with medical advancements.

If you’re interested in specific articles or themes from the blog, let me know!

Lifeunderwriter.net is a personal WordPress blog titled “Curated Content From a Life Underwriting Professional.” It features reflective commentary, curated articles, and personal anecdotes written by an anonymous life underwriting expert (someone with over 15 years of remote work experience in the field). The content spans topics related to health, longevity, demographics, lifestyle, risk assessment, retirement planning, nutrition, and broader societal issues like AI’s impact on critical thinking or remote work trends.

Key Features and Content

Blog Posts: Entries date back to at least 2008 and include recent ones from 2024–2025. Examples include discussions on vitamin D supplementation for older adults, coffee’s link to atrial fibrillation, Social Security finances, cognitive disabilities tied to income/education, and personal reflections on retirement or resilience.

Themes: Heavily influenced by the author’s professional background in life insurance underwriting (e.g., assessing mortality risks, medical summaries for policies), but it extends to non-professional topics like cooking recipes, music (e.g., Pat Metheny), or even cheese production history.

Style: Informal and opinionated, with embedded links to external studies, charts, images, and disclaimers. It’s not a commercial site—no services are actively offered, though older posts (e.g., from 2017) mention “hibernating” outsourced underwriting services like attending physician statement summaries.

Audience and Purpose

The blog targets readers interested in a underwriter’s unique lens on aging, mortality, and wellness—think professionals in insurance, finance, or health, plus general audiences curious about evidence-based life hacks. It’s more of a personal journal than an authoritative resource, emphasizing work-life balance (e.g., the author’s low-stress remote setup since ~2006) and long-term planning like deferring Social Security to age 70.

No direct contact info is listed, but it’s hosted on WordPress.com for easy following. If you’re in life insurance, it might resonate with underwriting pros navigating industry shifts like accelerated processes during COVID-19.

The Boss (SWMBO) and I talk about this often. Once the W2 income stops and we have to rely upon a small corporate pension, savings, and a shaky Social Security promise we’ll have to get conservative on our spending. No more Stratocasters. Less purchases for wardrobe enhancements. Gas station beer instead of craft brews.

I started writing my journal in 2005. One of the best things about keeping a journal is the ability to verify if memories from the past are accurate or the made up, mashups your brain creates as memories. Here’s my entry on Monday July 24 2006:

A 4:00 PM meeting with the Division head with an HR rep present is never a good thing. I immediately thought to myself:

“This is gonna suck.”

And it did, big time. I got whacked today.

And that’s how my WFH life began. When my work from home situation arises in conversation most are surprised to learn I’ve been WFH this long. I’m surprised how long I’ve been working from home!

I am convinced due to having a low stress working environment, better diet (NO office snacks/free food/lunches out), no commute, along with a host of other variables I just might be increasing my lifespan. I do know I get plenty of sleep on a regular routine basis.

Short sleep duration (< 7 h per night) was associated with a 14% increase in mortality risk compared to the reference of 7–8 h, with a pooled hazard ratio of 1.14 (95% CI 1.10 to 1.18). Conversely, long sleep duration (≥ 9 h per night) was associated with a 34% higher risk of mortality, with a hazard ratio of 1.34 (95% CI 1.26 to 1.42). Sex-specific analyses indicated that both short and long sleep durations significantly elevated mortality risk in men and women, although the effect was more pronounced for long sleep duration in women. Both short and long sleep durations are associated with increased all-cause mortality, though the degree of risk varies by sex. Imbalanced sleep increases mortality risk by 14–34%: a meta-analysis – Ungvari, Z., Fekete, M., Varga, P. et al. Imbalanced sleep increases mortality risk by 14–34%: a meta-analysis. GeroScience47, 4545–4566 (2025). https://doi.org/10.1007/s11357-025-01592-y

You must be logged in to post a comment.