One of the nation’s most beautiful historic shopping arcades was restored as 48 affordable micro-lofts, rents starting at $550 per month, and 17 small retail spaces in Providence, Rhode Island. The Micro Lofts at the Arcade Providence, completed in 2012, helps keep young professionals and artists downtown and is a major step in revitalizing the city. Micro Lofts at the Arcade Providence – https://www.cnu.org/what-we-do/build-great-places/micro-lofts-arcade-providence

If I were a lot younger, single, had a job in a CBD and not set in my Old Man Ways I would consider micro-living. I might even try a repurposed recycled wind turbine.

all images courtesy of Vattenfall and Business in Wind

My uncle Moy F Wong passed away on Sept. 22,2024 at 91 years of age. He was the youngest of eight children on my mother’s side of the family. A bunch of my relatives have lived into their nineties, some to 100 or more.

Now you know why I keep working. I might stick around for another 30 years.

I briefly considered medical school when I was in my 20’s. I never considered medical school when I was in my 60’s. Wonderful story. A very impressive human being.

Retirement doesn’t just raise financial concerns – it can also mean feeling unmoored and irrelevant

Published: August 29, 2024 8:49am EDT

Author

Marianne Janack John Stewart Kennedy Professor of Philosophy, Hamilton College

Disclosure statement

Marianne Janack does not work for, consult, own shares in or receive funding from any company or organization that would benefit from this article, and has disclosed no relevant affiliations beyond their academic appointment.

But this might not be the biggest problem that potential retirees face. The deeper issues of meaning, relevance and identity that retirement can bring to the fore are more significant to some workers.

Work has become central to the modern American identity, as journalist Derek Thompson bemoans in The Atlantic. And some theorists have argued that work shapes what we are. For most people, as business ethicist Al Gini argues, one’s work – which is usually also one’s job – means more than a paycheck. Work can structure our friendships, our understandings of ourselves and others, our ideas about free time, our forms of entertainment – indeed our lives.

I teach a philosophy course about the self, and I find that most of my students think of the problems of identity without thinking about how a job will make them into a particular kind of person. They think mostly about the prestige and pay that come with certain jobs, or about where jobs are located. But when we get to existentialist philosophers such as Jean-Paul Sartre and Simone de Beauvoir, I often urge them to think about what it means to say, as the existentialists do, that “you are what you do.”

Don’t let yourself be misled. Understand issues with help from experts

How you spend 40 years of your life, I tell them, for at least 40 hours each week – the time many people spend at their jobs – is not just a financial decision. And I have come to see that retirement isn’t just a financial decision, either, as I consider that next phase of my life.

Usefulness, tools and freedom

For Greek and Roman philosophers, leisure was more noble than work. The life of the craftsperson, artisan – or even that of the university professor or the lawyer – was to be avoided if wealth made that possible.

The good life was a life not driven by the necessity of producing goods or making money. Work, Aristotle thought, was an obstacle to the achievement of the particular forms of excellence characteristic of human life, like thought, contemplation and study – activities that express the particular character of human beings and are done for their own sake.

And so, one might surmise, retirement would be something that would allow people the kind of leisure that is essential to human excellence. But contemporary retirement does not seem to encourage leisure devoted to developing human excellence, partly because it follows a long period of making oneself into an object – something that is not free.

German philosopher Immanuel Kant distinguished between the value of objects and of subjects by the idea of “use.” Objects are not free: They are meant to be used, like tools – their value is tied to their usefulness. But rational beings like humans, who are subjects, are more than their use value – they are valuable in their own right, unlike tools.

And yet, much of contemporary work culture encourages workers to think of themselves and their value in terms of their use value, a change that would have made both Kant and the ancient Greek and Roman philosophers wonder why people didn’t retire as soon as they could.

But as one of my colleagues said when I asked him about retirement: “If I’m not a college professor, then what am I?” Another friend, who retired at 59, told me that she does not like to describe herself as retired, even though she is. “Retired implies useless,” she said.

So retiring is not just giving up a way of making money; it is a deeply existential issue, one that challenges one’s idea of oneself, one’s place in the world, and one’s usefulness.

One might want to say, with Kant and the ancients, that those of us who have tangled up our identities with our jobs have made ourselves into tools, and we should throw off our shackles by retiring as soon as possible. And perhaps from the outside perspective, that’s true.

But from the participant perspective, it’s harder to resist the ways in which what we have done has made us what we are. Rather than worry about our finances, we should worry, as we think about retirement, more about what the good life for creatures like us – those who are now free from our jobs – should be.

At the age of fifty I began the process of becoming what I wanted to be. I had known for a long time that I was a teacher and that the vehicle for my teaching would be in my writing. I also came to the conclusion I would never be compensated well enough through writing to support myself and my family. So I got good at something else.

That something else has and continues to provide a good living.

What I do is who I am and who I am is what I do. No existential crisis here.

If you’ve been to my blog before I apologize for repeating myself. But for new readers I’m past the “traditional” retirement age of 65. I don’t want to retire nor do I intend to retire for several years. One word describes why I continue to work. FEAR. I’m afraid of living too long and outliving my savings. I am petrified of leaving the workforce and no longer having an earned income stream. Living on a fixed income when the cost of everything keeps going higher scares the shit out of me.

Amidst my fear and anxiety the Social Security Administration approved my application for retirement benefits. When I looked at my monthly benefit I was pleasantly surprised. I then added up our future income sources and calculated that our fixed income from social security plus a small defined benefit pension plan will cover 82.5% of our current monthly expenses. Add in future annual withdrawals from savings and investments The Boss and I are financially OK until our nineties.

My fears are overblown. Check this out:

Conventional financial planning also overstates the income seniors need. That owes partly to planners assuming that seniors require the same amount of money throughout retirement. Yet as economists Michael Hurd and Susanne Rohwedder of the Rand Corp. have shown, average household spending drops by roughly 40% from age 65 to 90. Seniors aren’t running out of money—spending on gifts and donations increases with age. Retirees simply spend less on themselves than financial planners assume.

Planners likewise forget that much of adults’ pre-retirement income is spent on their children. The U.S. estimates that a couple earning roughly $83,000 with two children spends more than $26,000 annually providing food, housing, healthcare and other needs for their children. That’s money parents can’t spend on themselves. Of the income they could devote to their own needs, Social Security will replace around 60%. The upshot is that parents need less savings on top of Social Security than one might think. You Don’t Need to Be a Millionaire to Retire By Andrew G. Biggshttps://www.aei.org/op-eds/you-dont-need-to-be-a-millionaire-to-retire/

“I faced a painful reality: I didn’t know anything about anything….”

Andy Clarke – financial writer and editor, a retired CFA dispensing advice to retirees on investing and savings.

A 2021 survey by Pew Research looked at the question another way: It asked people from around the world what made their lives meaningful. In countries such as Italy, Spain, and Sweden, work ranked highly as a source of meaning. In Italy, work was the No. 1 source of meaning, with 43% saying they drew meaning from work. Spaniards ranked work higher than family. But in the US, only 17% mentioned work as a source of meaning. That was a sharp decline from when Pew asked the same question four years prior — a full one-third of Americans mentioned their jobs as a source of meaning in 2017, double the 2021 rate. Increasingly, it seems that more people feel like their jobs don’t matter. Why so many Americans hate their jobs — https://www.businessinsider.com/american-employees-disengaged-work-meaningless-fake-email-jobs-2024-6

Here are some of the biggest reasons some people don’t have enough money saved for retirement:

You don’t make enough money. This is likely the biggest reason most households don’t have enough retirement savings. Some people simply don’t earn a high enough income to have any money left over.

There are personal finance people who would like you to believe it’s all bad habits that cause people to under-fund their retirement.

Many people don’t have any excess remaining after paying for necessities.

We saved as much as we could and if I work a few more years we can plump up our financial cushion. Our expenses will likely be less in the years to come (except someone’s clothing/shoe/Tiny Human budget and that someone is not me). So with a willing employer and continued good health I plan to work full time for a few more years and then ease into retirement by continuing to work part time.

The first five years of my 30 Year Plan is complete. Now I need to work on what to do for the 25 years afterwards.

I have made a commitment to work and to share what I learn with others; this is my responsibility and contribution to life. Work has richly educated me, and I am very grateful for the many opportunities I have been given to learn and to share.

The Boss once again is outside in the yard doing her thing. I’m inside doing my thing, drinking coffee, reading, writing. One of my addictions is staying current with the news and this post popped up in my RSS feed. At my age it doesn’t take much prompting for me to reflect on retirement. The Road to 70 is nearly complete. Soon I’ll be writing the next chapter of life The Road to 75. Dear Reader, if this sounds “old”, it is.

Critical thinking and understanding risk are the cornerstones of what I do. So when I have an opportunity to validate or repudiate the key assumptions in my plans I am in my Happy Place. When I decided not to retire several years ago my personal mantra focused on the following two critical variables in my retirement planning:

Stay healthy.

Find a willing employer.

Number One. I just had my annual wellness checkup. Bloodwork normal. Tendency towards obesity curtailed. Blood pressure elevated on two readings. Per Doctor’s orders I bought a BP machine and started keeping a log. All of my readings at home have been normal. A little white coat effect and the excitement of seeing my physician (Redhead Effect)…all good.

Number Two. Don’t underestimate how essential having or finding an employer who will pay you to work as you get older. Too many of us know the feeling of being cast out to the street for becoming too “old”.

As I prepare to write the next chapter it’s time to revisit and revise the two most important goals that got me to where I am. After some considerable time and effort here are my revised goals for the next five years.

A very astute reader asked a very simple question: Why is this scary? So I went back and looked at my post. I thought I had completed the post but obviously not. The chart lacked context. So here’s the rest of the post I thought I posted. Welcome to my Senior Moment.

The relatively high labor force participation of Boomers may be beneficial both to them and the wider economy. Some retirement experts emphasize working longer as the key to a secure retirement, in part because the generosity of monthly Social Security benefits increases with each year claiming is postponed. For the economy as a whole, economic growth in part depends on labor force growth, and the Boomers staying in the work force bolsters the latter.

To ease the anxiety of retirement, consider delaying Social Security to get a larger monthly check and perhaps also purchasing immediate fixed annuities. I plan to do both.

Specifically the part of the quote in bold bugged me. I thought to myself, nice plan. But how many people can afford to buy an immediate fixed annuity? I can’t. How many people actually defer Social Security until age 70 to maximize their monthly payments?

Well, get ready for the ugly. It’s Scary Chart time.

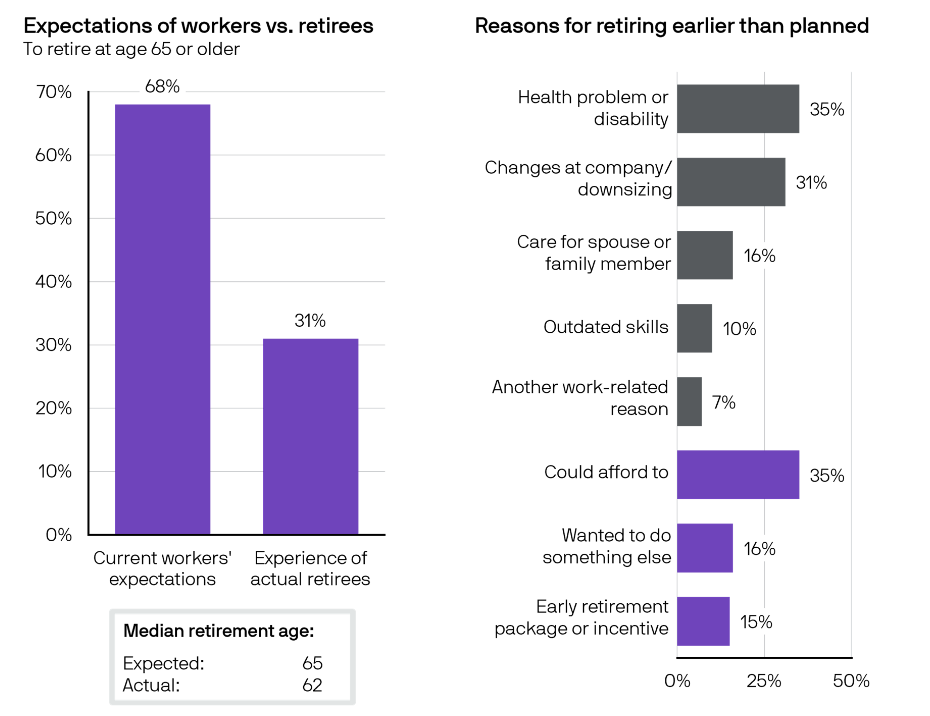

Answer: 4%

Why just 4%?

Answer: 97% of people who retired sooner than planned did so due to health and employment issues.

And some retirees will leave the working world straight into a world of high inflation.

Just beyond the guests and beyond the hornbeam trees where I’ve strung fairy lights for the party, I think I can see my future. The grind of work is finally over, my retirement dream cued up. April in Paris! Reading by the sea! Spanish lessons in Antigua so I can better speak to my grandson. I’ll be playing with him, too, in the open-ended days my children rarely knew with me. I’m not saying I deserve a life of ease. But I worked hard to earn my retirement, dropping giant chunks of my salary into company and government pension plans throughout those forty years. It’s time for the famous social contract to hold up its end of the bargain and take care of me, the way it did my father before me, to deliver on the idea that retirement is my right after a life of work and the promise that I will have the time and means to enjoy it.

Except none of that happened. The year since my retirement party has not been a dreamy passage to a welcoming future but a nerve-shattering trip into the unknown. My debt is swelling like a broken ankle; my hard-won savings may or may not be sucked into the vortex of an international market collapse. Can I keep my house? Who knows? The macro-economy is messing with my micro-economy. The future keeps shape-shifting. And none of the careful planning I put into my retirement is going to change that.

Another quiet Sunday and I’m thinking about retirement (again). Writers read a lot. I’ll typically have quite a number of books started in various stages of completion. Recently I started reading the first in a series of books titled The Write Quotes: The Writing Life. The quotes paint similarities of thoughts and experiences and are amazing. You realize you are never alone in any of life’s adventures.

Since 2021, more than 1.5 million seniors have reentered the workforce. There were about 10.6 million people ages 65 to 74 employed in 2020, according to 2021 data from the U.S. Labor Department.

Just last month I came to the realization that (I am) Flunking Retirement. When 65 rolled around I started collecting a small corporate defined benefit pension. Years ago the monthly amount had a lot more purchasing power than it does now. Still, I feel fortunate to have this income stream.

In yesteryear, the pension was a staple of the American working class experience—reach retirement age and you could expect to live out your years modestly, yet comfortably, off of monthly payments from your former employer. However, since the 1980s, companies offering pensions are a dwindling breed. Instead, most employers offer defined contribution programs such as 401(k) plans. Only a handful of industries (such as the military, public works and education) still offer pension plans to their retirees.

When I reached my US Social Security FRA (full retirement age) I didn’t retire nor start collecting benefits. Delaying social security payments until age 70 translates into about an 8% increase in benefits annually. If you’re healthy and you don’t need the income for necessities, it’s worth the wait.

Working longer is a powerful lever. Social Security benefits claimed at 70 instead of at 62 are at least 76 percent higher, and the additional years of work allow 401(k) assets to increase and reduce the period of time that the assets need to cover. In fact, my research shows that the vast majority of millennials will be fine if they work to age 70. And although that might sound old, it’s historically normal in another sense: Retiring at 70 leaves the ratio of retirement to working years the same as when Social Security was originally introduced.

Millennials are not the only generation ill-prepared for retirement.

America’s 65 million Generation Xers (born between 1965 and 1980) are confronted with a new set of financial challenges that are redefining their plans for retirement, just as they enter their final working years, according to Prudential Financial, Inc.’s latest Pulse research survey, “Gen X:Retirement Revised.”

Remember A Plan is Not a Strategy – Update 08.03.22? Having a plan for retirement is great but not all plans turn out as planned. My last executive position ended up being my last executive position and trust me, that was not what I planned. It’s a good thing that my strategy worked a lot better than my plans.

Stay tuned for the next installment of my random thoughts on retirement where I will document (finally) the integrative choices I’ve made that comprise my retirement strategy.

You must be logged in to post a comment.