I briefly considered medical school when I was in my 20’s. I never considered medical school when I was in my 60’s. Wonderful story. A very impressive human being.

Retirement doesn’t just raise financial concerns – it can also mean feeling unmoored and irrelevant

Published: August 29, 2024 8:49am EDT

Author

Marianne Janack John Stewart Kennedy Professor of Philosophy, Hamilton College

Disclosure statement

Marianne Janack does not work for, consult, own shares in or receive funding from any company or organization that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

But this might not be the biggest problem that potential retirees face. The deeper issues of meaning, relevance and identity that retirement can bring to the fore are more significant to some workers.

Work has become central to the modern American identity, as journalist Derek Thompson bemoans in The Atlantic. And some theorists have argued that work shapes what we are. For most people, as business ethicist Al Gini argues, one’s work – which is usually also one’s job – means more than a paycheck. Work can structure our friendships, our understandings of ourselves and others, our ideas about free time, our forms of entertainment – indeed our lives.

I teach a philosophy course about the self, and I find that most of my students think of the problems of identity without thinking about how a job will make them into a particular kind of person. They think mostly about the prestige and pay that come with certain jobs, or about where jobs are located. But when we get to existentialist philosophers such as Jean-Paul Sartre and Simone de Beauvoir, I often urge them to think about what it means to say, as the existentialists do, that “you are what you do.”

Don’t let yourself be misled. Understand issues with help from experts

How you spend 40 years of your life, I tell them, for at least 40 hours each week – the time many people spend at their jobs – is not just a financial decision. And I have come to see that retirement isn’t just a financial decision, either, as I consider that next phase of my life.

Usefulness, tools and freedom

For Greek and Roman philosophers, leisure was more noble than work. The life of the craftsperson, artisan – or even that of the university professor or the lawyer – was to be avoided if wealth made that possible.

The good life was a life not driven by the necessity of producing goods or making money. Work, Aristotle thought, was an obstacle to the achievement of the particular forms of excellence characteristic of human life, like thought, contemplation and study – activities that express the particular character of human beings and are done for their own sake.

And so, one might surmise, retirement would be something that would allow people the kind of leisure that is essential to human excellence. But contemporary retirement does not seem to encourage leisure devoted to developing human excellence, partly because it follows a long period of making oneself into an object – something that is not free.

German philosopher Immanuel Kant distinguished between the value of objects and of subjects by the idea of “use.” Objects are not free: They are meant to be used, like tools – their value is tied to their usefulness. But rational beings like humans, who are subjects, are more than their use value – they are valuable in their own right, unlike tools.

And yet, much of contemporary work culture encourages workers to think of themselves and their value in terms of their use value, a change that would have made both Kant and the ancient Greek and Roman philosophers wonder why people didn’t retire as soon as they could.

But as one of my colleagues said when I asked him about retirement: “If I’m not a college professor, then what am I?” Another friend, who retired at 59, told me that she does not like to describe herself as retired, even though she is. “Retired implies useless,” she said.

So retiring is not just giving up a way of making money; it is a deeply existential issue, one that challenges one’s idea of oneself, one’s place in the world, and one’s usefulness.

One might want to say, with Kant and the ancients, that those of us who have tangled up our identities with our jobs have made ourselves into tools, and we should throw off our shackles by retiring as soon as possible. And perhaps from the outside perspective, that’s true.

But from the participant perspective, it’s harder to resist the ways in which what we have done has made us what we are. Rather than worry about our finances, we should worry, as we think about retirement, more about what the good life for creatures like us – those who are now free from our jobs – should be.

At the age of fifty I began the process of becoming what I wanted to be. I had known for a long time that I was a teacher and that the vehicle for my teaching would be in my writing. I also came to the conclusion I would never be compensated well enough through writing to support myself and my family. So I got good at something else.

That something else has and continues to provide a good living.

What I do is who I am and who I am is what I do. No existential crisis here.

I have made a commitment to work and to share what I learn with others; this is my responsibility and contribution to life. Work has richly educated me, and I am very grateful for the many opportunities I have been given to learn and to share.

Again, you can’t connect the dots looking forward; you can only connect them looking backward. So you have to trust that the dots will somehow connect in your future. You have to trust in something — your gut, destiny, life, karma, whatever. This approach has never let me down, and it has made all the difference in my life.

Sometimes things in life work out as planned. Sometimes they don’t. This time the plan is going as planned. At my annual wellness check up everything turned out fine except for my blood pressure. The two readings taken showed an elevated systolic and per Doctor’s orders I had to buy a BP machine which set me back $36 plus tax. I was instructed to keep a log for two weeks. For grins, I checked my online account to see what Dr. Lewis wrote for the office visit notes. No mention whatsoever regarding my BP readings. Probably because both of us felt this wasn’t a huge problem. The Boss started showing some concern and I had to report my pressures to her every day. Again I felt this wasn’t a worrisome medical issue. Besides if the diagnosis was hypertension I was looking at daily Lisinopril 10 mg, no big deal.

After two weeks I sent Dr. Lewis my log. She replied later that day.

Thank you for diligently keeping track of your blood pressure readings. I see that your readings have been fairly consistent. Yes you can stop watching it. If you feel fatigued or headaches please recheck it.

Sincerely, KL

I survived another annual wellness check. The Road to 70 is still pretty smooth. But the ride is not as smooth for others.

A CivicScience survey of nearly 3,000 respondents conducted between March and May 2024 reported 61% of those aged 55 and over say they won’t be able to retire by 65, and 53% will need to keep working even when they do retire. Boomers and Beyond: 5 Ways To Make Extra Money if You Retire in Your 70s – https://www.gobankingrates.com/retirement/planning/boomers-ways-make-extra-money-retire-70s/.

I admit to falling for the clickbait. Of course I wanted to know about 5 ways to make extra money if I retire in my 70’s. And I’m a Boomer. So I read the article. Here are the 5 ways to make extra money:

Add Money to a High-Yield Savings Account

Buy Dividend Stocks

Rent Out Unused Space in Your Home

Become a Dog Walker

Become a Ride-Share Driver

What is the average monthly benefit for a retired worker? The estimated average monthly Social Security retirement benefit for January 2024 is $1,907. https://faq.ssa.gov/en-us/Topic/article/KA-01903

Hmm…

I wrote back in May that my focus was simple. All I had to do was stay healthy and stay connected with an employer willing to keep an Old Guy with a particular set of skills on the payroll. More Random Thoughts on Retirement – The Dot Project May 2024. At this point I hope to become a dog walker only if I want to, not if I have to. Prioritize your health. Save as much as you can. Plan on living AND working longer. Defer collecting Social Security retirement until you turn 70 (if you can). Read my other blog https://garyskitchen.net/. Tell your friends and family you found this blog written by an Old Guy on what it takes to become an Old Guy. They’ll love you for this.

Again, you can’t connect the dots looking forward; you can only connect them looking backward. So you have to trust that the dots will somehow connect in your future. You have to trust in something — your gut, destiny, life, karma, whatever. This approach has never let me down, and it has made all the difference in my life.

Steve Jobs

Let’s be honest: If you keeled over at 68, it would be a family tragedy—but it wouldn’t be a financial one. At that juncture, all your financial problems would be over, and your family would likely be better off financially because they’d inherit your retirement nest egg, which would probably still be largely intact. Instead, the real financial risk is living to a ripe old age. That raises the question: As you make your retirement plans, shouldn’t you care more about the live version of your future self, rather than the dead one?

Today’s life expectancies hover just below eighty, and if you reach the milestone of seventy they jump to the mid eighties. Due to advances in medicine and healthier lifestyles, reaching your nineties or even 100 is more realistic than ever. How do you ensure that you don’t run out of money? The answer is to start saving more now and plan to work longer. You’re Going to Live Past 90. Congrats! Here’s How to Pay For It. — https://www.esquire.com/news-politics/a60647995/how-to-afford-living-to-100/

A Big Dot

A little over four and a half years ago at the tender age of 65 my boss asked me if I was planning on retiring or if I wanted to continue working. I said I wanted to continue working. My FRA (full retirement age) for social security retirement benefits was still nearly a year away and I really didn’t want to collect a reduced benefit. As I connect the dots this decision turned out to be a Big Dot. Covid happened. Then inflation soared and continues to soar making everything cost more. I’m glad I didn’t retire back then and lock in a lower monthly lifetime benefit before the cost of everything went up.

Sometimes things in life work out as planned. Sometimes they don’t. When I decided to stay in the workforce the strategy was to wait until age 70 to collect social security benefits. The math was compelling.

My focus was simple. All I had to do was stay healthy and stay connected with an employer willing to keep an Old Guy with a particular set of skills on the payroll.

My particular set of skills is understanding what kills people.

The Road to 70 is now just a short trip. Just 10% of people in one survey planned to wait until age 70 to claim Social Security – https://www.cnbc.com/2023/08/08/survey-just-10percent-plan-to-wait-until-age-70-to-claim-social-security.html. Time for another Big Dot related to this Big Dot. I think I’ll keep working for another 3-5 years, contingent upon the same variables of sustained good health and a willing employer. I have about another 30 years to go, so why not do a few more years of work?

One of the most important parts of exercise programming, no matter who I am working with, is proper resistance training to build muscle strength. Some amount of age-related loss of muscle function is normal and inevitable. But by incorporating resistance training that is appropriate and safe at any ability level, you can slow down the rate of decline and even prevent some loss of muscle function.

In one of our team’s previous studies, we saw that otherwise healthy individuals with sarcopenia had issues delivering vital nutrients to muscle. This could lead to greater likelihood of various diseases, such as Type 2 diabetes, and slow down recovery from exercise.

Recent estimates suggest that sarcopenia affects 10% to 16% of the elderly population worldwide. But even if a person doesn’t have clinically diagnosed sarcopenia, they may still have some of the underlying symptoms that, if not dealt with, could lead to sarcopenia.

Reducing overall calorie intake may rejuvenate your muscles and activate biological pathways important for good health, according to researchers. Decreasing calories without depriving the body of essential vitamins and minerals, known as calorie restriction, has long been known to delay the progression of age-related diseases in animal models. This new study suggests the same biological mechanisms may also apply to humans.

Retirement is more than a transition in our relationship with money. It is a major shift in our sense of self. The work that has defined our lives for decades begins to fade from view. Everything about life is different after retirement, down to the minute details of the daily routine. I think it is important to ask yourself, who am I without my job, without my career? And more importantly, how will I spend my time? How will I spend my days, weeks, months, seasons, and years once the routine ends? These are vital questions for anyone contemplating retirement. For many, the allure of endless days on the beach or in the garden loses its luster quite fast. The risk of becoming bored is a real and unexpected risk that many retirees face.

The endless string of triple digit days has finally ended. I’m so thankful that it’s not Too Hot to Blog and the writing is free and effortless once again. I’m still thinking strategy because having A Plan is Not a Strategy – Update 08.03.22. Yet time and time again the question begs an answer. How will I spend my time in retirement?

As long as I continue working the question doesn’t require an answer.

Andel’s suggestion to anyone contemplating retirement: “Find a new routine that’s meaningful.” He points to people living in the Blue Zones, regions of the world that have been identified to be home to a greater number of residents who’ve reached the age of 100 and beyond. One of the common characteristics among Blue Zone inhabitants is, says Andel, “these people all have purpose.”

The funny thing about life at “retirement age” and still working is you think about retirement a lot.

Since I still work a full time job I have a lot of trouble envisioning what my retirement will look like.

After reading this article and listening to Andel’s short talk I am now scared of retirement.

I need to figure out how to avoid brain rot. But my journal tells me I already have.

My Purpose is to educate others on diet and disease, weight loss and weight management by sharing my personal journey through writing and other teaching activities.

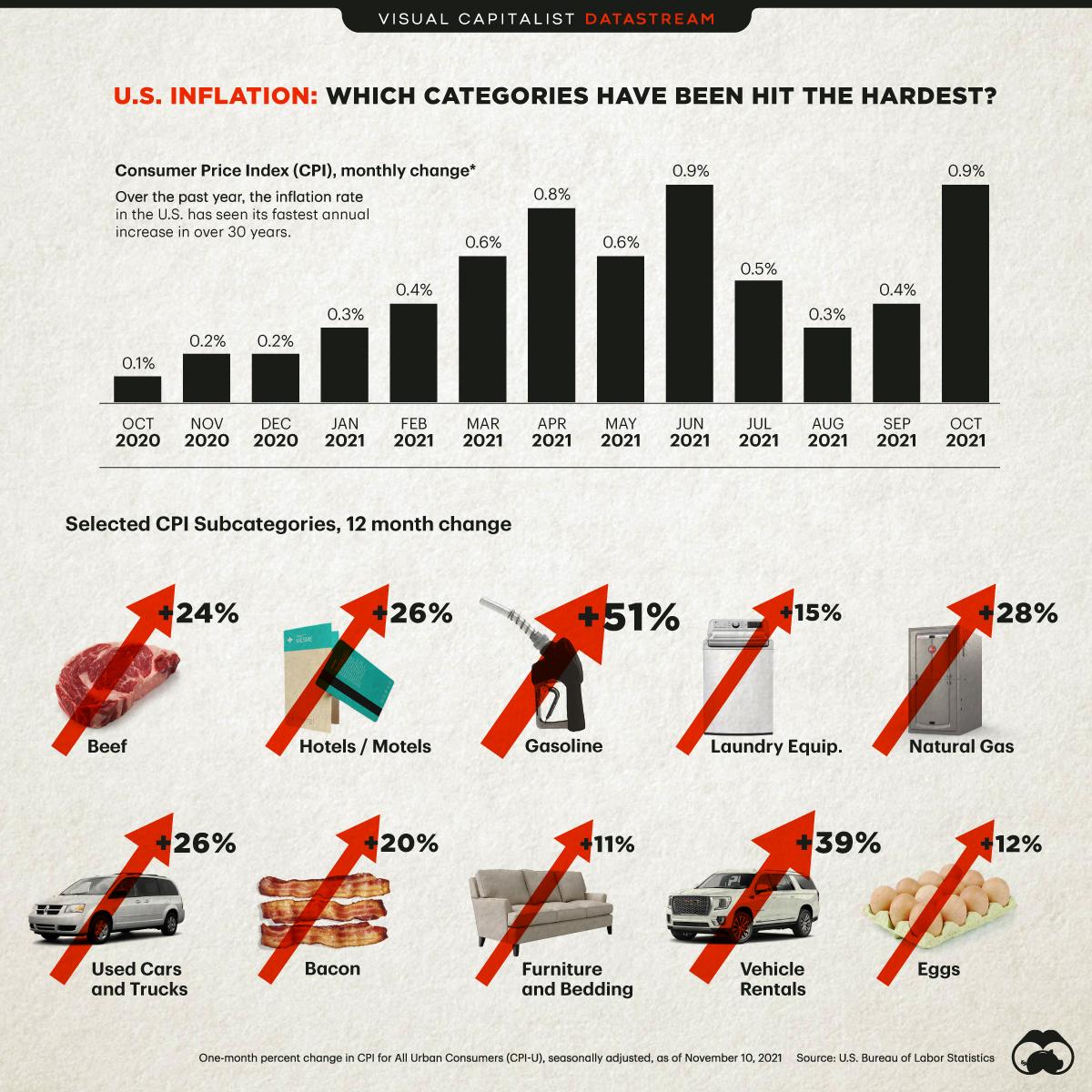

I think a lot of Americans who are preparing to retire now are going to have to rethink their plans. Because there’s no way the money that they’ve saved and the income streams that they anticipate receiving are going to be sufficient given the much higher cost of living that we’re going to be experiencing. And this is not just going to be a few percent a year. We’re talking double-digit increases in the cost of living for many, many years in a row.

Peter Schiff, chief global strategist of Euro Pacific Capital

A hedge against inflation in retirement is to keep working. My patented solution is twofold: Build a nest egg while working, and work for as long as possible, either doing what you’ve been doing, or doing something new and interesting and fun. Full-time is great, but even a part-time gig is great, and for all kinds of reasons, not just money, and even if you have plenty of money and don’t need to work.

Wolf Richter

Retirement math now is simple. If you can, work longer and save more.

You must be logged in to post a comment.