Retirement doesn’t just raise financial concerns – it can also mean feeling unmoored and irrelevant

Published: August 29, 2024 8:49am EDT

Author

Marianne Janack John Stewart Kennedy Professor of Philosophy, Hamilton College

Disclosure statement

Marianne Janack does not work for, consult, own shares in or receive funding from any company or organization that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

But this might not be the biggest problem that potential retirees face. The deeper issues of meaning, relevance and identity that retirement can bring to the fore are more significant to some workers.

Work has become central to the modern American identity, as journalist Derek Thompson bemoans in The Atlantic. And some theorists have argued that work shapes what we are. For most people, as business ethicist Al Gini argues, one’s work – which is usually also one’s job – means more than a paycheck. Work can structure our friendships, our understandings of ourselves and others, our ideas about free time, our forms of entertainment – indeed our lives.

I teach a philosophy course about the self, and I find that most of my students think of the problems of identity without thinking about how a job will make them into a particular kind of person. They think mostly about the prestige and pay that come with certain jobs, or about where jobs are located. But when we get to existentialist philosophers such as Jean-Paul Sartre and Simone de Beauvoir, I often urge them to think about what it means to say, as the existentialists do, that “you are what you do.”

Don’t let yourself be misled. Understand issues with help from experts

How you spend 40 years of your life, I tell them, for at least 40 hours each week – the time many people spend at their jobs – is not just a financial decision. And I have come to see that retirement isn’t just a financial decision, either, as I consider that next phase of my life.

Usefulness, tools and freedom

For Greek and Roman philosophers, leisure was more noble than work. The life of the craftsperson, artisan – or even that of the university professor or the lawyer – was to be avoided if wealth made that possible.

The good life was a life not driven by the necessity of producing goods or making money. Work, Aristotle thought, was an obstacle to the achievement of the particular forms of excellence characteristic of human life, like thought, contemplation and study – activities that express the particular character of human beings and are done for their own sake.

And so, one might surmise, retirement would be something that would allow people the kind of leisure that is essential to human excellence. But contemporary retirement does not seem to encourage leisure devoted to developing human excellence, partly because it follows a long period of making oneself into an object – something that is not free.

German philosopher Immanuel Kant distinguished between the value of objects and of subjects by the idea of “use.” Objects are not free: They are meant to be used, like tools – their value is tied to their usefulness. But rational beings like humans, who are subjects, are more than their use value – they are valuable in their own right, unlike tools.

And yet, much of contemporary work culture encourages workers to think of themselves and their value in terms of their use value, a change that would have made both Kant and the ancient Greek and Roman philosophers wonder why people didn’t retire as soon as they could.

But as one of my colleagues said when I asked him about retirement: “If I’m not a college professor, then what am I?” Another friend, who retired at 59, told me that she does not like to describe herself as retired, even though she is. “Retired implies useless,” she said.

So retiring is not just giving up a way of making money; it is a deeply existential issue, one that challenges one’s idea of oneself, one’s place in the world, and one’s usefulness.

One might want to say, with Kant and the ancients, that those of us who have tangled up our identities with our jobs have made ourselves into tools, and we should throw off our shackles by retiring as soon as possible. And perhaps from the outside perspective, that’s true.

But from the participant perspective, it’s harder to resist the ways in which what we have done has made us what we are. Rather than worry about our finances, we should worry, as we think about retirement, more about what the good life for creatures like us – those who are now free from our jobs – should be.

At the age of fifty I began the process of becoming what I wanted to be. I had known for a long time that I was a teacher and that the vehicle for my teaching would be in my writing. I also came to the conclusion I would never be compensated well enough through writing to support myself and my family. So I got good at something else.

That something else has and continues to provide a good living.

What I do is who I am and who I am is what I do. No existential crisis here.

If you’ve been to my blog before I apologize for repeating myself. But for new readers I’m past the “traditional” retirement age of 65. I don’t want to retire nor do I intend to retire for several years. One word describes why I continue to work. FEAR. I’m afraid of living too long and outliving my savings. I am petrified of leaving the workforce and no longer having an earned income stream. Living on a fixed income when the cost of everything keeps going higher scares the shit out of me.

Amidst my fear and anxiety the Social Security Administration approved my application for retirement benefits. When I looked at my monthly benefit I was pleasantly surprised. I then added up our future income sources and calculated that our fixed income from social security plus a small defined benefit pension plan will cover 82.5% of our current monthly expenses. Add in future annual withdrawals from savings and investments The Boss and I are financially OK until our nineties.

My fears are overblown. Check this out:

Conventional financial planning also overstates the income seniors need. That owes partly to planners assuming that seniors require the same amount of money throughout retirement. Yet as economists Michael Hurd and Susanne Rohwedder of the Rand Corp. have shown, average household spending drops by roughly 40% from age 65 to 90. Seniors aren’t running out of money—spending on gifts and donations increases with age. Retirees simply spend less on themselves than financial planners assume.

Planners likewise forget that much of adults’ pre-retirement income is spent on their children. The U.S. estimates that a couple earning roughly $83,000 with two children spends more than $26,000 annually providing food, housing, healthcare and other needs for their children. That’s money parents can’t spend on themselves. Of the income they could devote to their own needs, Social Security will replace around 60%. The upshot is that parents need less savings on top of Social Security than one might think. You Don’t Need to Be a Millionaire to Retire By Andrew G. Biggshttps://www.aei.org/op-eds/you-dont-need-to-be-a-millionaire-to-retire/

“I faced a painful reality: I didn’t know anything about anything….”

Andy Clarke – financial writer and editor, a retired CFA dispensing advice to retirees on investing and savings.

A 2021 survey by Pew Research looked at the question another way: It asked people from around the world what made their lives meaningful. In countries such as Italy, Spain, and Sweden, work ranked highly as a source of meaning. In Italy, work was the No. 1 source of meaning, with 43% saying they drew meaning from work. Spaniards ranked work higher than family. But in the US, only 17% mentioned work as a source of meaning. That was a sharp decline from when Pew asked the same question four years prior — a full one-third of Americans mentioned their jobs as a source of meaning in 2017, double the 2021 rate. Increasingly, it seems that more people feel like their jobs don’t matter. Why so many Americans hate their jobs — https://www.businessinsider.com/american-employees-disengaged-work-meaningless-fake-email-jobs-2024-6

Here are some of the biggest reasons some people don’t have enough money saved for retirement:

You don’t make enough money. This is likely the biggest reason most households don’t have enough retirement savings. Some people simply don’t earn a high enough income to have any money left over.

There are personal finance people who would like you to believe it’s all bad habits that cause people to under-fund their retirement.

Many people don’t have any excess remaining after paying for necessities.

We saved as much as we could and if I work a few more years we can plump up our financial cushion. Our expenses will likely be less in the years to come (except someone’s clothing/shoe/Tiny Human budget and that someone is not me). So with a willing employer and continued good health I plan to work full time for a few more years and then ease into retirement by continuing to work part time.

The first five years of my 30 Year Plan is complete. Now I need to work on what to do for the 25 years afterwards.

Scientists from the University of South Australia measured blood samples from 172 middle aged adults, finding a strong link between low magnesium levels and high amounts of a genotoxic amino acid called homocysteine. University of South Australia. “Low magnesium levels increase disease risk.” ScienceDaily. http://www.sciencedaily.com/releases/2024/08/240812123307.htm (accessed August 13, 2024).

Journal Reference:

Varinderpal S. Dhillon, Permal Deo, Michael Fenech. Low magnesium in conjunction with high homocysteine increases DNA damage in healthy middle aged Australians. European Journal of Nutrition, 2024; DOI: 10.1007/s00394-024-03449-0

Whole grains, dark green leafy vegetables, nuts, beans, bananas, avocados and dark chocolate are magnesium-rich foods.

Effects of Genetic Risk on Incident Type 2 Diabetes and Glycemia: The T2D-GENE Lifestyle Intervention Trial – The Journal of Clinical Endocrinology & Metabolism, dgae422, https://doi.org/10.1210/clinem/dgae422

On a personal level I’ve been taking a low dose statin forever, 100 IU Vitamin D3 and a multivitamin daily, need to move more, Fexofenadine prn, and still not a vegan or drive an EV.

The study found that among older adults aged 75-84, initiation of statin therapy led to a 1.2% risk reduction in major CVD over a 5-year period. For older adults aged 85 and greater, initiation of statins had an even larger impact, leading to a 4.4% risk reduction in major CVD over a 5-year period. The study found that there was no significant difference in adverse effects including myopathy or liver dysfunction in both age groups.

For older adults aged 75 or greater, empiric vitamin D supplementation is recommended because of the possible reduction of risk in all-cause mortality in this population. Of note, this was a grade 2 recommendation by the panel, indicating that the benefits of the treatment probably outweigh the risks. The panel stated that vitamin D supplementation could be delivered through fortified foods, multivitamins with vitamin D, or as a separate vitamin D supplement.

The study found that participants who were more sedentary were less likely to age healthfully, with each additional 2 hours of TV watching per day associated with a 12% reduction in likelihood of healthy aging. Light physical activity was associated with a significant increase in healthy aging, with a 6% increase in the likelihood of healthy aging for each additional 2 hours of light activity. Each additional 1 hour of moderate to vigorous activity was associated with a 14% increase in the likelihood of healthy aging. These findings support discussions with patients that behavior change, even in small increments, can be beneficial in healthy aging.

The researchers found that people in the high resiliency group were less anxious and depressed, less prone to judge, and had activity in regions of the brain associated with emotional regulation and better cognition compared to the group with low resiliency. “When a stressor happens, often we go to this aroused fight or flight response, and this impairs the breaks in your brain,” Gupta said. “But the highly resilient individuals in the study were found to be better at regulating their emotions, less likely to catastrophize, and keep a level head,” added Desiree Delgadillo, postdoctoral researcher and one of the first authors.

The high resiliency group also had different microbiome activity than the low resiliency group. Namely, the high resiliency group’s microbiomes excreted metabolites and exhibited gene activity associated with low inflammation and a strong and healthy gut barrier. A weak gut barrier, otherwise known as a leaky gut, is caused by inflammation and impairs the gut barrier’s ability to absorb essential nutrients needed by the body while blocking toxins from entering the gut.

Resilience is the capacity to remain flexible and adaptable while facing life’s challenges. It is a complex concept involving traits, environmental factors, and a learned capacity that comes from experience. https://positivepsychology.com/what-is-resilience/

Ben Carlson is a smart man. His short list of unexciting, non-sexy and generally boring bits of investment advice inspired me to add my own generally boring bits of non solicited quasi-investment advice. And in no particular order of importance here they are.

Live beneath your means.

Pay yourself first (save, save, save some more).

Invest in your health (diet, exercise, etc).

Invest in your brain, be a lifelong learner.

Connect with family and friends (social media doesn’t count).

Find your purpose.

Work hard. Hard work is no guarantee of success but the lack of hard work guarantees failure.

A happy fulfilling life is more than just the money or your net worth.

Again, you can’t connect the dots looking forward; you can only connect them looking backward. So you have to trust that the dots will somehow connect in your future. You have to trust in something — your gut, destiny, life, karma, whatever. This approach has never let me down, and it has made all the difference in my life.

Sometimes things in life work out as planned. Sometimes they don’t. This time the plan is going as planned. At my annual wellness check up everything turned out fine except for my blood pressure. The two readings taken showed an elevated systolic and per Doctor’s orders I had to buy a BP machine which set me back $36 plus tax. I was instructed to keep a log for two weeks. For grins, I checked my online account to see what Dr. Lewis wrote for the office visit notes. No mention whatsoever regarding my BP readings. Probably because both of us felt this wasn’t a huge problem. The Boss started showing some concern and I had to report my pressures to her every day. Again I felt this wasn’t a worrisome medical issue. Besides if the diagnosis was hypertension I was looking at daily Lisinopril 10 mg, no big deal.

After two weeks I sent Dr. Lewis my log. She replied later that day.

Thank you for diligently keeping track of your blood pressure readings. I see that your readings have been fairly consistent. Yes you can stop watching it. If you feel fatigued or headaches please recheck it.

Sincerely, KL

I survived another annual wellness check. The Road to 70 is still pretty smooth. But the ride is not as smooth for others.

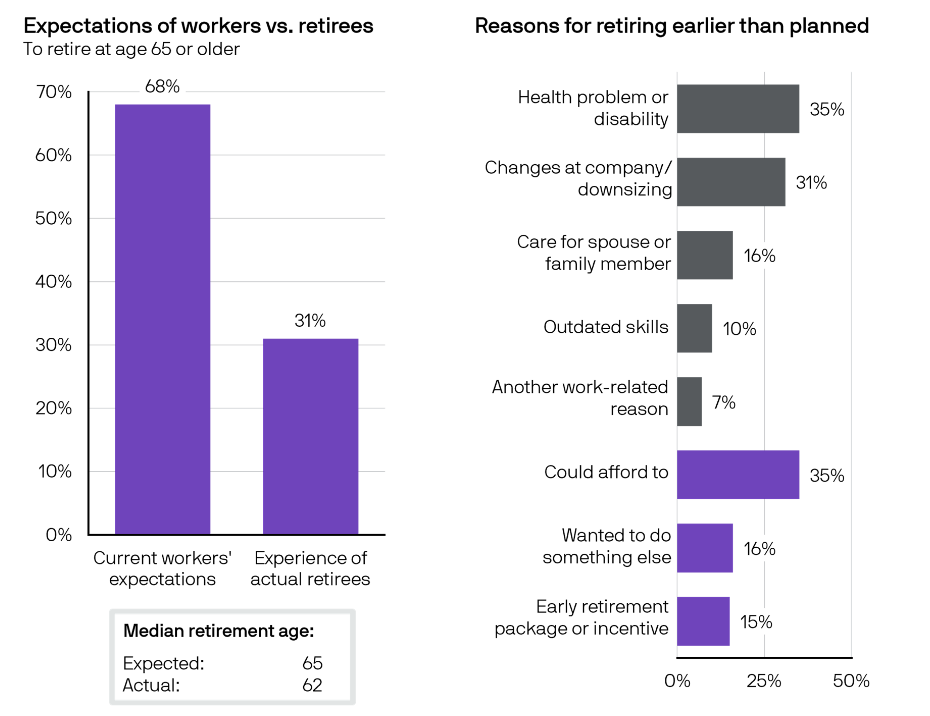

A CivicScience survey of nearly 3,000 respondents conducted between March and May 2024 reported 61% of those aged 55 and over say they won’t be able to retire by 65, and 53% will need to keep working even when they do retire. Boomers and Beyond: 5 Ways To Make Extra Money if You Retire in Your 70s – https://www.gobankingrates.com/retirement/planning/boomers-ways-make-extra-money-retire-70s/.

I admit to falling for the clickbait. Of course I wanted to know about 5 ways to make extra money if I retire in my 70’s. And I’m a Boomer. So I read the article. Here are the 5 ways to make extra money:

Add Money to a High-Yield Savings Account

Buy Dividend Stocks

Rent Out Unused Space in Your Home

Become a Dog Walker

Become a Ride-Share Driver

What is the average monthly benefit for a retired worker? The estimated average monthly Social Security retirement benefit for January 2024 is $1,907. https://faq.ssa.gov/en-us/Topic/article/KA-01903

Hmm…

I wrote back in May that my focus was simple. All I had to do was stay healthy and stay connected with an employer willing to keep an Old Guy with a particular set of skills on the payroll. More Random Thoughts on Retirement – The Dot Project May 2024. At this point I hope to become a dog walker only if I want to, not if I have to. Prioritize your health. Save as much as you can. Plan on living AND working longer. Defer collecting Social Security retirement until you turn 70 (if you can). Read my other blog https://garyskitchen.net/. Tell your friends and family you found this blog written by an Old Guy on what it takes to become an Old Guy. They’ll love you for this.

The Boss once again is outside in the yard doing her thing. I’m inside doing my thing, drinking coffee, reading, writing. One of my addictions is staying current with the news and this post popped up in my RSS feed. At my age it doesn’t take much prompting for me to reflect on retirement. The Road to 70 is nearly complete. Soon I’ll be writing the next chapter of life The Road to 75. Dear Reader, if this sounds “old”, it is.

Critical thinking and understanding risk are the cornerstones of what I do. So when I have an opportunity to validate or repudiate the key assumptions in my plans I am in my Happy Place. When I decided not to retire several years ago my personal mantra focused on the following two critical variables in my retirement planning:

Stay healthy.

Find a willing employer.

Number One. I just had my annual wellness checkup. Bloodwork normal. Tendency towards obesity curtailed. Blood pressure elevated on two readings. Per Doctor’s orders I bought a BP machine and started keeping a log. All of my readings at home have been normal. A little white coat effect and the excitement of seeing my physician (Redhead Effect)…all good.

Number Two. Don’t underestimate how essential having or finding an employer who will pay you to work as you get older. Too many of us know the feeling of being cast out to the street for becoming too “old”.

As I prepare to write the next chapter it’s time to revisit and revise the two most important goals that got me to where I am. After some considerable time and effort here are my revised goals for the next five years.

You must be logged in to post a comment.