Again, you can’t connect the dots looking forward; you can only connect them looking backward. So you have to trust that the dots will somehow connect in your future. You have to trust in something — your gut, destiny, life, karma, whatever. This approach has never let me down, and it has made all the difference in my life.

Sometimes things in life work out as planned. Sometimes they don’t. This time the plan is going as planned. At my annual wellness check up everything turned out fine except for my blood pressure. The two readings taken showed an elevated systolic and per Doctor’s orders I had to buy a BP machine which set me back $36 plus tax. I was instructed to keep a log for two weeks. For grins, I checked my online account to see what Dr. Lewis wrote for the office visit notes. No mention whatsoever regarding my BP readings. Probably because both of us felt this wasn’t a huge problem. The Boss started showing some concern and I had to report my pressures to her every day. Again I felt this wasn’t a worrisome medical issue. Besides if the diagnosis was hypertension I was looking at daily Lisinopril 10 mg, no big deal.

After two weeks I sent Dr. Lewis my log. She replied later that day.

Thank you for diligently keeping track of your blood pressure readings. I see that your readings have been fairly consistent. Yes you can stop watching it. If you feel fatigued or headaches please recheck it.

Sincerely, KL

I survived another annual wellness check. The Road to 70 is still pretty smooth. But the ride is not as smooth for others.

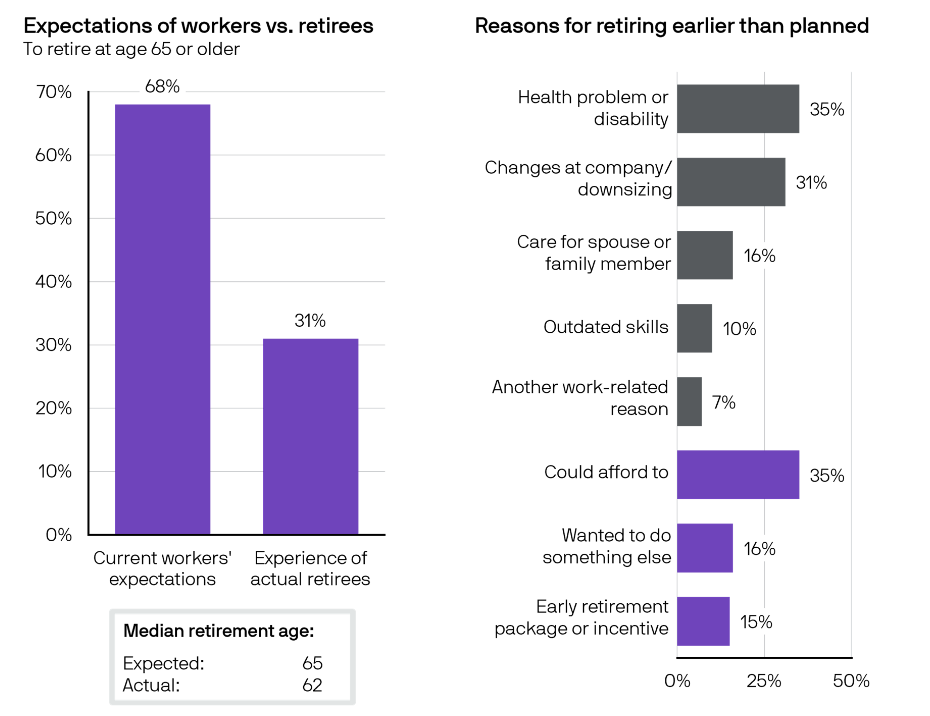

A CivicScience survey of nearly 3,000 respondents conducted between March and May 2024 reported 61% of those aged 55 and over say they won’t be able to retire by 65, and 53% will need to keep working even when they do retire. Boomers and Beyond: 5 Ways To Make Extra Money if You Retire in Your 70s – https://www.gobankingrates.com/retirement/planning/boomers-ways-make-extra-money-retire-70s/.

I admit to falling for the clickbait. Of course I wanted to know about 5 ways to make extra money if I retire in my 70’s. And I’m a Boomer. So I read the article. Here are the 5 ways to make extra money:

Add Money to a High-Yield Savings Account

Buy Dividend Stocks

Rent Out Unused Space in Your Home

Become a Dog Walker

Become a Ride-Share Driver

What is the average monthly benefit for a retired worker? The estimated average monthly Social Security retirement benefit for January 2024 is $1,907. https://faq.ssa.gov/en-us/Topic/article/KA-01903

Hmm…

I wrote back in May that my focus was simple. All I had to do was stay healthy and stay connected with an employer willing to keep an Old Guy with a particular set of skills on the payroll. More Random Thoughts on Retirement – The Dot Project May 2024. At this point I hope to become a dog walker only if I want to, not if I have to. Prioritize your health. Save as much as you can. Plan on living AND working longer. Defer collecting Social Security retirement until you turn 70 (if you can). Read my other blog https://garyskitchen.net/. Tell your friends and family you found this blog written by an Old Guy on what it takes to become an Old Guy. They’ll love you for this.

The Boss once again is outside in the yard doing her thing. I’m inside doing my thing, drinking coffee, reading, writing. One of my addictions is staying current with the news and this post popped up in my RSS feed. At my age it doesn’t take much prompting for me to reflect on retirement. The Road to 70 is nearly complete. Soon I’ll be writing the next chapter of life The Road to 75. Dear Reader, if this sounds “old”, it is.

Critical thinking and understanding risk are the cornerstones of what I do. So when I have an opportunity to validate or repudiate the key assumptions in my plans I am in my Happy Place. When I decided not to retire several years ago my personal mantra focused on the following two critical variables in my retirement planning:

Stay healthy.

Find a willing employer.

Number One. I just had my annual wellness checkup. Bloodwork normal. Tendency towards obesity curtailed. Blood pressure elevated on two readings. Per Doctor’s orders I bought a BP machine and started keeping a log. All of my readings at home have been normal. A little white coat effect and the excitement of seeing my physician (Redhead Effect)…all good.

Number Two. Don’t underestimate how essential having or finding an employer who will pay you to work as you get older. Too many of us know the feeling of being cast out to the street for becoming too “old”.

As I prepare to write the next chapter it’s time to revisit and revise the two most important goals that got me to where I am. After some considerable time and effort here are my revised goals for the next five years.

Again, you can’t connect the dots looking forward; you can only connect them looking backward. So you have to trust that the dots will somehow connect in your future. You have to trust in something — your gut, destiny, life, karma, whatever. This approach has never let me down, and it has made all the difference in my life.

Steve Jobs

Let’s be honest: If you keeled over at 68, it would be a family tragedy—but it wouldn’t be a financial one. At that juncture, all your financial problems would be over, and your family would likely be better off financially because they’d inherit your retirement nest egg, which would probably still be largely intact. Instead, the real financial risk is living to a ripe old age. That raises the question: As you make your retirement plans, shouldn’t you care more about the live version of your future self, rather than the dead one?

Today’s life expectancies hover just below eighty, and if you reach the milestone of seventy they jump to the mid eighties. Due to advances in medicine and healthier lifestyles, reaching your nineties or even 100 is more realistic than ever. How do you ensure that you don’t run out of money? The answer is to start saving more now and plan to work longer. You’re Going to Live Past 90. Congrats! Here’s How to Pay For It. — https://www.esquire.com/news-politics/a60647995/how-to-afford-living-to-100/

A Big Dot

A little over four and a half years ago at the tender age of 65 my boss asked me if I was planning on retiring or if I wanted to continue working. I said I wanted to continue working. My FRA (full retirement age) for social security retirement benefits was still nearly a year away and I really didn’t want to collect a reduced benefit. As I connect the dots this decision turned out to be a Big Dot. Covid happened. Then inflation soared and continues to soar making everything cost more. I’m glad I didn’t retire back then and lock in a lower monthly lifetime benefit before the cost of everything went up.

Sometimes things in life work out as planned. Sometimes they don’t. When I decided to stay in the workforce the strategy was to wait until age 70 to collect social security benefits. The math was compelling.

My focus was simple. All I had to do was stay healthy and stay connected with an employer willing to keep an Old Guy with a particular set of skills on the payroll.

My particular set of skills is understanding what kills people.

The Road to 70 is now just a short trip. Just 10% of people in one survey planned to wait until age 70 to claim Social Security – https://www.cnbc.com/2023/08/08/survey-just-10percent-plan-to-wait-until-age-70-to-claim-social-security.html. Time for another Big Dot related to this Big Dot. I think I’ll keep working for another 3-5 years, contingent upon the same variables of sustained good health and a willing employer. I have about another 30 years to go, so why not do a few more years of work?

The workplace is evolving, too, with businesses increasingly seeking the experience and wisdom of senior talent. Currently, 19% of adults 65 and older are employed, compared to 11% in 1987, according to Pew Research. Moreover, individuals aged 65 and older constitute the most rapidly expanding group within the labor force. By 2032, it’s expected that one in every four U.S. workers will be 55 or older, with nearly one in 10 being 65 or older, showcasing the growing presence of seniors in the workplace.

Group-based trajectory modeling identified four groups of distinct occupational cognitive demands according to the degree of routine tasks in the participants occupations during their 30s, 40s, 50s and 60s. The researchers analyzed the link between these trajectory groups and clinically diagnosed MCI and dementia in participants in the HUNT4 70+ Study (2017-19). Additionally, the researchers accounted for important dementia risk factors such as age, gender, educational level, income, overall health, and lifestyle habits from assessments made in 1984-86 and 1995-97. Within age groupings the researchers looked at such occupations as primary school teacher, salesperson, nurse and caregiver, office cleaner, civil engineer, and mechanic, among others.

When a psychology professor in Michigan looked through his data on interpersonal conflict a decade ago, he discovered something unexpected. The study, which examined differences across cultures and age groups, seemed to show Americans got wiser as they got older. Richard Nisbett was used to research showing poorer mental skills among elderly adults, but his work found they were better at recognizing multiple perspectives, encouraging compromise, and acknowledging the limits of their own knowledge.

Perhaps, he reasoned, navigating conflict got better with age because it was such a specific, experience-based skill. Working memory, which stores short-term facts like newly learned names, may decline but, as people get older, they inevitably accrue more knowledge from having navigated similar situations throughout their lives. Now 82 years old, Nisbett recognizes the improvement in himself. “I’ve noticed situations to avoid, comments not to make, and the importance of apology,” he said.

The precursors for vitamin D are reduced as we age. By age 70, our ability to produce vitamin D is about half of what it was at age 20. D is in scarce supply in our regular diets. Most milk and some juices, milk alternatives and cereals are fortified with D, but other dietary sources — fatty fish like mackerel and sardines, and some mushrooms — aren’t exactly a staple in most American diets. As a result, nearly 1 in 4 people in the U.S. have inadequate blood levels of vitamin D3, the most active form.

You must be logged in to post a comment.