We plan for the money. We don’t plan for the Monday morning when no one needs you to be anywhere.

Julianne Holt-Lunstad, a professor of psychology and neuroscience at Brigham Young University, published a landmark meta-analysis in 2015 involving over 3.4 million participants. Her finding: social isolation increases the risk of premature death by 26%, and loneliness by 29%. Those numbers rival the health impact of smoking fifteen cigarettes a day. We treat smoking as a public health crisis. We treat retirement loneliness as a personal failing.

Though the traditional retirement age in the U.S. typically falls between 62 and 67, many Americans continue working beyond that point. As of 2024, slightly more than 22% of adults aged 65 and older are still employed, either full-time or part-time. Though the traditional retirement age in the U.S. typically falls between 62 and 67, many Americans continue working beyond that point. As of 2024, slightly more than 22% of adults aged 65 and older are still employed, either full-time or part-time. – https://financebuzz.com/working-in-retirement-data

So I’m not the only Old Guy who is still working past age 65.

“We have to understand that anything in the past takes you out of the present moment. Anything in the future takes you out of the present moment.”

Zen Master Daigneault

To readers who are visiting this blog for the first time my posts on Random Thoughts About Retirement and Unretirement are written by an Old Guy who is old enough to be retired but isn’t retired and is still working. I had another birthday and the older I get the more I think about retirement. Back in 2023 I was thinking about what retirement for me would look like (see More Random Thoughts on Retirement – June 2023). But decisions such as this take serious thought and consideration. At first I thought I wanted to retire to a quiet life of blogging and writing my Future Best Seller titled The Man Who Had No Hobbies. After much thought I decided to add a short term goal to my retirement plan. My new short term goal is to avoid unretirement.

My RSS feed feeds me headlines on unretirement.

According to a new report from T. Rowe Price around 7% of retirees are looking for work in retirement, while 20% say they’re already working part time or full time…The two main reasons for coming back into the workforce are a tale of opposites. While 45% chose to work for social and emotional benefits… a slightly larger percentage — 48% — felt they needed to work for financial reasons.

Once an eagerly awaited milestone, retirement is currently undergoing a transformative reevaluation. Traditionally seen as a well-deserved period of rest and relaxation, the dream of early retirement is now being challenged by a new perspective – that of embracing lifelong work. This paradigm shift reflects the changing nature of work, increased life expectancy, and the desire for personal fulfillment.

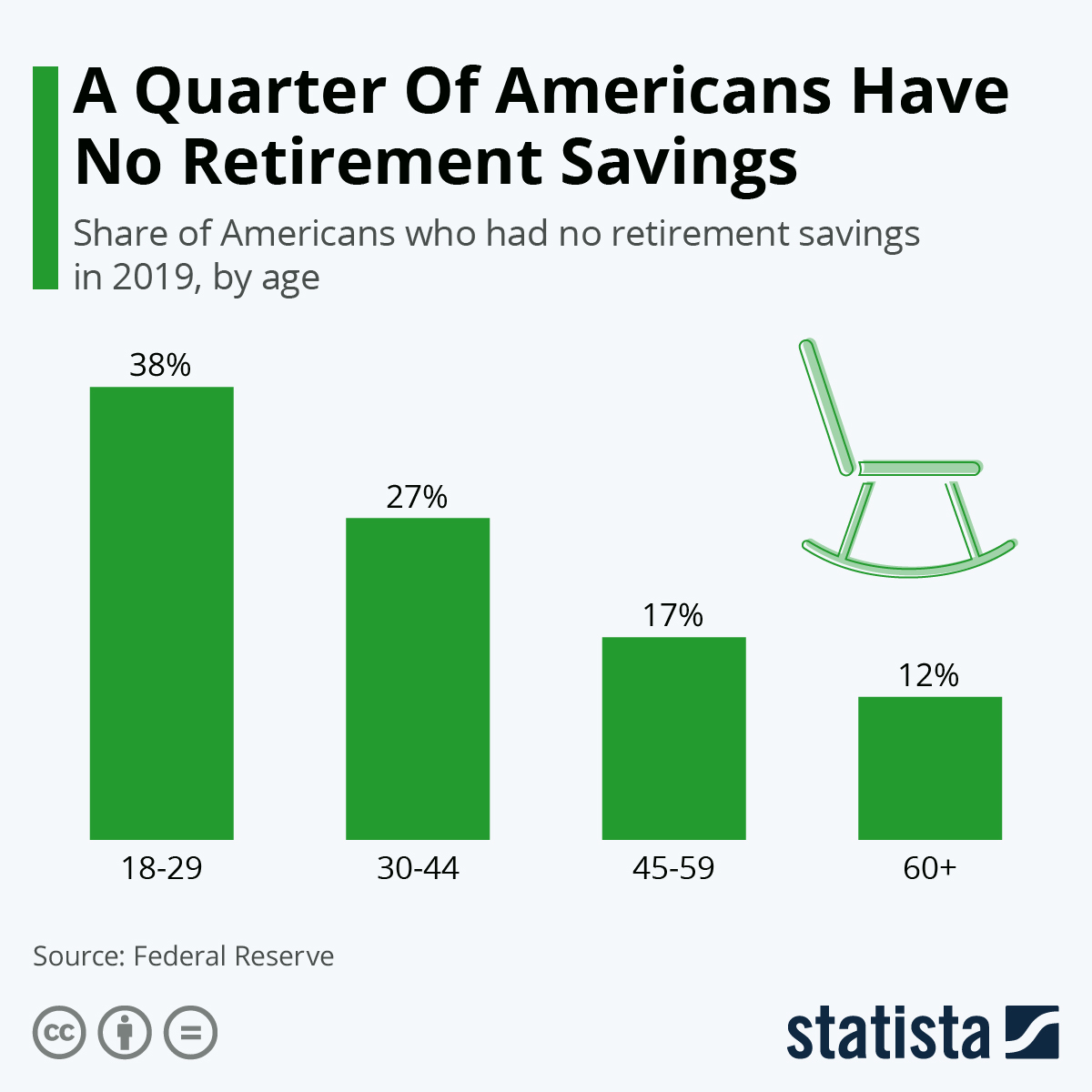

The reality is many won’t have a choice. The following chart illustrates retirement savings as of 2019.

Americans are having trouble financially preparing themselves for life after work. A recent Federal Reserve report found that nearly a quarter of U.S. adults have absolutely no retirement savings or pension. Even though the level of preparation increases as people get older, concern about inadequate savings is still readily apparent across all age groups, even older people in their 60s.

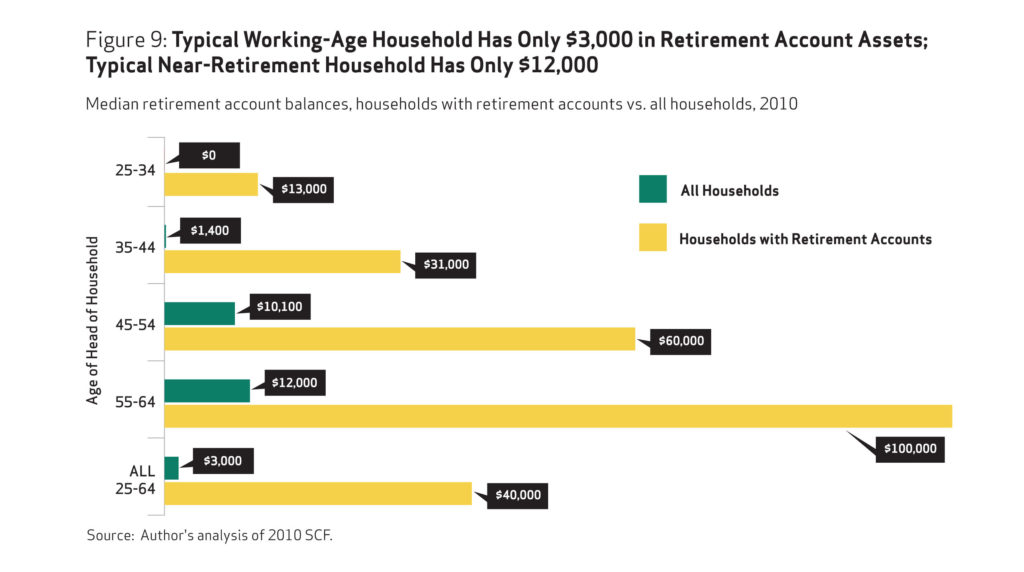

OOPS. I’m glad I didn’t click the Publish button. The savings situation appears to be worse than I thought. The study below was an analysis of data from 2010!

The study broadly examines how American households are faring in relation to retirement savings targets recommended by some financial services firms. It uses the Federal Reserve’s Survey of Consumer Finances to analyze retirement plan participation, savings, and overall assets of all U.S. households age 25 to 64, not just those with retirement account assets. This is important because some 45 percent, or 38 million working-age households, do not have any retirement account assets.

The average working household has virtually no retirement savings. When all households are included— not just households with retirement accounts—the median retirement account balance is $3,000 for all working-age households and $12,000 for near-retirement households. Two-thirds of working households age 55-64 with at least one earner have retirement savings less than one times their annual income, which is far below what they will need to maintain their standard of living in retirement.

The findings confirm that the American Dream of retiring comfortably after a lifetime of work will be impossible for many. Based on 401(k)–type account and IRA balances alone, some 92 percent of working households do not meet conservative retirement savings targets for their age and income. Even when counting their entire net worth, 65 percent still fall short.

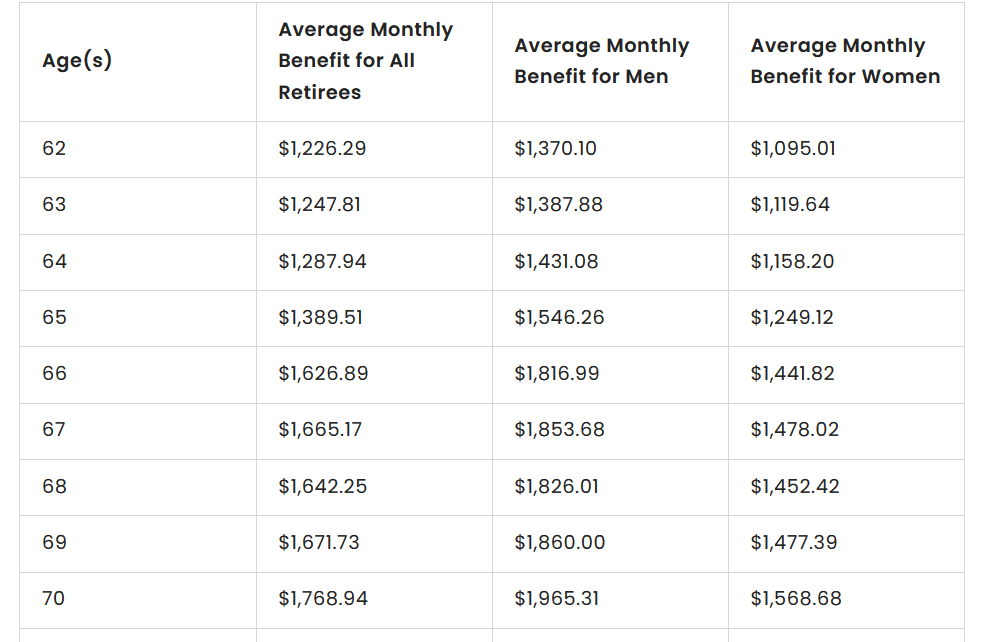

So how will you afford retirement without any savings? Don’t look to Social Security. Here’s some numbers on average Social Security payments. The full chart at the source website goes up to age 100.

As of December 31, 2021, the average Social Security payment for all retirees was $1,658.03 a month, according to the Social Security Administration’s Annual Statistical Supplement for 2022. For men, the overall average was $1,838.08. For women, the average was $1,483.75 — a difference of $354.33 per month.

Whether people unretire or simply stay in the workforce longer, some of the largest financial benefits of additional years of work are delaying retirement account withdrawals and delaying claiming Social Security benefits. These actions essentially shorten the amount of time your assets will need to support you in retirement. Even a few additional years of income have a positive effect on the probability that you won’t outlive your funds.

The Boss once again is outside in the yard doing her thing. I’m inside doing my thing, drinking coffee, reading, writing. One of my addictions is staying current with the news and this post popped up in my RSS feed. At my age it doesn’t take much prompting for me to reflect on retirement. The Road to 70 is nearly complete. Soon I’ll be writing the next chapter of life The Road to 75. Dear Reader, if this sounds “old”, it is.

Critical thinking and understanding risk are the cornerstones of what I do. So when I have an opportunity to validate or repudiate the key assumptions in my plans I am in my Happy Place. When I decided not to retire several years ago my personal mantra focused on the following two critical variables in my retirement planning:

Stay healthy.

Find a willing employer.

Number One. I just had my annual wellness checkup. Bloodwork normal. Tendency towards obesity curtailed. Blood pressure elevated on two readings. Per Doctor’s orders I bought a BP machine and started keeping a log. All of my readings at home have been normal. A little white coat effect and the excitement of seeing my physician (Redhead Effect)…all good.

Number Two. Don’t underestimate how essential having or finding an employer who will pay you to work as you get older. Too many of us know the feeling of being cast out to the street for becoming too “old”.

As I prepare to write the next chapter it’s time to revisit and revise the two most important goals that got me to where I am. After some considerable time and effort here are my revised goals for the next five years.

Retirement blues are “a dirty secret,” says Robert Delamontagne, PhD, author of The Retiring Mind. He had to go through his own adjustment when he retired in 2007. He says people are reluctant to talk openly about those struggles because it’s embarrassing. “People would ask me, ‘How’s retirement?’ I used to say, ‘It’s great! I’m having a great time!’ What was I supposed to say?” Once the newness wears off, you may start to question your new situation. “Will my money last?” “Will my health hold up?” “Am I being useful, or am I going to just play bridge and golf for the rest of my life?”

The strategy has achieved clarity. The Plan is a 3-5 year time-frame. The objective is to continue full time paid work then pursue part time paid work til death do us part. As a younger man I never envisioned this to be my desired life in retirement. But here we are.

Time is the most valuable asset I’m sacrificing for this strategy. Time to do whatever I please, whenever I like. Personal projects like my future best seller The Man Who Had No Hobbies will have a completion date further into the future. But the tradeoffs for me are worth it. Many times I’ve asked retired people how’s retirement? Too many times the answer is “I’m bored”. When you are younger, working your ass off, building a career, raising a family, the thought of retirement is seductive. The reality of retirement is different and nothing you could have imagined in your younger life.

No one talks about what we lose when we retire. Well, no one except Jonathan Clements the founder and editor of https://humbledollar.com/ Here’s his list:

Income

Identity

Purpose

Structure

Community

Relevance

Power

Income. This is the most obvious loss, we all know it’s coming—and yet many folks are left anxious by the disappearance of their paycheck, even if they have ample savings. Moreover, with that paycheck gone, not only do we lose the ability to save, but also our financial life goes into reverse, with savings coming out of our nest egg instead of going in.

Given that, it’s hardly surprising that studies suggest retirees tend to be happier when they have ample predictable income, such as from a pension. Don’t have a pension? To ease the anxiety of retirement, consider delaying Social Security to get a larger monthly check and perhaps also purchasing immediate fixed annuities. I plan to do both.

Read the full article at the link above. Especially if you are nearing retirement.

Well, that’s enough thinking about retirement for a Saturday morning. I have to mow the shade grass The Boss over seeded in the backyard. There’s college football today. I also need to get ready for dinner company tonight.

If you want to live a satisfying, long life, neuroscientist Daniel Levitin has some advice for you: Stay busy. What is the ideal age to retire? Never. Even if you’re physically impaired, it’s best to keep working, either in a job or as a volunteer. Lamont Dozier, the co-writer of such iconic songs as “Heat…

Rather than relying on mass immigration to fill phantom ‘labour shortages’ – in turn displacing both young and older workers alike – the more sensible policy option is to moderate immigration and instead better utilise the existing workforce as well as use automation to overcome any loss of workers as the population ages – as has been utilised in Japan.

Chuck and Barb found that they had a lot in common with their fellow workers, who came from all corners of the United States. Many had seen their retirement savings vanish in the stock market or had lost homes to foreclosure. Others had watched businesses go under or grappled with unemployment and ageism. A larger number had become full-time RVers or vandwellers because they could no longer afford traditional housing—what they called “sticks and bricks.” They talked about how Social Security wasn’t enough to cover the basic necessities and about the yoke of debt from every imaginable source: medical bills, maxed-out credit cards, even student loans.

I was delighted and surprised when I found Nomadland by Jessica Bruder available for loan at my local library. So I downloaded the book and have been reading stories of the forgotten victims of the 2008 financial crisis. I feel lucky and blessed to be where I am at the present time. Life for me could have turned out a lot like the people profiled in this book.

You must be logged in to post a comment.