We plan for the money. We don’t plan for the Monday morning when no one needs you to be anywhere.

Julianne Holt-Lunstad, a professor of psychology and neuroscience at Brigham Young University, published a landmark meta-analysis in 2015 involving over 3.4 million participants. Her finding: social isolation increases the risk of premature death by 26%, and loneliness by 29%. Those numbers rival the health impact of smoking fifteen cigarettes a day. We treat smoking as a public health crisis. We treat retirement loneliness as a personal failing.

Though the traditional retirement age in the U.S. typically falls between 62 and 67, many Americans continue working beyond that point. As of 2024, slightly more than 22% of adults aged 65 and older are still employed, either full-time or part-time. Though the traditional retirement age in the U.S. typically falls between 62 and 67, many Americans continue working beyond that point. As of 2024, slightly more than 22% of adults aged 65 and older are still employed, either full-time or part-time. – https://financebuzz.com/working-in-retirement-data

So I’m not the only Old Guy who is still working past age 65.

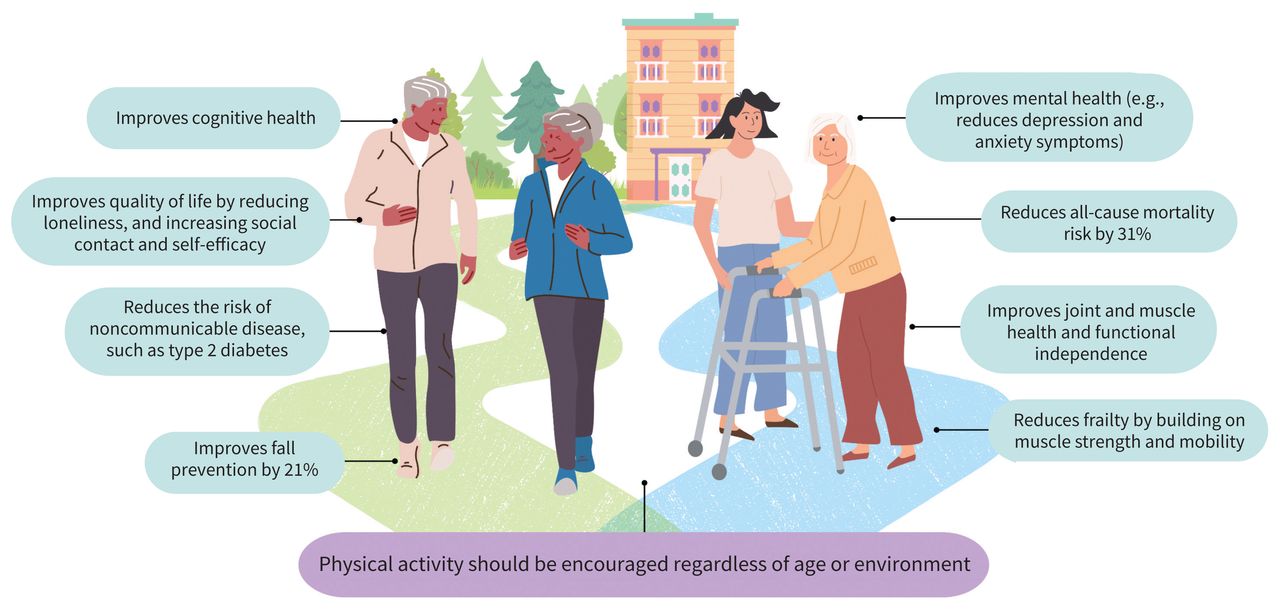

The association between physical activity and mortality and morbidity is well established. A 2023 meta-analysis of large prospective studies that examined dose–response found that physical activity levels equivalent to the recommended 150 minutes per week of moderate physical activity reduced all-cause mortality by 31% compared with no physical activity.12 The authors used metabolic equivalent of task (MET), the ratio of work metabolic rate to resting metabolic rate. One MET is equivalent to the energy cost of sitting quietly. A 2019 systematic review and meta-analysis found that, among middle-aged and older adults (aged ≥ 40 yr), higher levels of total physical activity were associated with reduced risk of death in a dose–response relation, such that the most, second-most, and third-most active quartiles were associated with 0.47, 0.35, and 0.28 hazard ratios, respectively, compared with the least active quartile.13 According to a large 2019 observational study, resistance exercise is also associated with reduced mortality independent of aerobic exercise.14 Two 2022 meta-analyses found, respectively, that 60 minutes of resistance exercise per week is associated with a risk reduction of 27% in all-cause mortality15 and that muscle-strengthening activities for 30–60 minutes per week is associated with a 10%–20% reduction.16

Cardiorespiratory fitness and peak exercise capacity are associated with mortality. Peak exercise capacity is a better indicator of risk of death than established cardiovascular risk factors such as smoking, hypertension, and diabetes mellitus.17 A study examining cardiorespiratory fitness in older adults found dose-dependent reductions in mortality across all age groups (including participants aged 60–69, 70–79, and 80–95 yr).18 Substantial improvements (approximately 16%) in VO2max (an individual’s maximum rate of oxygen consumption, a strong indicator of mortality19) in older adults can occur with only 90 minutes of submaximal exercise per week over 16–20 weeks.20

Strength is also associated with reductions in all-cause mortality in older adults. A 2022 systematic review and meta-analysis found a linear inverse relation between handgrip strength and all-cause mortality up to sex-dependent thresholds (42 kg for men, 25 kg for women) in older adults.21 In their 2018 systematic review and meta-analysis, the authors found both handgrip and knee extension strength to be predictors of all-cause mortality in adults, with most of the studies examining adults older than 65 years.22 – Move more, age well: prescribing physical activity for older adults CMAJ January 27, 2025 197 (3) E59-E67; DOI: https://doi.org/10.1503/cmaj.231336

A key takeaway from the updated guidelines is that the biggest benefits often come from a simple starting point. Transitioning from no resistance training to any regular activity can lead to meaningful improvements. While factors such as load, volume, and frequency can be adjusted, experts say the main priority for most adults should be building a routine they can follow consistently.

Another important shift in the recommendations is the recognition that effective resistance training does not require access to a gym. Exercises using elastic bands, bodyweight movements, or simple at home routines can still produce measurable gains in strength, muscle size, and daily function. McMaster University. “The best strength training plan might be simpler than you think.” ScienceDaily https://www.sciencedaily.com/releases/2026/03/260319074552.htm

The study focused exclusively on adults 80 and older, a group with very different dietary requirements than younger adults. As people age, the body goes through significant physiological changes. Energy expenditure decreases, and losses in muscle mass, bone density, and appetite are common. Together, these changes increase the risk of malnutrition and frailty.

Most evidence for the health benefits of diets that exclude meat comes from studies of younger adults rather than frail older populations. Some research suggests older non-meat eaters face a higher risk of fractures due to lower calcium and protein intake.

In later life, nutritional priorities shift. Rather than focusing on preventing long-term diseases, the goal becomes maintaining muscle mass, preventing weight loss and ensuring every mouthful delivers plenty of nutrients. Study finds vegetarians over 80 less likely to reach 100-The Conversation. https://www.sciencedaily.com/releases/2026/02/260225081214.htm “Study finds vegetarians over 80 less likely to reach 100.” ScienceDaily. (accessed February 27, 2026).

Story Source:

Materials provided by The Conversation. Original written by Chloe Casey, Lecturer in Nutrition and Behaviour, Bournemouth University. Note: Content may be edited for style and length.

CRSP’s origins date back to the 1960s. Its initial goal was to build a database of historical stock prices. This is harder than it might seem. Before trading was computerized, stock prices were maintained on paper. And when stocks split or companies merged, that added to the complexity.

Despite this seemingly dull mandate, CRSP has played an important role in the development of modern finance over the years. Most notably, the efficient market hypothesis and the capital asset pricing model were both made possible by CRSP data. And today, many of the world’s largest index funds, including Vanguard’s Total Stock Market Fund, are built on CRSP indexes. Endowment Lessonshttps://humbledollar.com/2026/02/endowment-lessons/

This article by Adam M. Grossman uses the University of Chicago’s financial struggles as a cautionary tale for individual investors.

Key Lessons for Individual Investors

Spending: Avoid “Keeping Up with the Joneses”

The university invested heavily in new buildings and programs to maintain its “eminence” without securing corresponding revenue.

Takeaway: Financial success depends on income exceeding expenses. Operating costs of new assets (like large homes or complex projects) must be planned for in advance.

Saving: Beware of Recency Bias

During a 15-year market boom, the university ramped up debt rather than stockpiling resources.

Takeaway: Investors often falsely assume current trends will continue forever. Use periods of market strength to re-balance portfolios and manage risk rather than increasing lifestyle or debt commitments.

Investing: Complexity vs. Simplicity

Performance: UChicago’s endowment returned 6.7% annually over 10 years, trailing a simple Vanguard Balanced Index Fund (VBIAX), which returned 8.2%.

Liquidity:The university locked over 60% of its funds into illiquid assets like private equity and real estate, making it difficult to cover cash flow needs.

Takeaway: High-fee, complex, and illiquid investments often under-perform simple index funds. If elite institutions with dedicated investment offices “are having second thoughts” about private equity, the message for individual investors seems clear.

This summary was produced by Gemini AI and edited by yours truly.

In findings published in Cell Metabolism, the team demonstrated that red blood cells can alter their metabolism when oxygen levels drop. This shift allows the cells to deliver oxygen to tissues more efficiently at high altitude. At the same time, it lowers circulating blood sugar, offering a potential explanation for reduced diabetes risk. Gladstone Institutes. “Scientists discover why high altitude protects against diabetes.” ScienceDaily https://www.sciencedaily.com/releases/2026/02/260221060952.htm (accessed February 21, 2026).

Journal Reference:

Yolanda Martí-Mateos, Zohreh Safari, Shaun Bevers, Ayush D. Midha, Will R. Flanigan, Tej Joshi, Helen Huynh, Brandon R. Desousa, Skyler Y. Blume, Alan H. Baik, Stephen Rogers, Aaron V. Issaian, Allan Doctor, Angelo D’Alessandro, Isha H. Jain. Red blood cells serve as a primary glucose sink to improve glucose tolerance at altitude. Cell Metabolism, 2026; DOI: 10.1016/j.cmet.2026.01.019

The first takeaway is about the mindset. Winning requires staying in the present. When you lose nearly half the points you play, the past offers no help. Dwelling on past mistakes only distracts from the real goal, which is to win the match. We cannot change what has happened, and we cannot control what comes next. Stay present, follow the process, and let the result take care of itself…The idea of edge applies directly to our lives. Life is made up of thousands of decisions taken over decades. A small edge in how we make those decisions quietly stacks the odds in our favor.

Take health. Lifting weights a few times a week, walking a few miles a day, eating reasonably well, and sleeping enough each give us a small edge. We are not competing with anyone else here. We are competing against chronic diseases. These habits do not guarantee outcomes, but they help us avoid most of the problems that are within our control, and leave the rest to chance. None of these decisions matter much on their own. Taken together over years they matter a lot.

Nice article, wonderful insights. Now go read the entire article.

Physical activity consistently emerges as the most important factor influencing both absolute physical capacity and the rate of age-related decline. Our longitudinal data are consistent with previous studies showing that regular physical activity can attenuate the decline in physical performance [17, 32–37]. Individuals who were physically active in their leisure time at age 16 maintained higher aerobic capacity, muscular endurance and muscle power throughout the observation period. This emphasizes the importance of early intervention to establish positive exercise habits in adolescence and early adulthood, as these patterns appear to have long-term benefits for physical function. Encouragingly, our results show that transitioning from physical inactivity to activity at any age significantly improves performance in all fitness modalities studied. These findings contradict the assumption that early inactivity irreversibly impairs physical performance. Rather, taking up regular physical activity leads to measurable improvements in performance even in later decades of life. This finding is of particular importance for clinical practice, as physical activity is still the only evidence-based intervention to reduce the risk of sarcopenia [2, 38]. Recent large population studies also show that an active lifestyle is beneficial at any age [13, 39, 40]. Rise and Fall of Physical Capacity in a General Population: A 47-Year Longitudinal Study – https://onlinelibrary.wiley.com/doi/10.1002/jcsm.70134

Text above in bold are my highlights.

Despite the documented limitations this is a very strong study.

I’ve been doing my home based virtual physical therapy for nearly a year. I’m trying to get to the gym at least twice a week. I don’t walk as much as I used to but…

“We have to understand that anything in the past takes you out of the present moment. Anything in the future takes you out of the present moment.”

Zen Master Daigneault

To readers who are visiting this blog for the first time my posts on Random Thoughts About Retirement and Unretirement are written by an Old Guy who is old enough to be retired but isn’t retired and is still working. I had another birthday and the older I get the more I think about retirement. Back in 2023 I was thinking about what retirement for me would look like (see More Random Thoughts on Retirement – June 2023). But decisions such as this take serious thought and consideration. At first I thought I wanted to retire to a quiet life of blogging and writing my Future Best Seller titled The Man Who Had No Hobbies. After much thought I decided to add a short term goal to my retirement plan. My new short term goal is to avoid unretirement.

My RSS feed feeds me headlines on unretirement.

According to a new report from T. Rowe Price around 7% of retirees are looking for work in retirement, while 20% say they’re already working part time or full time…The two main reasons for coming back into the workforce are a tale of opposites. While 45% chose to work for social and emotional benefits… a slightly larger percentage — 48% — felt they needed to work for financial reasons.

Once an eagerly awaited milestone, retirement is currently undergoing a transformative reevaluation. Traditionally seen as a well-deserved period of rest and relaxation, the dream of early retirement is now being challenged by a new perspective – that of embracing lifelong work. This paradigm shift reflects the changing nature of work, increased life expectancy, and the desire for personal fulfillment.

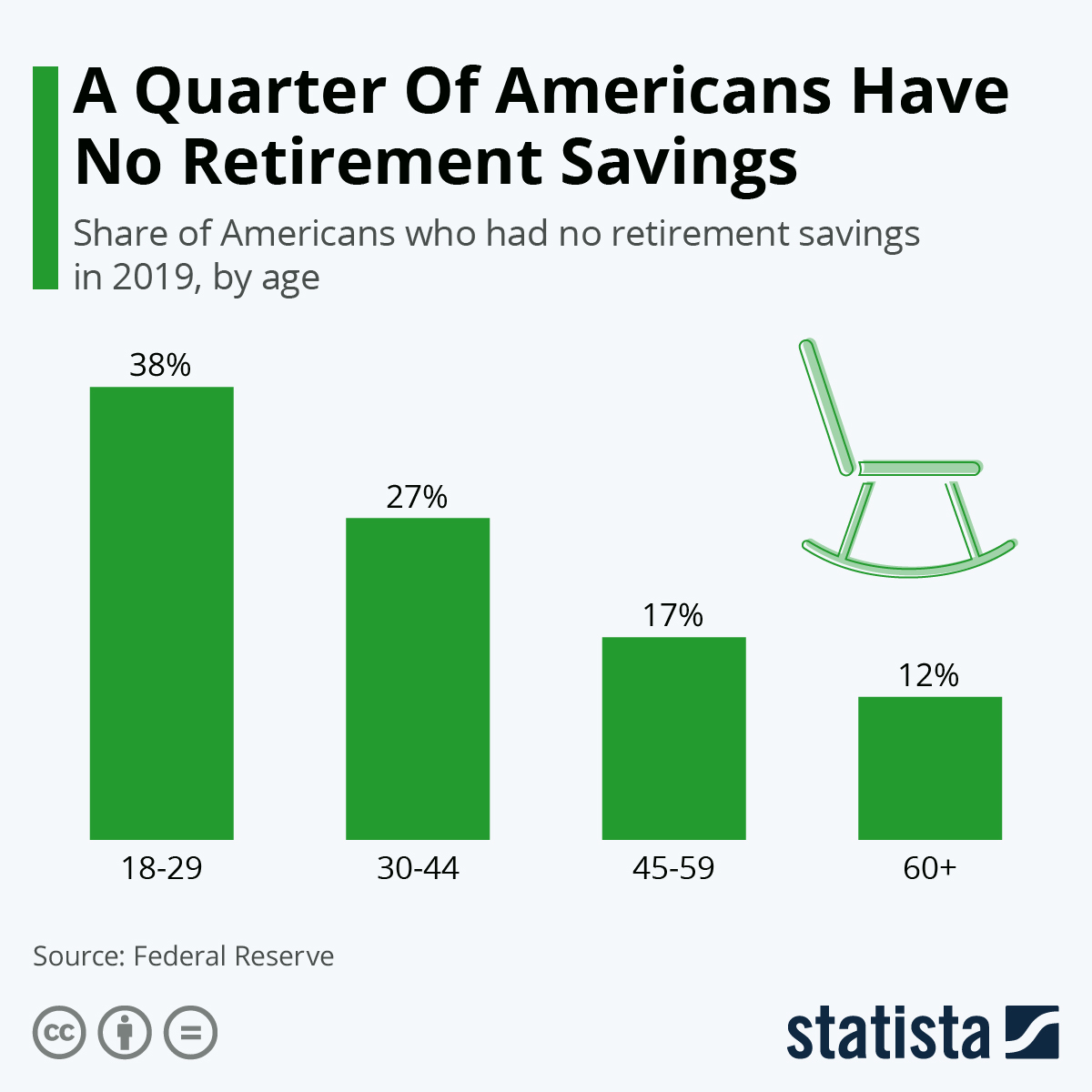

The reality is many won’t have a choice. The following chart illustrates retirement savings as of 2019.

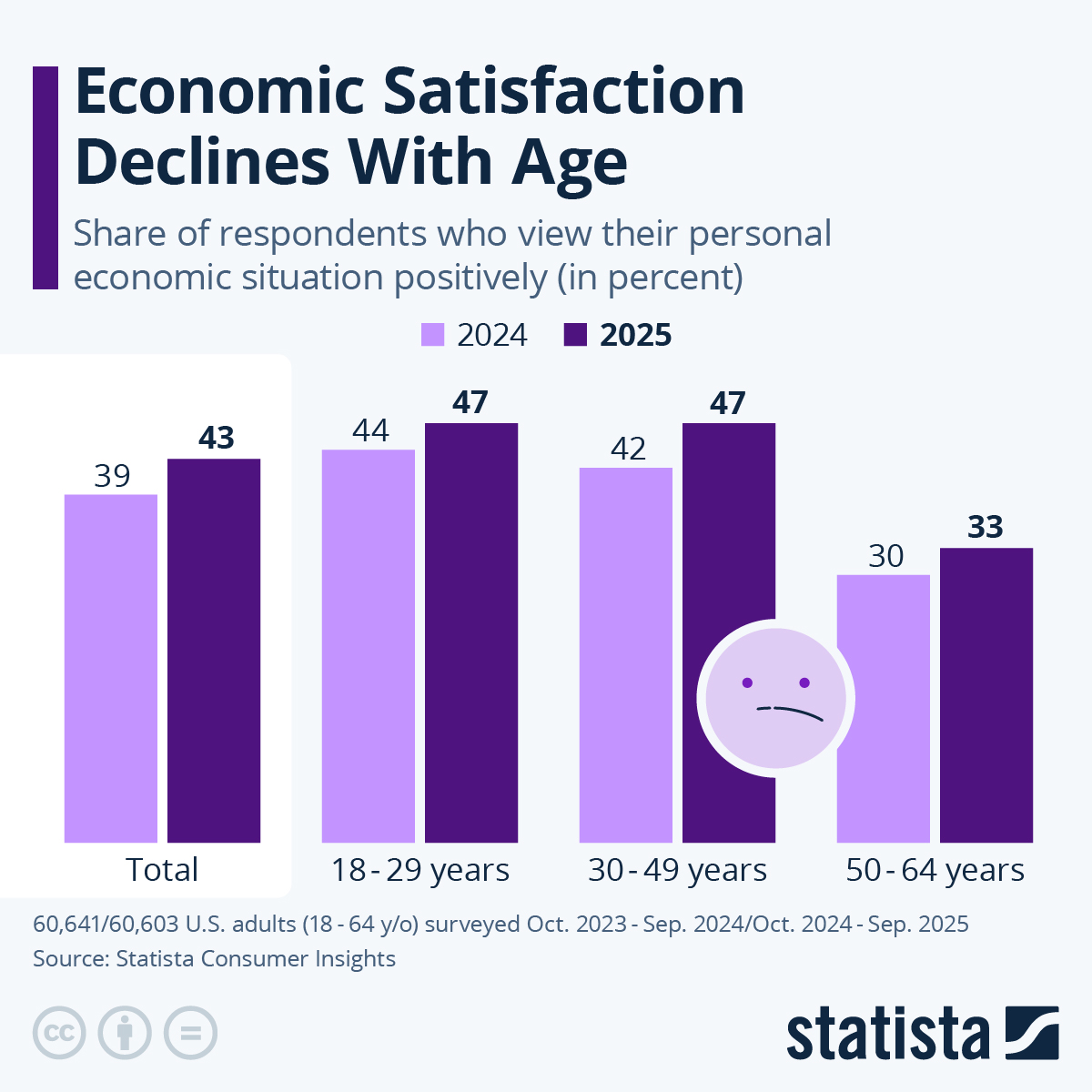

Americans are having trouble financially preparing themselves for life after work. A recent Federal Reserve report found that nearly a quarter of U.S. adults have absolutely no retirement savings or pension. Even though the level of preparation increases as people get older, concern about inadequate savings is still readily apparent across all age groups, even older people in their 60s.

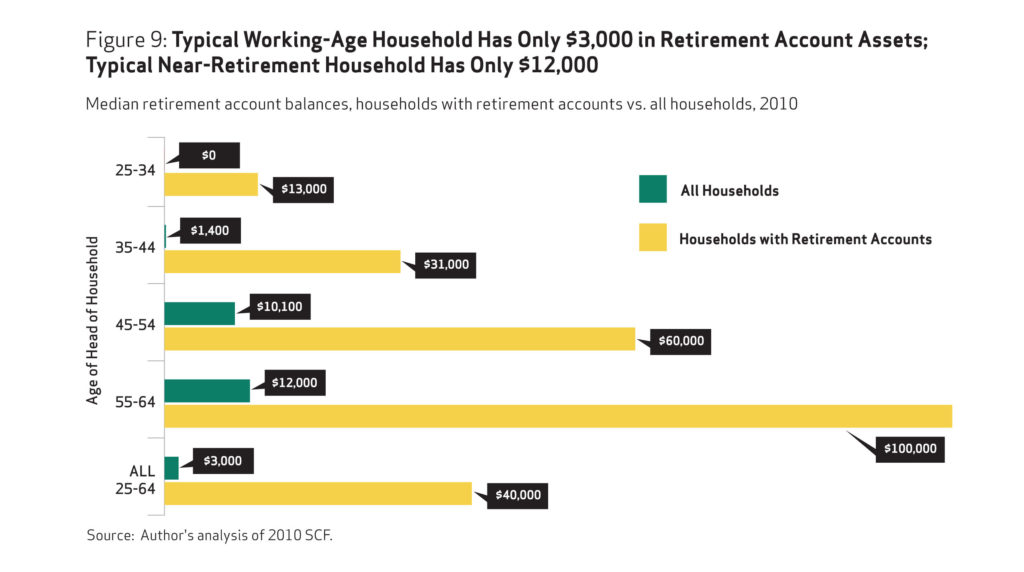

OOPS. I’m glad I didn’t click the Publish button. The savings situation appears to be worse than I thought. The study below was an analysis of data from 2010!

The study broadly examines how American households are faring in relation to retirement savings targets recommended by some financial services firms. It uses the Federal Reserve’s Survey of Consumer Finances to analyze retirement plan participation, savings, and overall assets of all U.S. households age 25 to 64, not just those with retirement account assets. This is important because some 45 percent, or 38 million working-age households, do not have any retirement account assets.

The average working household has virtually no retirement savings. When all households are included— not just households with retirement accounts—the median retirement account balance is $3,000 for all working-age households and $12,000 for near-retirement households. Two-thirds of working households age 55-64 with at least one earner have retirement savings less than one times their annual income, which is far below what they will need to maintain their standard of living in retirement.

The findings confirm that the American Dream of retiring comfortably after a lifetime of work will be impossible for many. Based on 401(k)–type account and IRA balances alone, some 92 percent of working households do not meet conservative retirement savings targets for their age and income. Even when counting their entire net worth, 65 percent still fall short.

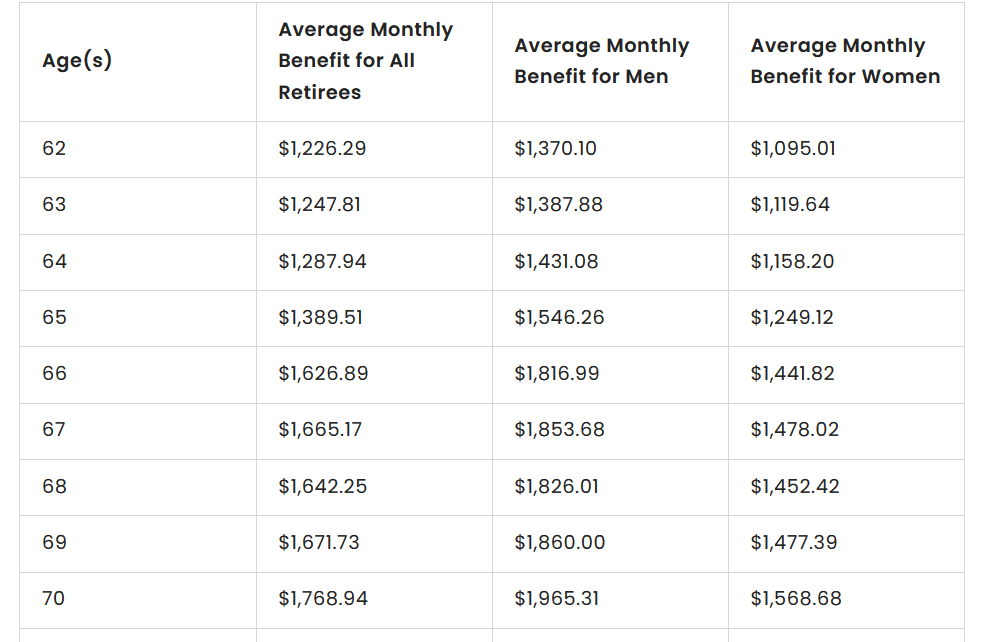

So how will you afford retirement without any savings? Don’t look to Social Security. Here’s some numbers on average Social Security payments. The full chart at the source website goes up to age 100.

As of December 31, 2021, the average Social Security payment for all retirees was $1,658.03 a month, according to the Social Security Administration’s Annual Statistical Supplement for 2022. For men, the overall average was $1,838.08. For women, the average was $1,483.75 — a difference of $354.33 per month.

Whether people unretire or simply stay in the workforce longer, some of the largest financial benefits of additional years of work are delaying retirement account withdrawals and delaying claiming Social Security benefits. These actions essentially shorten the amount of time your assets will need to support you in retirement. Even a few additional years of income have a positive effect on the probability that you won’t outlive your funds.

The Boss (SWMBO) and I talk about this often. Once the W2 income stops and we have to rely upon a small corporate pension, savings, and a shaky Social Security promise we’ll have to get conservative on our spending. No more Stratocasters. Less purchases for wardrobe enhancements. Gas station beer instead of craft brews.

You must be logged in to post a comment.