Keep moving people. Nothing to see here.

Intuit to lay off 1,800 employees, labels 1,050 as ‘underperformers’

YIKES.

Keep moving people. Nothing to see here.

Intuit to lay off 1,800 employees, labels 1,050 as ‘underperformers’

YIKES.

I wish upon you ample doses of pain and suffering.

Nvidia CEO Jensen Huang

I post things online because I find them interesting. Sometimes I post things online as a part of my collection of Electronic Sticky Notes, a reminder to myself to try a new recipe like https://spainonafork.com/my-mothers-lentil-stew-with-sweet-potatoes-recipe or as in this case a reminder to go back and listen to the entire interview when I have time. The first five minutes of this video taught me something I never knew about product positioning. The interview is over an hour long so I want to watch and listen in bite size chunks.

My favorite excerpt from the letter:

Let’s be honest, some people in academia are horrible, arrogant, selfish and narcissistic. And no matter how much the people at the top say they deal with bad behaviour, the nasty folk do have an annoying habit of getting promoted. The way in which academia selects and rewards particular skill sets produces an over-concentration of people who are low on empathy. I’ve met a lot of those ‘special’ colleagues over the years (no names mentioned obviously). I will not miss them one jot. They create a toxic working environment , dominate the discourse, ride roughshod over the rules, and cause a great deal of harm to others and get away scot-free. They’ve done me significant mental damage, but I can now happily forget them and move on with life.

My recommendation to anyone starting out in academia is stand your ground, challenge these energy vampires and politely make it clear that you don’t want to play their stupid toxic games. They really don’t have the power that they want you to believe they have, even though the system tends to promote them to roles that are beyond their emotional competence to fulfill. Pity them for the lack of other things to do with their lives. And, remember that 98% of what we do as academics is of no importance at all out there in the real world, so when a self-entitled colleague insists that their work on their favourite gene is earth-shattering; more important than anything you could ever do; and a good reason for their career to be advanced faster than yours; just smile and ignore them. Do your own thing, at your own pace. Have a life outside the university and remember that it’s just a job.

https://journalofhumannutritionanddieteticseditor.wordpress.com/2023/11/27/thats-it/

Every employee probably knows the difference between productive work and what a new report by software company Slack calls performative work – merely looking but not actually being busy. The data in the release shows that workers in some Asian countries – namely India, Japan and Singapore – seem to spend more time appearing to be working than employees in other places.

While Indians spent 43 percent of time in performative work, that number was 37 and 36 percent in Japan and Singapore, respectively. For comparison, U.S. respondents and those from Germany said they only appeared busy for 28 and 29 percent of the time. One outlier in Asia was South Korea, also with a low of 28 percent of work hours spent in “pretend mode”.

Who’s Only Looking Busy at Work? — https://www.statista.com/chart/30591/performative-productive-work/

And now we have a new productivity mantra…

Now that you’ve taken a break and worked on the root causes of your problem, it’s time to embrace a whole new mindset around work, money, and success. This is going to sound radical, but I want you to give yourself permission to achieve less.

The latest productivity mantra that we all need: ‘Achieve less’ — https://fortune.com/2023/08/16/latest-productivity-mantra-achieve-less-careers-mental-health-stress/

But The Boss may not agree with this new mantra…

While the debate over productivity in a remote office setting continues, one Australian woman is fighting back against her employer after being accused of not typing enough while working remotely.

Remote Employee Fired for ‘Low Keystroke Activity’ During Working Hours After 18 Years of Employment — https://www.entrepreneur.com/business-news/remote-worker-fired-for-low-keystroke-activity/457578

There’s a new description of the ideal job…

A lazy-girl job is any job that can be done from home within the standard 9-to-5 and has undemanding tasks and easygoing managers.. the jobs pay enough money ($60,000 to $80,000) for a young adult to live off but not feel pressure to work above their contracted hours.”

The term was coined in May 2023 by Gabrielle Judge, a 26-year-old career influencer. Judge told The Wall Street Journal that she was aware the word lazy would have a negative connotation, but she wanted to spark a conversation. “Lazy-girl jobs aren’t roles where you can slack off,” she said, “but career paths where your work-life balance should feel so awesome that you almost feel like you’re being lazy.”

Lazy-Girl Jobs Are Trending with Gen Z—Here’s How to Find One — https://www.rd.com/article/lazy-girl-jobs/

“Lazy-girl job” is one of the worse uses of the English language I’ve encountered because the use of the word “lazy” is bad. Really bad. The definition of any job done from home with undemanding tasks and easygoing managers is also bad. Really, really bad. A friend once told me the key to his success. With most jobs and careers the majority of us will be average performers (think bell curve). All you need to do to put yourself on the path to success is to be a little better than average. This lazy girl job thing is cultural acceptance of average or worse than average.

Working hard is not a guarantee of success. But not working hard is a guarantee of failure.

Same graphic, slightly larger.

Never present yourself than anything other than your true self.

I’m actually not WFH (working from home) today but reading about WFH. And I learned some new things about the world today. One of my favorite tidbits of unsolicited advice comes in the form of this question:

Do you live to work or work to live?

As Gartner research shows, workers want a more “human value proposition,” with 65% of survey respondents agreeing that the pandemic made them rethink the role that work should have in their lives. For all of our talk for decades about work-life balance, people finally feel in their bones what that means. The big question has shifted from “How does life fit into work?” to “How does work fit into life?”

How to Motivate Employees When Their Priorities Have Changed — https://hbr.org/2023/05/how-to-motivate-employees-when-their-priorities-have-changed

Nice to see others coming around to my way of thinking. The strongest motivation I had to establishing a WFH life was to not have work dominate my entire life. Not once have I felt lonely working in my home office. But apparently some WFH people get lonely.

When I first made the switch to working remotely, I was elated. I had been commuting for years, which regularly constituted 12 or more hours stuck in traffic each week and resulted in incalculable levels of stress and frustration. When I began working from home, in addition to regaining my lost commuting hours, I loved my new ability to focus on my work without the distraction of an open-plan office environment.

However, as time progressed, I started to feel lonely. I was able to laser-focus on my work, but my interactions with others were driven solely by virtual meeting agendas or email. I noticed I was becoming less enthused and more withdrawn. I spent too much time scrolling social media because I was silently craving connection with others. I was slowly but steadily becoming isolated.

Is Your Remote Job Making You Lonely? — https://hbr.org/2023/05/is-your-remote-job-making-you-lonely

Maybe you should turn your camera on during meetings.

A recent survey of 4,200 work-from-home employees found that 49% report a positive impact from engagement when their cameras are on during online meetings, and only 10% felt disengagement from turning on cameras. As leaders are figuring out hybrid and remote work, they are facing the challenge of deciding whether to encourage employees to keep their cameras on during meetings. This decision has a significant impact on communication, engagement and trust-building within the team. I can attest to that from my experience helping 21 organizations transition to long-term hybrid work arrangements.

The Pros and Cons of ‘Cameras On’ During Virtual Meetings — https://www.entrepreneur.com/leadership/the-pros-and-cons-of-cameras-on-during-virtual-meetings/450959

Then again, there may be a good reason why people have their cameras off.

A May 2022 study by the Federal Reserve Bank of Atlanta estimates that the number of working age Americans (25 to 54 years old) with substance use disorders has risen by 23% since pre-pandemic, to 27 million. A figure that’s about one in six of people who were employed around the time of the study. It’s caused a 9% to 26% drop in labor force participation that Karen Kopecky, one of the authors of the report, says continues today.Drug recovery firm Sierra Tucson concluded from a November 2021 survey that about 20% of US workers admitted to using recreational drugs while working remotely, and also to being under the influence during virtual meetings. Digital recovery clinic Quit Genius found in August 2022 that one in five believe that substance use has affected their work performance, also according to a survey.

Remote workers with substance use disorders face ‘rude awakening’ in return-to-office mandates — https://fortune.com/2023/05/13/remote-workers-substance-use-disorders-return-to-office-mandates/

OK, enough about WFH. Time to get back to thinking about retirement because (I am) Flunking Retirement.

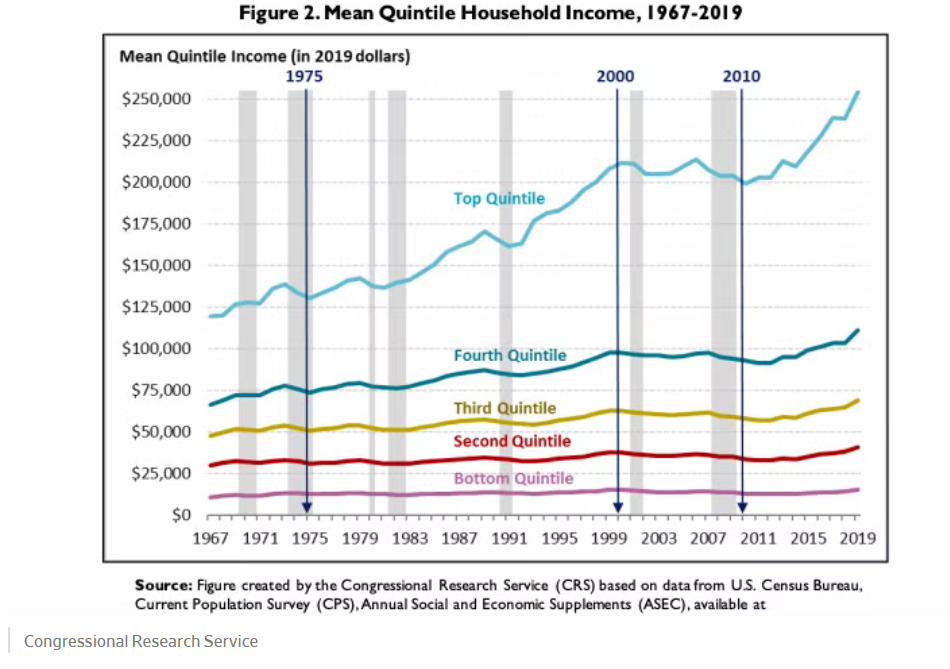

Per the Economic Policy Institute, wages in 2021 “rose fastest for the top 1% of earners (up 9.4%) and top 0.1% (up 18.5%), while those in the bottom 90% saw their real earnings fall 0.2% between 2020 and 2021.”

I Would Love to Have Enough Time and Money to Go to an Office to Work All Day — https://slate.com/business/2023/03/steven-rattner-new-york-times-remote-work-commute-child-care.html

The source article is about WFH vs RTO (work from home vs return to office) and is worth reading.

Nonprofit hospital and health plan operator Kaiser Permanente on Friday posted a $4.5 billion net loss in 2022, compared to a $8.1 billion net gain in 2021, as the integrated system struggled with billions of dollars in investment losses, a rise in care volume and ongoing labor shortages.

Kaiser’s $4.5B loss in 2022 driven by labor expenses, investment losses — https://www.healthcaredive.com/news/kaiser-reports-13b-operating-loss-2022-driven-by-expenses-inflation/642595/

Yikes.

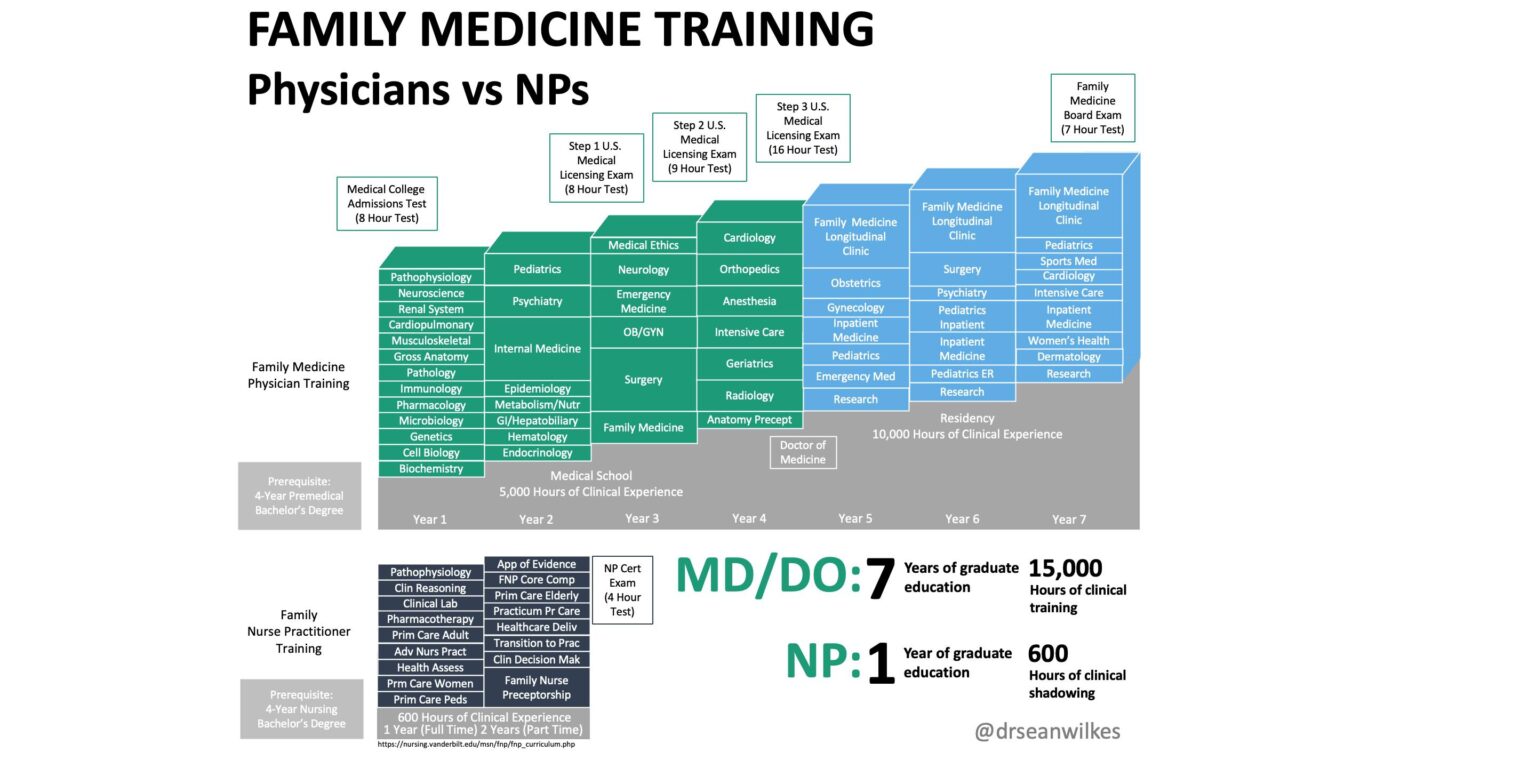

There are about 940,000 real doctors in the US and 12% of them quit last year. That’s a lot.

117,000 Doctors Left Their Jobs in 2021 — Authentic Medicine

For a deeper dive read this article https://www.advisory.com/daily-briefing/2022/10/25/workplace-departures

You must be logged in to post a comment.